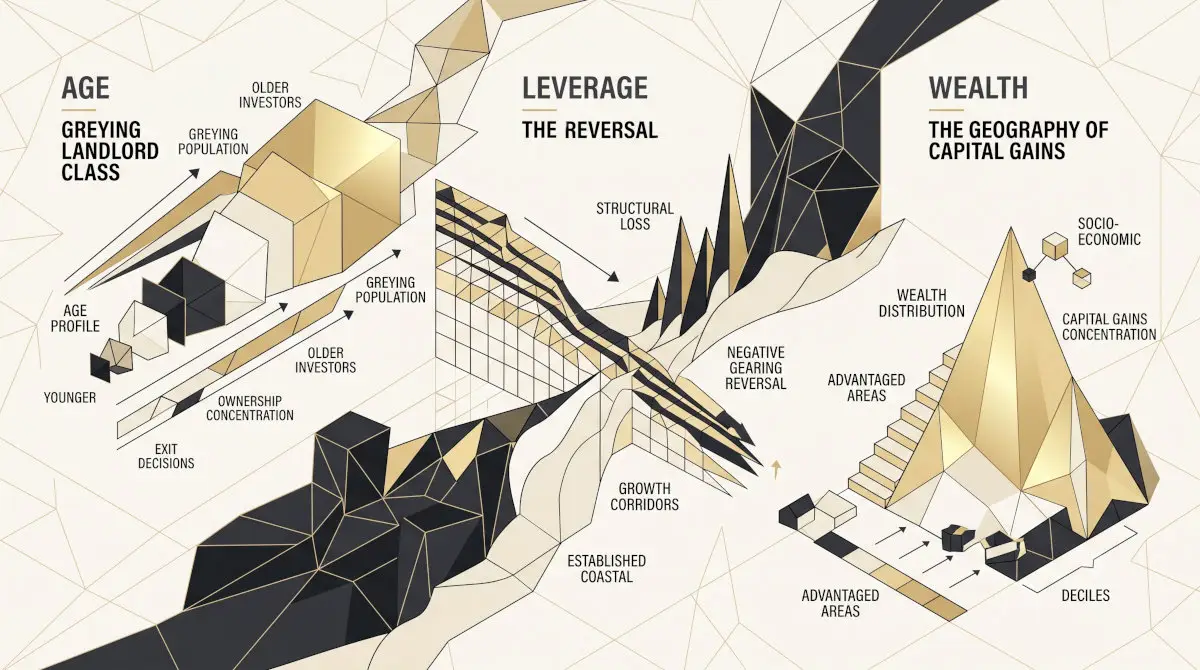

Three separate views of the Australian Taxation Office’s 2023–24 record — the last income year before the capital gains tax and negative gearing reforms received Royal Assent on 26 June 2026 — describe the same landlord class from three angles, and none of them agree with the popular account. It is not younger, more leveraged, or more evenly spread than the tax record shows. It is older than at any point in the 25-year series, it had just re-entered a structural loss position after the sharpest two-year deterioration on record, and the capital gains it did realise were concentrated overwhelmingly in the wealthiest tenth of local government areas. Age, leverage and wealth are three different lenses on the same reform-eve population — and each shows a landlord class more concentrated, not less, than the year before.

The Greying Landlord Class

Australia’s landlord population doubled over 25 years. The number of landlords under thirty fell. Between 1999–2000 and 2023–24, the number of Australians declaring rental property interests on their personal tax returns grew from 1.16 million to 2.34 million — a doubling, against national population growth of roughly a third. Every age cohort participated in that expansion except one. The number of landlords under thirty stood at 109,200 at the start of the series and 100,168 at its end: an absolute decline, sustained across a quarter-century in which the investor class as a whole doubled. The popular account of young property investors crowding out first home buyers finds no support in the taxation record.

Landlord Age Cohort Shares, 1999–2000 to 2023–24

Cohort shares of the landlord population, 1999–2000 to 2023–24. Source: ATO Taxation Statistics, individuals with rental property interests by age range.

The crossover. In 1999–2000, landlords aged sixty or more were the smallest adult cohort in the distribution, holding 14.7 per cent of rental interests by headcount. Their share rose in every year of the series but four, reaching 27.5 per cent by 2023–24 — a near-doubling. The decisive moment came in 2020–21, when the sixty-plus cohort overtook the 50–59s to become the single largest landlord age group in the country; it has extended that lead in each year since, reaching 642,351 individuals in 2023–24. The under-thirty share, meanwhile, declined from 9.4 per cent to 4.3 per cent, falling monotonically for the thirteen consecutive years from 2007–08 to 2020–21.

Steeper when weighted by property. The headcount understates the concentration, because portfolio depth rises monotonically with age. In 2023–24, 11.9 per cent of landlords under thirty held two or more property interests; the figure rises through every bracket to 32.9 per cent among the sixty-plus cohort. This is the demographic complement to the leverage geography described below: the loss-making, negatively geared segment of the market is younger and corridor-concentrated, while the older cohorts hold the unleveraged, positively geared stock — increasingly, the majority of it.

A rental supply base concentrated in owners at or beyond retirement age is a supply base whose forward trajectory is governed by exit decisions — sale, downsizing restructure, or transfer through estates — rather than by acquisition decisions, and each of those exit channels is priced, in part, by capital gains tax settings that have just changed. The series counts individuals declaring rental interests on personal returns; properties held through trusts, companies and self-managed superannuation funds sit outside it, and the growth of those vehicles over the period means some fraction of the young-cohort decline may reflect a migration of ownership structure rather than of ownership itself. The direction of the aging trend is robust to this caveat; its precise magnitude is not.

The Reversal

Negative gearing spent fourteen years in structural decline. Two years of the rate cycle returned it to its 25-year baseline — in the same fiscal window in which the reforms were conceived, drafted and debated. In 2023–24, 54.2 per cent of the nation’s 2.34 million individual landlords declared a net rental loss — within a percentage point of where the series began in 1999–2000. What makes the figure consequential is the path travelled between those two points. The share of loss-making landlords had been falling almost without interruption since 2007–08; the rate-tightening cycle that began in May 2022 reversed fourteen years of decline in two tax years.

Loss-Maker Share of Landlords, 1999–2000 to 2023–24

Share of landlords declaring net rental losses, 1999–2000 to 2023–24. Source: ATO Taxation Statistics, individuals with rental property interests.

Two years of reversal. Between 2021–22 and 2023–24 the loss share rose 12.3 percentage points, from 41.9 to 54.2 per cent — retracing in two years roughly what had taken the preceding nine to accumulate. Aggregate declared rental losses expanded from $5.98 billion in 2021–22 to $15.22 billion in 2023–24, a factor of 2.5, while the average loss per loss-making landlord nearly doubled from $6,298 to $12,014. The sector as a whole re-entered negatively geared territory — a net positive $5.87 billion to national taxable income in 2021–22 became a net negative $2.74 billion by 2023–24 — in the year the reform legislation was being drafted.

The geography of loss. The 2023–24 distribution across local government areas describes two different rental markets. The highest loss shares concentrate in the outer metropolitan growth corridors: Wyndham (80.6 per cent of landlords in loss), Melton (78.0), Casey (77.1), Blacktown (73.9) and Hume (73.3) — four of five Melbourne growth-corridor municipalities, all characterised by recently acquired, highly leveraged stock. At the other end sit the lifestyle-coast markets of northern and southern New South Wales: Byron (32.2 per cent), Bega Valley (33.8), Lismore and Mid-Coast (36.8 each) and Ballina (37.2) — consistent with long-held, low-debt portfolios in the hands of older owners. Negative gearing, in its 2023–24 form, is a phenomenon of tenure vintage and leverage rather than of location per se. Notably, the two-year deterioration was uniform across the socio-economic distribution — approximately five percentage points in every IRSAD decile — a repricing event applied across the entire leveraged landlord base, not a phenomenon of advantaged or disadvantaged areas specifically.

Two limitations bound the analysis. The series counts individuals declaring rental interests on personal returns, excluding trusts, companies and SMSFs. And 2023–24 is the final pre-reform observation: the behavioural response to the new settings — whether the loss-making majority holds, sells or restructures — will not be observable in taxation statistics until at least the 2026–27 income year is published. What the record establishes now is the starting condition: the reform arrived at the precise moment the behaviour it targets had returned to its 25-year baseline, after a decade in which it had been organically receding.

The Geography of Capital Gains

In the final pre-reform tax year, the most advantaged tenth of local government areas declared 43.5 per cent of the nation’s net capital gains from a fifth of its taxfilers. The incidence map of the CGT changes requires no modelling — it is already on file. Net capital gains are among the most geographically concentrated line items in the personal tax system, and the gradient runs precisely along the axis of socio-economic advantage.

Share of Taxfilers vs Share of Net Capital Gains by IRSAD Decile, 2023–24

Share of taxfilers vs share of net capital gains by IRSAD decile, 2023–24. Source: ATO postcode statistics aggregated to LGA; ABS SEIFA 2021.

Two-thirds of gains from the top two deciles. Ranked by the ABS Index of Relative Socio-economic Advantage and Disadvantage, LGAs in the top decile held 21.3 per cent of the nation’s taxfilers in 2023–24 but declared 43.5 per cent of its net capital gains. The ninth and tenth deciles together — 44.5 per cent of taxfilers — accounted for 67.9 per cent of the national pool. Across 316 LGAs with at least 5,000 taxfilers, the correlation between an area’s share of residents declaring a net capital gain and its IRSAD decile is r = 0.64. Correlation does not establish causation, and the mechanism here is unmysterious in any case: capital gains require capital.

A sixty-five-fold gradient. Cottesloe, on Perth’s western beaches, declared $23,186 in net capital gains per resident taxfiler in 2023–24 — the highest in the country — followed by Woollahra ($22,531) and Mosman ($18,288). At the other end sit Katherine ($355), Glenorchy ($537) and Port Augusta ($583). The participation gradient matches the magnitude gradient: 19.8 per cent of Mosman’s taxfilers declared a net capital gain, against an average of 7.8 per cent across significant LGAs.

The national pool was growing into the reform, not shrinking — aggregate net capital gains declared across LGAs rose from $36.9 billion in 2022–23 to $39.3 billion in 2023–24. Three boundaries on interpretation: net capital gains in the ATO’s postcode statistics aggregate all asset classes, not property specifically; the geography is that of claimant residence, not asset location; and LGA-level capital gains data exist in the APN Codex for two income years only, so the concentration described here is a cross-sectional fact, not a trend claim.

Three Lenses, One Landlord Class

The three series were not built as a single cross-tabulation — each is drawn from a different ATO statistical collection, at a different unit of aggregation, and none directly links an individual’s age, loss status and capital gains in the one record. What can be said is that the three descriptive facts are consistent with, rather than contradictory to, a single underlying population: an ageing cohort of largely unleveraged, long-held property increasingly concentrated in high-advantage areas, sitting alongside a younger, more leveraged, corridor-concentrated cohort now back in a structural loss position. The Reversal’s finding that loss-share deterioration was uniform across IRSAD deciles is a useful check against overreading this synthesis — the loss-side story is not itself an advantage-gradient story. The three findings describe complementary structural facts about the same reform-eve population; they are not evidence of a single mechanism linking them, and none of the three datasets can be joined at the individual level to test that directly.

Methodology Note

All three analyses draw on ATO Taxation Statistics for individuals with rental property interests and net capital gains, 1999–2000 to 2023–24 (rental interests) and 2022–23 to 2023–24 (capital gains, postcode-level only). Local government area figures are aggregated from ATO postcode-level statistics via the APN Mesh Block concordance; LGAs with fewer than 2,000 landlord taxpayers are excluded from loss-share rankings, and LGAs with fewer than 5,000 taxfilers are excluded from per-taxfiler capital gains rankings. IRSAD decile is the ABS Index of Relative Socio-economic Advantage and Disadvantage, 2021 vintage. Dollar figures throughout are nominal.

Loss share is individuals declaring an overall net rent loss as a proportion of all individuals declaring rental interests with a determinable outcome. Cohort shares are computed on individuals with a stated age range; unknown-age records (fewer than ten per year) are excluded. Interests are counted per individual, so a jointly held property appears once for each holder. Properties held through trusts, companies and self-managed superannuation funds sit outside all three series; the growth of those vehicles over the period means each series is a conservative measure of total investor activity. Small-postcode suppression in the ATO source carries through to LGA aggregation; affected areas are excluded rather than estimated. All analysis is descriptive; correlation does not establish causation, and none of the three datasets can be joined at the individual level.