The ‘Green Floor’: Structural Adjustment in Australian Farmland Values Driven by the Nature Repair Market

APN ANALYSIS: A-251127-AUS131235

Executive Summary

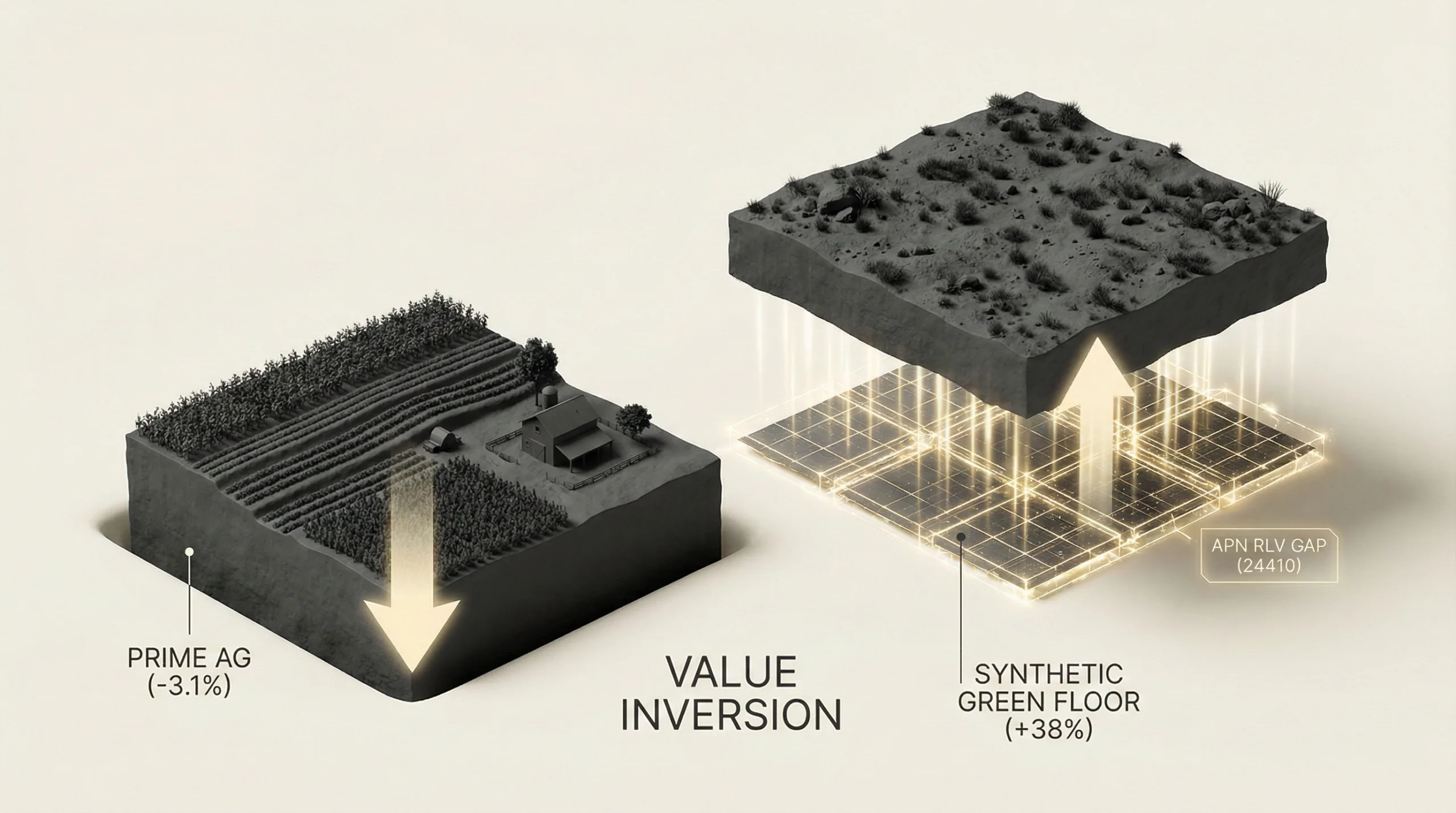

The Australian agricultural property market has undergone a structural adjustment. The operationalisation of the Nature Repair Market (NRM) in late 2025 has created a synthetic ‘Green Floor’ under the value of marginal grazing land, decoupling it from traditional agricultural fundamentals. While prime farmland values are entering a corrective cycle, declining 3.1% nationally due to higher interest rates and commodity price normalisation, specific ‘substrate’ zones in Western Australia are experiencing accelerated growth of up to 38%. This counter-cyclical appreciation is driven entirely by the capitalisation of anticipated environmental income streams from carbon and biodiversity credits, not agricultural output.

For property professionals, this represents a structural re-rating of land utility. The ‘Highest and Best Use’ for vast tracts of marginal country has structurally shifted from producing food and fibre to producing environmental certificates. This has created a new, institutionally-backed asset class—’Environmental Infrastructure’—and demands a fundamental rethink of valuation methodologies, risk assessment, and acquisition strategy for assets previously considered low-value.

Background & Strategic Context

This event validates and calibrates APN’s core macro-theses, demonstrating how state-level intervention directly structures new market boundaries and asset classes, creating cohorts with differential market outcomes.

State-Level Market Structuring (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The federal government’s creation of the Nature Repair Market is a direct application of the principles tracked by the APN Sovereign Policy Composite Index™ (SPCI, 24800). The legislation has structured a new source of demand for a specific land type, degraded grazing country, creating a regulatory arbitrage that overrides traditional market forces and establishes a synthetic price floor.

Quantifying the Green Premium (APN Climate-Risk Asset Devaluation Index™ – 24500): The +13% to +38% valuation increase in ‘substrate’ zones like the Great Eastern and Avon-Midland regions is a direct manifestation of the APN Regional Green Premium Uplift™ (24520). This index is now calibrated to track the quantifiable premium paid for land with high carbon and biodiversity yield potential over land valued purely on its agricultural productivity.

Defining the New Asset Class (APN Substrate™ – 24150): The market’s bifurcation confirms the utility of the APN Substrate™ framework. The index moves beyond simple climate risk to define and value land based on its ‘Ecological Deficit’, its potential for restoration. This analysis confirms that degraded land, once a liability, is now a premium input for generating environmental certificates, inverting traditional valuation logic.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Clean Energy Regulator’s Q3 2025 Quarterly Carbon Market Report and the Bendigo Bank Farmland Values 2025 Mid-Year Update. The key facts are:

- Market Bifurcation: While national median farmland values declined 3.1% year-on-year to $9,885/ha, marginal ‘substrate’ zones in Western Australia (Avon-Midland, Great Eastern) appreciated by +13% to +38%.

- NRM Operationalisation: The first Nature Repair Market project, Silva Capital’s Cooplacurripa Biodiversity Project No.1, was registered on 12 August 2025, confirming the market is live and providing a tangible benchmark for investors.

- Valuation Mechanism: The ‘Green Floor’ is an implied value derived from ‘stacking’ Nature Repair Certificates on top of Australian Carbon Credit Units (ACCUs). This creates an anticipated revenue stream of $40-$50/ha/yr (biodiversity) on top of carbon income, which, when capitalised, justifies land values 45-80% above traditional grazing valuations.

- Analysis of Market Liquidity: The secondary market for Nature Repair Certificates is currently non-existent, with zero trades recorded in Q3 2025. The valuation increase is driven by accelerated acquisition by institutional aggregators securing future supply for corporate compliance (Safeguard Mechanism) and voluntary commitments, not by realised cash flows from certificate sales.

Critical Analysis & Balanced View

The central paradox is a material escalation in valuation for an asset class whose derivative income stream (NRM certificates) is illiquid. However, to label this a simple speculative valuation premium would be a misreading of the underlying driver. The liquidity is not absent; it is internalised. The buyers of the ‘substrate’, aggregators like Silva Capital and GreenCollar, are backed by long-term institutional capital (pension funds) and corporate off-takers (Rio Tinto, BHP, Qantas) who are not speculating on short-term certificate prices. They are strategically hedging multi-decade, multi-billion-dollar carbon liabilities under the legislated Safeguard Mechanism.

This transforms the land from a speculative asset into a piece of essential environmental infrastructure. The ‘Green Floor’ is therefore not supported by market sentiment, but by the balance sheets of Australia’s largest corporations and the force of federal law. The primary risk is not a material valuation correction, but a future policy reversal. This dynamic has inverted agricultural valuation principles: for this asset class, ecological degradation is now the primary indicator of financial potential, as it represents the ‘uplift’ that can be monetised.

Strategic Implications for Property Professionals

- For Valuers & Financiers: Traditional valuation methodologies based on carrying capacity (DSE/ha) are now no longer structurally viable for marginal land. Valuations must incorporate a ‘dual-use’ potential, pricing the option value of conversion to a carbon/biodiversity project. This requires new expertise in environmental market mechanics and ACCU/NRM yield modelling.

- For Agents & Buyers’ Agents: The target buyer profile for marginal country has shifted from owner-operator graziers to institutional funds and carbon aggregators. Marketing campaigns must pivot from highlighting agricultural productivity to showcasing ‘substrate potential’, ecological deficit, rainfall, scale, and proximity to conservation zones.

- For Agricultural Consultants & Farm Managers: A new advisory stream has opened. The highest return on capital for clients with marginal land may no longer be investing in pasture improvement, but in navigating the complexities of NRM project registration and management. This represents a strategic pivot from food production to environmental services.

- For Developers & Strategic Land Acquirers: The ‘Green Floor’ creates a firm valuation baseline for large-scale rural holdings, reducing downside risk. However, it also introduces a new, well-capitalised competitor for land, potentially displacing traditional agricultural expansion and creating scarcity for land suitable for other forms of development.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides validation for the APN Climate-Risk Asset Devaluation Index™ (24500) and its core thesis that climate-related regulation is a primary driver of asset re-pricing. It also validates the APN Substrate™ (24150) framework as a necessary tool for identifying and classifying this new environmental asset class.

- Index Calibration: The APN Regional Green Premium Uplift™ (24520) is now calibrated using the +13% to +38% value differential observed between WA’s ‘substrate’ zones and the national average. The implied yield of ~$40-50/ha/year for NRM certificates will be used as a baseline input for modelling financial sensitivity in these regions.

- Data Capture: This analysis triggers a new data capture mandate under the APN Symbiotic Intelligence Network™ (24310) to monitor all NRM project registrations, methodologies, and aggregator land acquisitions. The goal is to build a predictive model for identifying the next ‘substrate’ hotspots before they are priced by the open market.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.