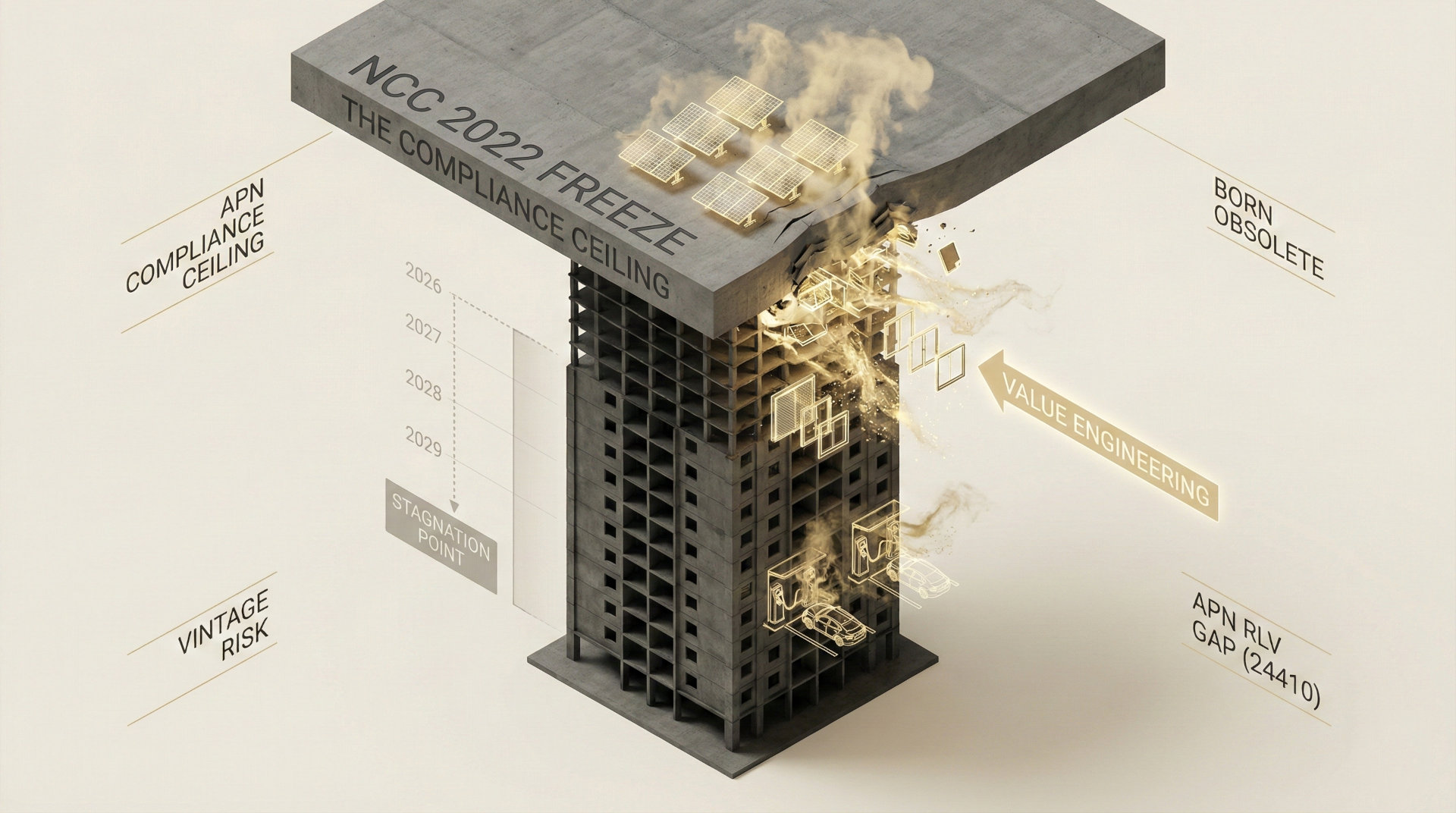

The ‘Compliance Ceiling’: How Regulatory Stagnation is Producing an Asset Class Structurally Non-Viable at Completion

APN ANALYSIS: A-260210-AUS137147

Executive Summary

The Australian residential property sector has entered a phase defined by a ‘Compliance Ceiling’, a regulatory freeze on residential building standards that will remain static until mid-2029. This policy, enacted by the Building Ministers’ Meeting in October 2025 to stimulate housing supply, has inadvertently triggered a systemic ‘value engineering’ trend. In the current high-interest-rate environment, developers are serially utilising planning modification mechanisms, such as NSW’s Section 4.55 and Victoria’s Section 72, to strip non-mandated sustainability features from approved projects to ensure financial viability. This behaviour is creating a distinct and vulnerable asset class: residential stock built between 2026 and 2029 that is structurally non-viable upon completion.

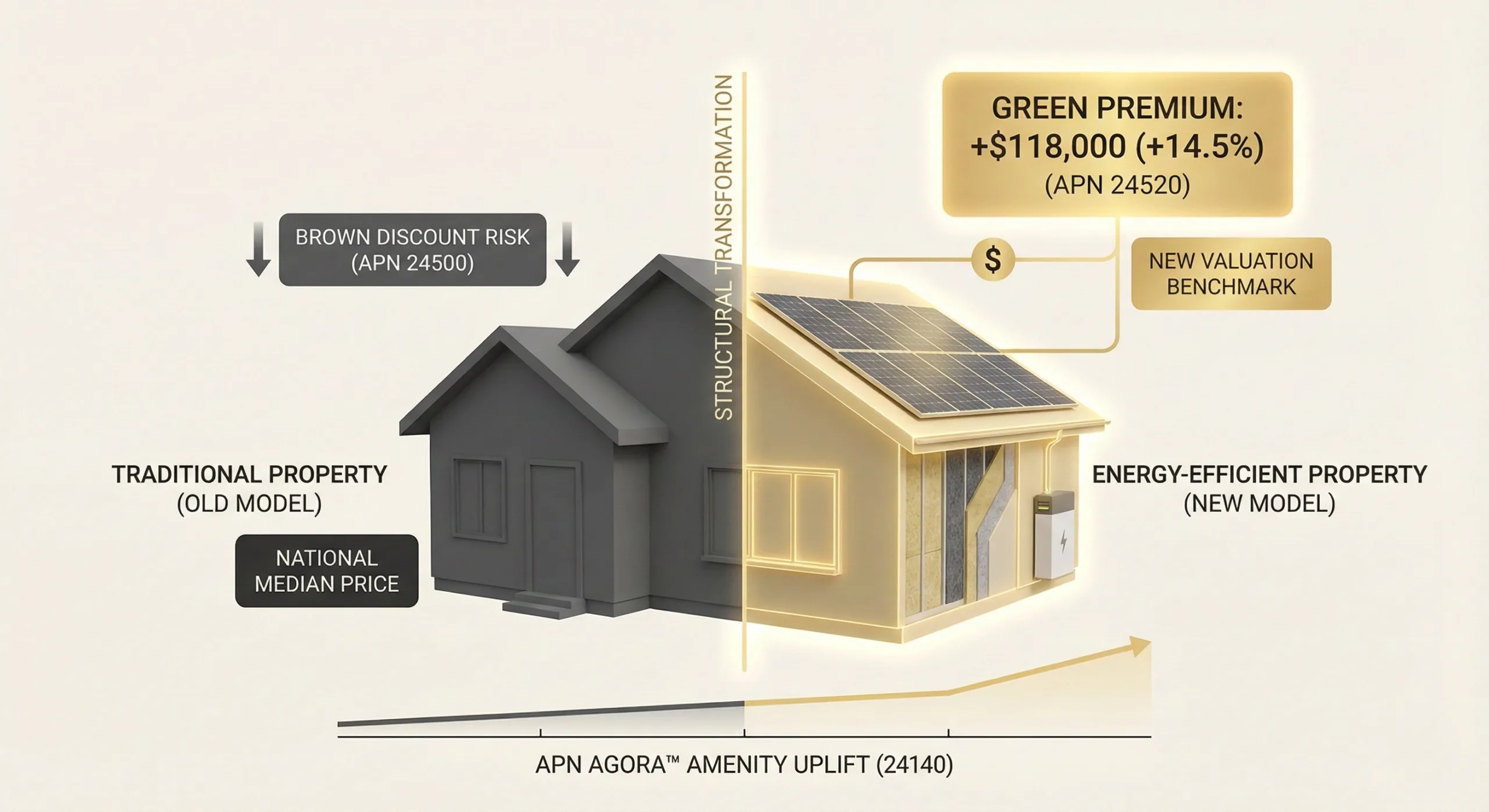

For property professionals, this dynamic represents a material, latent valuation risk. While legally compliant with frozen 2022 standards, this vintage of housing will lack the fundamental infrastructure for the 2030 net-zero transition, such as EV charging backbones and superior thermal performance. This will accelerate the shift from a ‘Green Premium’ to a ‘Brown Discount’, creating a material valuation discount for these assets in the secondary market. Lenders, valuers, agents, and future owners must now factor in this ‘Vintage Risk’, as the short-term cost savings of developers will become the long-term special levies of owners corporations.

Background & Strategic Context

This event validates the core thesis of the APN Sovereign Policy Composite Index™ (SPCI, 24800), which posits that top-down state intervention is the primary force shaping market boundaries and asset values. The government’s decision to prioritise immediate housing supply over long-term performance has directly re-engineered market incentives, creating a clear divergence in asset quality and future liability.

The Regulatory Floor as a Ceiling (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The October 2025 decision was not merely a delay but a strategic pivot, signalling to the industry that construction speed and cost reduction now supersede performance and future-proofing. By freezing the National Construction Code (NCC) for residential assets, the government has effectively established the 2022 7-star standard as both a floor and a ceiling, legitimising the production of technically outdated assets for a seven-year window.

The Viability Defence (APN Residual Land Value (RLV) Gap™): The persistent 3.85% cash rate has widened the APN Residual Land Value (RLV) Gap™ (24410), making previously planned ‘green’ features economically unviable for many build-to-sell projects. Developers are now deploying this ‘viability defence’ in modification applications, successfully arguing that features like EV readiness or high-performance glazing must be stripped to preserve project feasibility, a direct consequence of the high cost of capital.

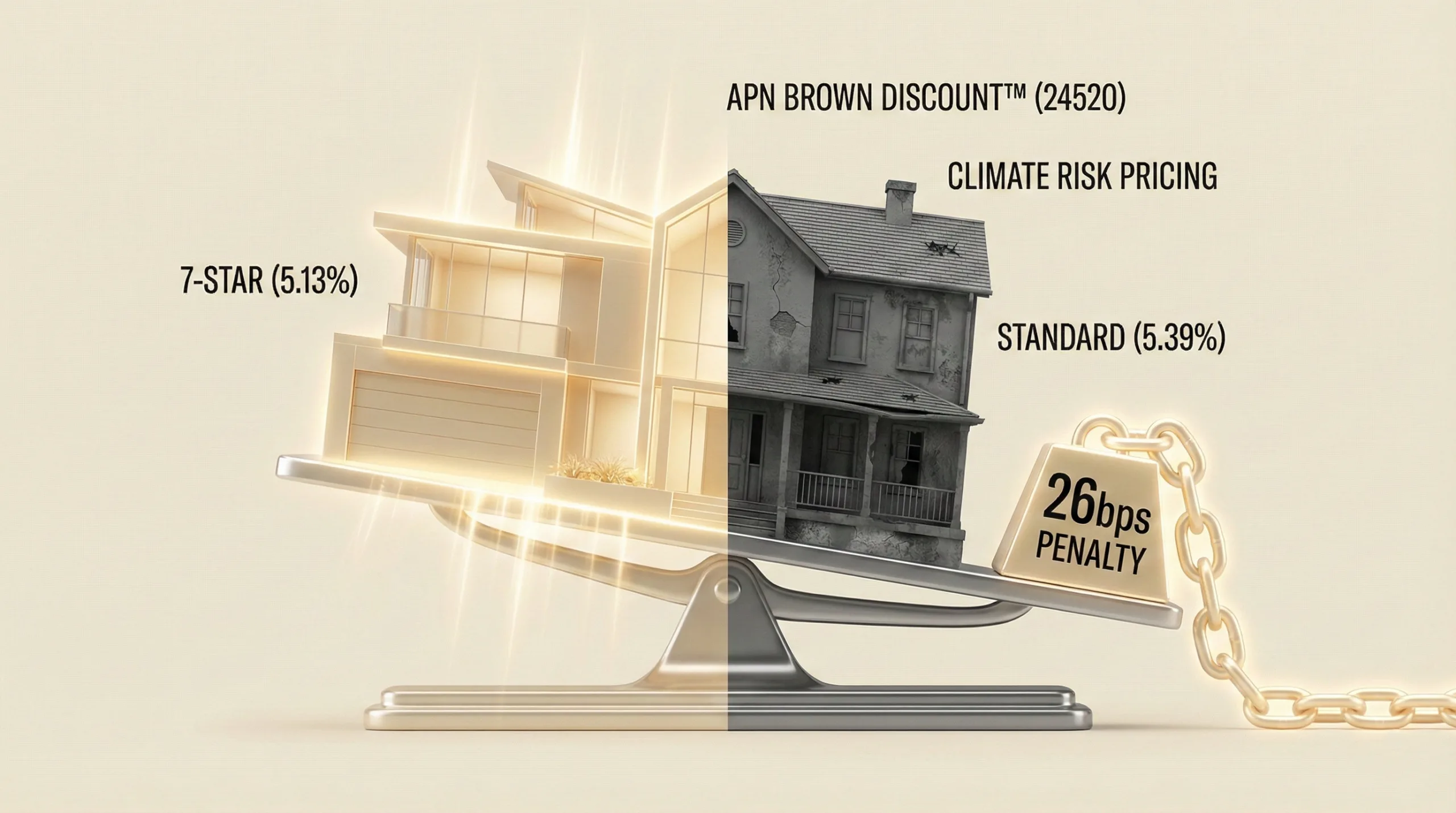

The Emergence of the Brown Discount (APN Climate-Risk Asset Devaluation Index™): The NCC 2025 creates a two-speed code, mandating solar and electrification readiness for commercial assets while pausing them for residential. This regulatory divergence is the primary catalyst for the materialisation of the APN Brown Discount™ (24520). It ensures that the 2026–2029 residential vintage will be structurally inferior, carrying a quantifiable financial liability when benchmarked against future-ready commercial stock and post-2029 residential assets.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the October 2025 Building Ministers’ Meeting communiqué, subsequent NCC 2025 preview documents, and observable market behaviour through state-level planning portals. The key facts are:

- The Regulatory Freeze: The Building Ministers’ Meeting of October 2025 mandated a pause on further increases to residential energy efficiency and EV charging provisions in the National Construction Code until mid-2029. The minimum standard remains the 7-star NatHERS rating from NCC 2022.

- The Commercial Divergence: In stark contrast, NCC 2025 introduces mandatory upgrades for commercial buildings (Class 3-9), including compulsory solar PV systems (minimum 65 W/m² of roof area) and provisions that support electrification readiness, legally compelling them toward a net-zero trajectory.

- The Financial Constraint: The Reserve Bank of Australia’s maintenance of a 3.85% cash rate has significantly increased construction financing costs, providing developers with a substantive ‘financial viability’ argument to justify the removal of non-mandated features.

- The Withdrawal Mechanism: Developers are systematically using state-based planning modification instruments, primarily Section 4.55 in NSW and Section 72 in Victoria, to legally strip ‘voluntary’ sustainability features from development approvals, a practice APN designates as ‘Voluntary Withdrawal’.

Critical Analysis & Balanced View

The ‘Compliance Ceiling’ presents a paradox: a policy designed to enhance housing affordability is creating a new generation of assets with inherent long-term financial liabilities. The ‘value engineering’ currently underway is not a bug but a feature of a system that prioritises short-term supply metrics over long-term asset performance. This process constitutes a direct transfer of risk from the developer’s balance sheet to the future owners corporation, which will inevitably face significant special levies to fund retrofits for electrification and energy efficiency.

While developers argue they are responding to a market where affordability trumps sustainability, this view is myopic. It ignores the inevitable repricing that will occur in the secondary market post-2029 when these assets are benchmarked against new, future-compliant stock. A clear bifurcation is emerging between the build-to-sell market, which is driving this trend toward minimum compliance, and the institutional build-to-rent sector. BTR operators, who hold assets long-term, are more likely to build above code to de-risk their portfolios and protect future income streams from the ‘Brown Discount’. The current modification volume is therefore an indicator that a high proportion of the pipeline is being optimised for developer exit, not for the end-user’s lifecycle cost.

Strategic Implications for Property Professionals

- For Developers: Differentiate or discount. While the mass market allows for minimum-compliance builds, the BTR sector and premium owner-occupier market offer an opportunity driven by capital reallocation toward lower-risk assets. Be prepared to evidence ‘above-code’ specifications as a core marketing pillar post-2025, or face being benchmarked against the structurally non-viable asset class.

- For Valuers & Lenders: Asset-level due diligence is now a primary consideration. Valuations for 2026–2029 vintage stock must begin pricing in a future ‘Brown Discount’ liability. Lenders must assess the long-term serviceability risk of assets that will inevitably face significant special levies for mandatory retrofits, impacting the financial stability of the owners corporation.

- For Agents & Buyers’ Agents: Educate your clients on ‘Vintage Risk’. A building’s completion date between 2026 and 2029 is an indicator requiring deeper investigation into its ‘future-readiness’, specifically the existence of EV charging infrastructure, solar generation, and thermal performance beyond the bare minimum NCC 2022 standard.

- For Strata Managers & Owners Corporations: Begin auditing the development history of any new building entering your portfolio. For any building completing post-2025, scrutinise the DA modification history for evidence of ‘Voluntary Withdrawal’. Proactively budget for future capital works related to electrification and energy efficiency, as these costs have likely been transferred from the developer to the owners.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the core tenets of the APN Climate-Risk Asset Devaluation Index™ (24500), confirming that regulatory divergence (APN Sovereign Policy Composite Index™ (SPCI, 24800)) is a primary catalyst for the materialisation of the APN Brown Discount™ (24520) in specific asset classes.

- Index Calibration: The APN Future Development Pipeline Index™ (24400) is calibrated to increase the weighting of the ‘Modification Application Velocity’ metric. This serves as a leading indicator of ‘Green Premium Erosion’ and quantifies the degradation in the structural integrity of the future supply pipeline.

- Data Capture: This triggers a new data capture mandate within the APN Symbiotic Intelligence Network™ (24310) to systematically track Section 4.55 (NSW) and Section 72 (VIC) applications that specifically reference the removal of energy efficiency, EV readiness, or solar infrastructure features from residential developments.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.