Validated: Brisbane’s Structural Land-Use Contest Creates Sustained Industrial Scarcity as Data Centres Displace Logistics Stock

APN ANALYSIS: A-260205-AUS136790

Executive Summary

Brisbane’s industrial market is experiencing a structural adjustment, not a cyclical downturn. APN analysis validates the ‘Structural Land-Use Contest’ thesis, where a convergence of demand from AI-driven data centres and e-commerce logistics has created a ‘Functional Scarcity’. This is not a simple lack of land, but a fundamental mismatch where available sites lack the high-power infrastructure modern occupiers require. This scarcity is structurally sustained by a negative APN Residual Land Value (RLV) Gap™, where construction costs have structurally exceeded market values, halting new speculative supply in the elevated-risk sub-2,000-square-metre asset class and creating a ‘buy over build’ imperative.

For property professionals, this signals a sustained recalibration of industrial asset valuation. The traditional metrics of location and floor area are being superseded by power capacity and grid connection speed. Assets with latent power potential are now a distinct, premium sub-class, while the ‘buy over build’ dynamic will intensify competition for existing stock, sustaining rental growth and forcing a strategic re-evaluation of every industrial portfolio.

Background & Strategic Context

This validation of Brisbane’s ‘Structural Land-Use Contest’ is not an isolated market event; it is a direct calibration of APN’s core macro-theses. It demonstrates the intersection of state-level economic drivers, the structural decoupling of construction economics, and the emergence of new, non-traditional demand vectors that are fundamentally reshaping asset utility and value.

The State-Level Impetus: The ‘Structural Land-Use Contest’ is a direct consequence of overlapping government priorities, as tracked by the APN Sovereign Policy Composite Index™ (SPCI, 24800). Federal and State initiatives promoting the digital economy are driving data centre demand, while record infrastructure spending and population growth are simultaneously driving logistics requirements and placing pressure on construction labour markets. These state-level forces are creating elevated, competing demands on a finite resource: serviced industrial land.

The Construction Constraint (APN Replacement Cost Gap™): Existing assets are currently trading at a 30% discount to their replacement cost. This financial inversion creates a ‘Yield Fortress’ around established stock, because the cost of new delivery is so much higher than the acquisition price of existing buildings, speculative development is economically irrational. This effectively halts the supply of new small- to mid-sized assets and forces capital to compete for existing, power-ready buildings.

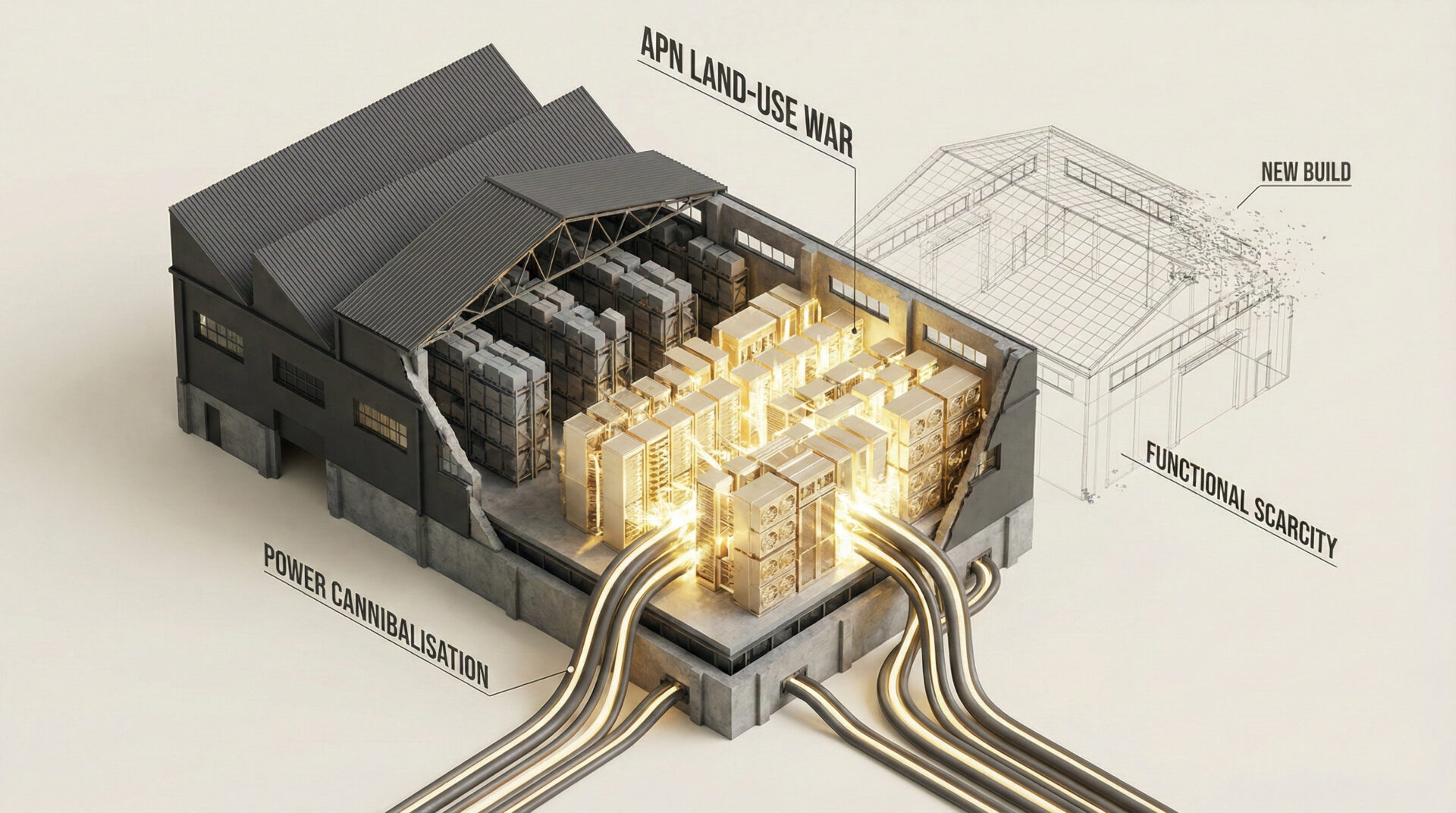

The Infill Squeeze (APN Infrastructure Uplift Multiplier™): The analysis confirms a substantive change in what constitutes ‘infrastructure’. The value multiplier is no longer just proximity to a motorway, but the availability of an 11kV+ power connection. This recalibrates the APN IUM™, identifying ‘Powered Land’ as the primary determinant of value and explaining why data centre operators can outbid logistics users for prime infill sites.

Deconstruction of the Source Event

This deconstruction is based on an internal APN intelligence briefing stress-testing the ‘Functional Scarcity’ thesis in the Brisbane industrial market. The key facts are:

- Vacancy Peak Exceeded: Brisbane’s industrial vacancy rate tightened to 3.4% in Q4 2025, outperforming the 3.6% forecast and sitting structurally below the 4.0% market equilibrium threshold, indicating structural undersupply.

- The ‘Serviced Land’ Illusion: Only 11% (approx. 738 hectares) of Brisbane’s 6,490 hectares of zoned industrial land is classified as ‘undeveloped and serviced’. High-demand infill precincts like the Trade Coast hold a materially low 11% share of this functional supply.

- The Replacement Cost Barrier: A structural 30% gap exists where the cost to build a new facility exceeds the market value of a comparable existing asset. This has entrenched a ‘buy-over-build’ strategy and made speculative development structurally static.

- Data Centre Displacement: ‘Edge’ data centres, requiring 500–2,000sqm footprints and high-megawatt power, are actively targeting and repurposing the same infill logistics assets, structurally removing them from the general supply pool.

- The Grid Friction Point: Grid connection delays of two to three years are now a standard project risk. This use of connection timelines as a strategic instrument makes sites with existing, active power connections a premium, immediately deployable asset class, bifurcating the market into ‘Powered’ and ‘Unpowered’ land.

Critical Analysis & Balanced View

The core insight from this analysis is a notable paradox: the grid friction point, which appears to be a brake on the ‘Structural Power Contest’, actually amplifies it. The multi-year delays in securing new high-capacity connections make existing ‘powered’ sites materially more valuable. This transforms the risk profile of industrial land acquisition. A site with a legacy 11kV connection from a former manufacturing use is no longer just a brownfield redevelopment; it is a strategic digital asset that allows an operator to bypass a three-year queue. This creates a significant value arbitrage opportunity that logistics users cannot compete with.

The balanced view must acknowledge that this dynamic introduces a new layer of risk. Investors acquiring unpowered land with the hope of a data centre rezoning or development are engaging in high-stakes speculation on grid policy and capacity upgrades. The primary source of lower-risk returns and alpha is the existing, often underestimated, stock of older industrial buildings in infill locations with grandfathered power rights. This is not just a Brisbane phenomenon; it is the strategic template for how the structural contest for infill industrial land will unfold across Sydney and Melbourne, where power constraints are even more concentrated.

Strategic Implications for Property Professionals

- For Investors & Fund Managers: The primary mandate is to audit portfolios for ‘Latent Power Capacity’. Assets previously valued on logistics metrics (e.g., hardstand, eaves height) must be re-assessed for their proximity to substations and existing kVA capacity. These ‘powered nodes’ are now a distinct asset class and must be valued accordingly.

- For Developers: Speculative development in the sub-2,000sqm infill market is financially unviable without a pre-commitment from a high-value tenant. The strategic shift is towards site amalgamation and securing power pre-approvals, effectively creating ‘Powered Land’ as the end product, rather than a completed building.

- For Agents & Buyers’ Agents: Due diligence must now include a ‘Power Audit’. Verifying grid connection capacity, load letters, and connection timelines is as essential as a building inspection. The ability to articulate the value of an 11kV connection will be the key differentiator in transacting high-value infill industrial assets.

- For Occupiers (Logistics): The environment of constrained alternatives is now structural. Lease renewal is the primary strategy. Relocation will involve significant compromises on location (moving to outer rings) or cost. Securing long-term tenure in powered, infill locations is a material supply chain advantage.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the core thesis of the APN Replacement Cost Gap™ (24450), confirming a structural halt to speculative supply. It also validates the recalibration of the APN Infrastructure Uplift Multiplier™ (APN IUM™) (24420) to prioritise power capacity over traditional transport connectivity.

- Index Calibration: The APN Future Development Pipeline Index™ (24400) is calibrated to more heavily discount zoned land that lacks confirmed, high-capacity power connections. The ‘serviced land’ filter will now be bifurcated into ‘Standard Serviced’ and ‘Power-Ready’ classifications to reflect the material value gap created by grid access.

- Data Capture: This triggers a new data capture mandate under the APN Symbiotic Intelligence Network™ (24310) to track and map all 11kV+ substations, known grid connection queues, and ‘grandfathered’ power rights within primary industrial precincts across Australia’s eastern seaboard.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.