RBA-APRA Coordination Accelerates Regulatory Velocity Multiplier and Concentrates Risk in Non-Bank Sector

APN ANALYSIS: A-251025-AUS37

Executive Summary

Coordinated preparation by APRA and the RBA for new macroprudential tools has materially increased the Regulatory Velocity Multiplier (RVM). The regulators’ shift from policy design to “implementation aspects” for tools like debt-to-income (DTI) limits is a high-confidence signal of latent regulatory risk that is currently being under-priced by the market.

This unified regulatory front, which creates a new causal link between RBA rate cuts and APRA intervention, will structurally concentrate risk in the non-bank sector. This “spillover effect” increases the systemic footprint of non-bank lenders and negatively impacts the APN Professional Sentiment Index™ (24300).

Background & Strategic Context

This coordinated regulatory preparation is a major financial stability signal, and its strategic implications are best understood through our core intelligence frameworks:

State-Led Intervention (Project Overlord) This is a core Project Overlord event. The RBA’s explicit endorsement of APRA’s preparatory work in its Financial Stability Review creates a unified regulatory front. This is a deliberate, coordinated state-level intervention designed to pre-emptively manage market stability and signal new “rules of the game” to regulated entities.

Regulatory Velocity (Project Cerberus Oz) The RVM mechanism here is subtle and significant. By focusing on “implementation aspects” before a crisis, the regulators are compressing the future timeline between a policy decision and its market impact. This operational readiness dramatically increases the speed and efficacy of regulatory velocity, which is a core theme of Project Cerberus Oz.

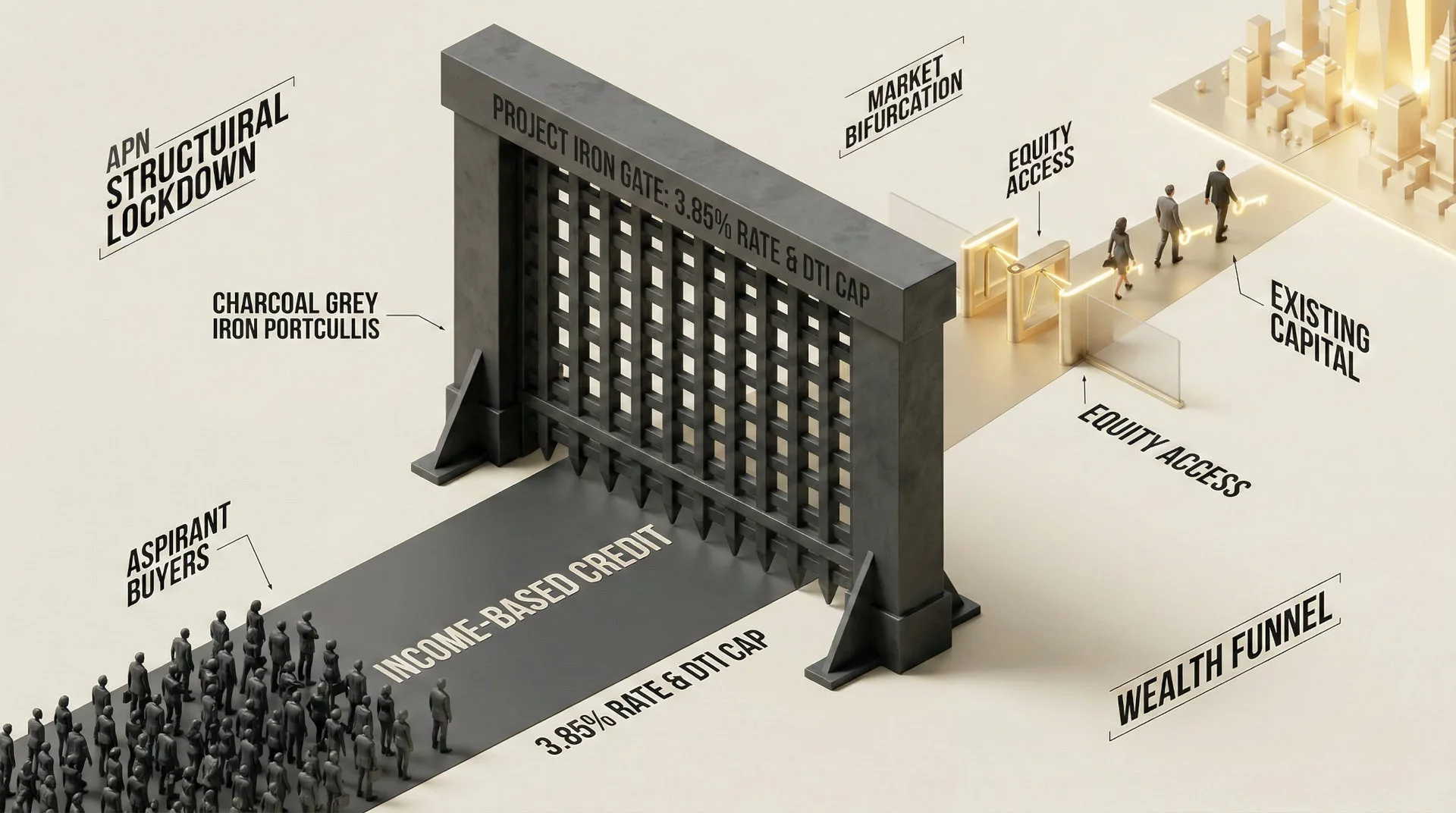

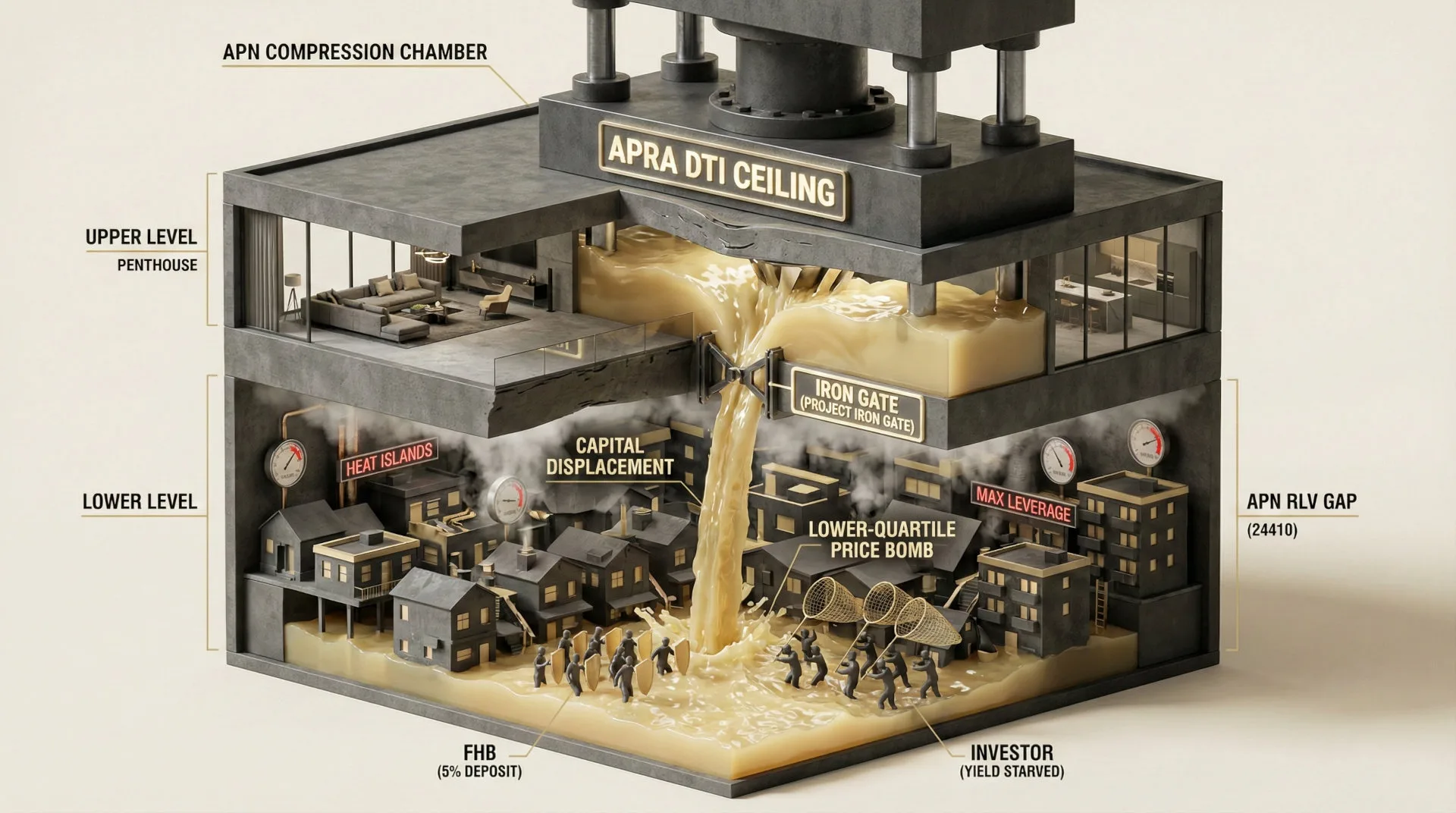

Risk Concentration (The Wealth Funnel) The confirmed “spillover effect” is a direct accelerant of The Wealth Funnel. Macroprudential tightening on banks will intentionally push higher-risk (high-DTI, investor) lending into the non-bank sector. This concentrates risk in less-regulated entities, increasing their vulnerability to shocks and ultimately strengthening the relative stability of the large incumbent banks.

Under-Priced Risk (APN Professional Sentiment Index™ (24300)) The intelligence identifies a significant market blind spot. Mainstream commentary is focused on the cash rate, while ignoring this latent regulatory risk. This disconnect creates a material, unpriced negative risk factor that must be recalibrated in the APN Professional Sentiment Index™ (24300).

Deconstruction of the Source Event

This deconstruction is based on an internal APN intelligence briefing. The key facts are:

- APRA is “engaging with regulated entities on implementation aspects” of new macroprudential tools, signalling a move to operational readiness.

- The RBA explicitly endorsed this preparatory work in its October 2025 Financial Stability Review (FSR).

- The targeted tools include limits on new high debt-to-income (DTI) and investor/interest-only loans.

- The RBA FSR notes “early signs that high DTI lending has started to pick up.”

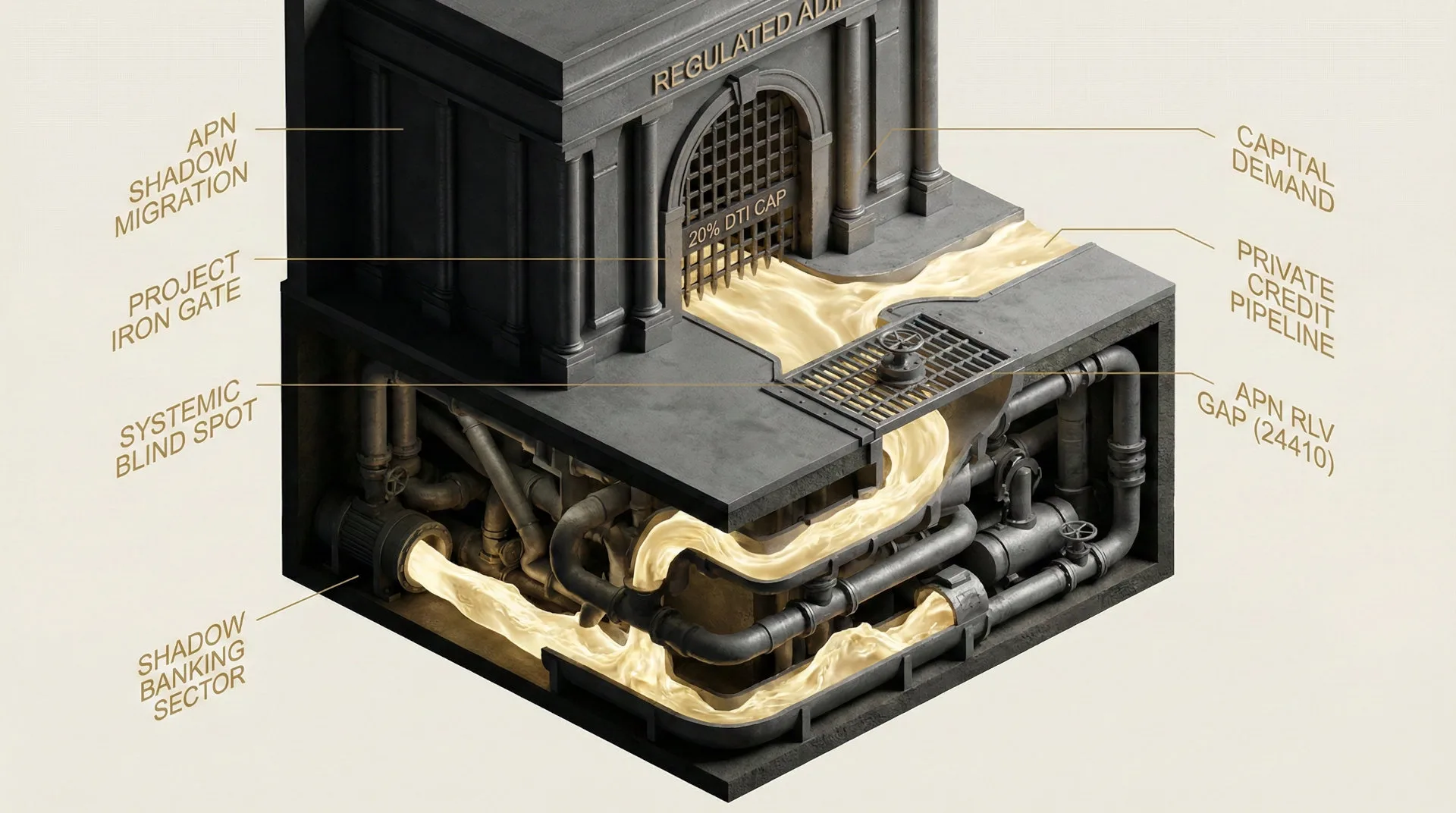

- International and RBA analysis confirms that tightening on banks drives higher-risk credit toward the non-bank (NBFI) sector (the spillover effect).

- The current absence of specific analysis from major bank economists on this “engagement” signal confirms it is an under-priced, latent risk.

Critical Analysis & Balanced View

The “real” story is the new causal link between monetary and macroprudential policy. The market must now understand that the probability of APRA intervention is inversely correlated with RBA rate cuts. As market expectations for monetary easing (rate cuts) increase, so too must the priced-in probability of APRA intervention to manage the subsequent credit growth.

- Risk Concentration is a Feature, Not a Bug: The spillover effect is the intended mechanism. It will concentrate vulnerable, high-DTI and investor borrowers in the less-regulated non-bank sector, which increases the NBFI sector’s systemic risk footprint and vulnerability to credit shocks.

- The Non-Bank Dilemma: Non-bank lenders face a strategic dilemma. Actively absorbing these spillover loans to gain short-term market share will, by definition, accelerate their growth into the “systemically important” category, which in turn accelerates the timeline for future, direct regulatory intervention against them.

Balanced View: On the surface, this appears to be a routine, preparatory engagement by regulators. However, the analysis reveals it as a sophisticated, coordinated signal of a new policy framework. By pre-loading the “implementation” phase, regulators have increased the RVM and created a material, unpriced risk for a market that is solely focused on the cash rate. This guarantees that future risk will be concentrated in the non-bank sector.

Strategic Implications for Property Professionals

- For Lenders & Investors (Risk Modelling): All forecasting scenarios for RBA rate cuts must now automatically trigger a higher probability weighting for APRA intervention. The two policies are now explicitly interdependent.

- For Non-Bank Lenders: You face a critical strategic dilemma: chasing short-term market share by absorbing high-DTI “spillover” loans will accelerate your growth into a “systemically important” category, guaranteeing future, direct regulatory oversight.

- For Valuers & Sentiment Analysts: The APN Professional Sentiment Index™ (24300) must be recalibrated to assign a higher negative weighting to these preparatory signals, as they represent a significant latent risk that is currently being ignored by the market.

- For All Professionals (Monitoring): Focus must escalate to the rate of change (velocity) of investor credit and high-DTI loan origination. The RBA has clearly identified these metrics as the primary lead indicators that will trigger future regulatory action.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

Property values and market conditions can go down as well as up.

Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.