The Serviceability Shield: Logan’s 12-Week ‘Backyard Pivot’ Validated as a Rapid Response Mechanism to Material RBA Rate Adjustments

APN ANALYSIS: A-260207-AUS136975

Executive Summary

The Reserve Bank of Australia’s February 2026 decision to lift the cash rate to 3.85% has triggered a structural adaptation in the residential property market, creating concentrated fiscal stress for mortgaged households. This has validated the APN ‘Backyard Pivot’ thesis, where the primary residence must be repurposed as active ‘Income Infrastructure’ to ensure serviceability. Our analysis confirms the ‘granny flat’ has evolved from a passive dwelling into a ‘Serviceability Shield’, a financial firewall designed to neutralise the repayment increase of $198–$212 per month for a median Sydney home.

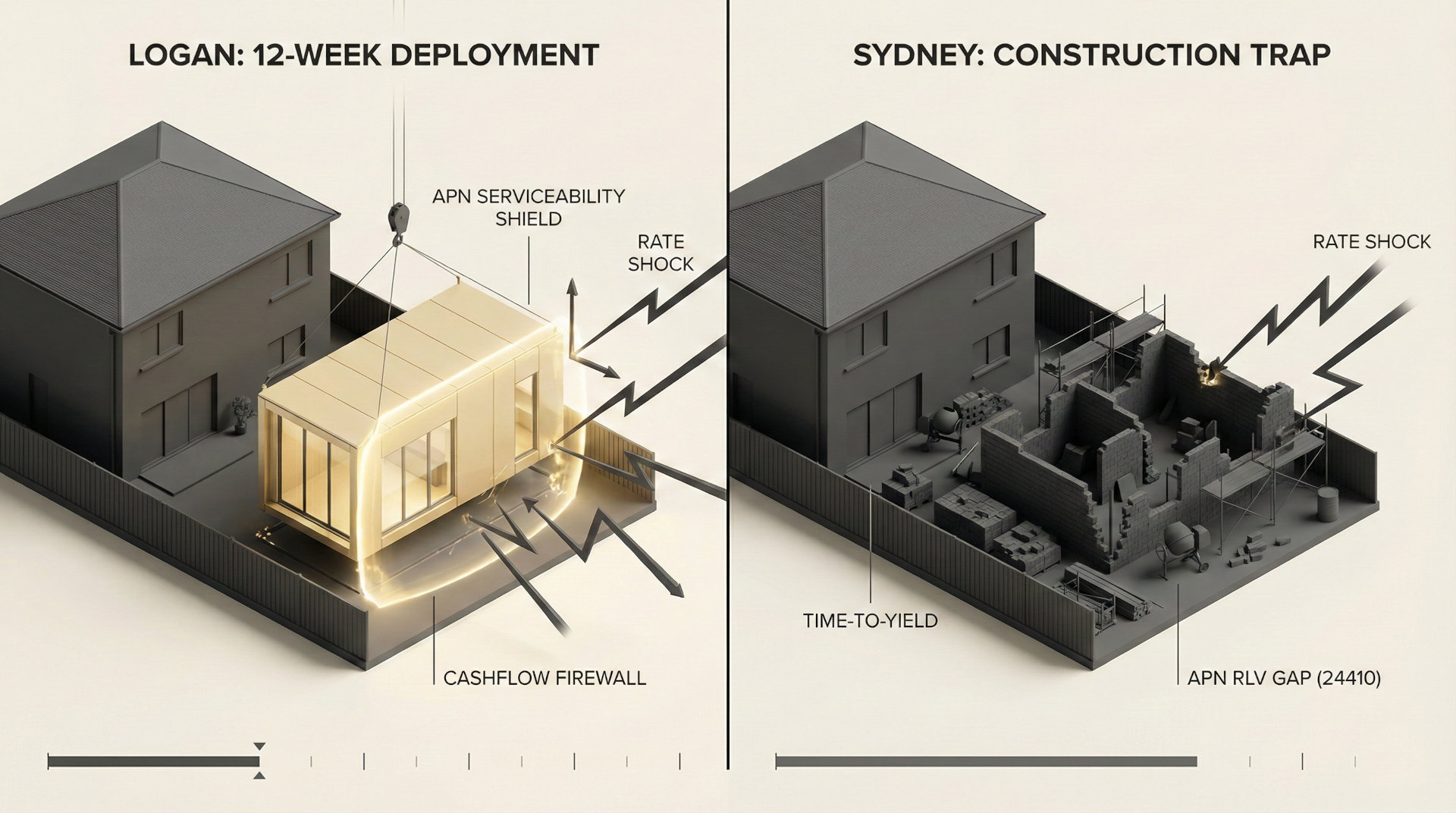

For property professionals, this trend is not about speculative investment but about identifying viable, high-velocity cash flow solutions for clients facing default. The primary metric is no longer gross yield but ‘Time-to-Yield’. This exposes the ‘Construction Trap’ inherent in Sydney’s 9-month custom-build pathway, which poses a significant liquidity risk. Conversely, it validates the Logan/Ipswich modular strategy, where a 12-week deployment timeline provides the immediate fiscal relief required in a scenario of acute affordability constraint, making it a more rapid fiscal mitigation mechanism.

Background & Strategic Context

This event validates and calibrates two core APN macro-theses. The RBA’s hawkish turn provides a clear example of Project Iron Gate, where regulatory-driven serviceability constraints physically decouple borrowers from refinancing options, forcing them to seek internal liquidity. Concurrently, the starkly different outcomes in Queensland and New South Wales are a direct function of state-level intervention, confirming the primacy of the APN Sovereign Policy Composite Index™ (SPCI, 24800) in shaping market viability.

The Iron Gate Effect (APN Credit Rationing Index™): The RBA’s rate hike has pushed assessment rates to 9.5%, creating a “Serviceability Shield” requirement. Investors must now prioritise high-velocity cash flow strategies to bypass the credit rationing that has left standard borrowing capacity structurally static.

The Velocity Arbitrage (APN Regulatory Velocity Multiplier™): The “QLD Accepted Development” pathway represents a material reduction in regulatory friction. By utilising these code-assessable provisions, investors can execute a “12-Week Speed-to-Yield” strategy, bypassing the 12-month DA delays that materially compromise project viability in a high-rate environment.

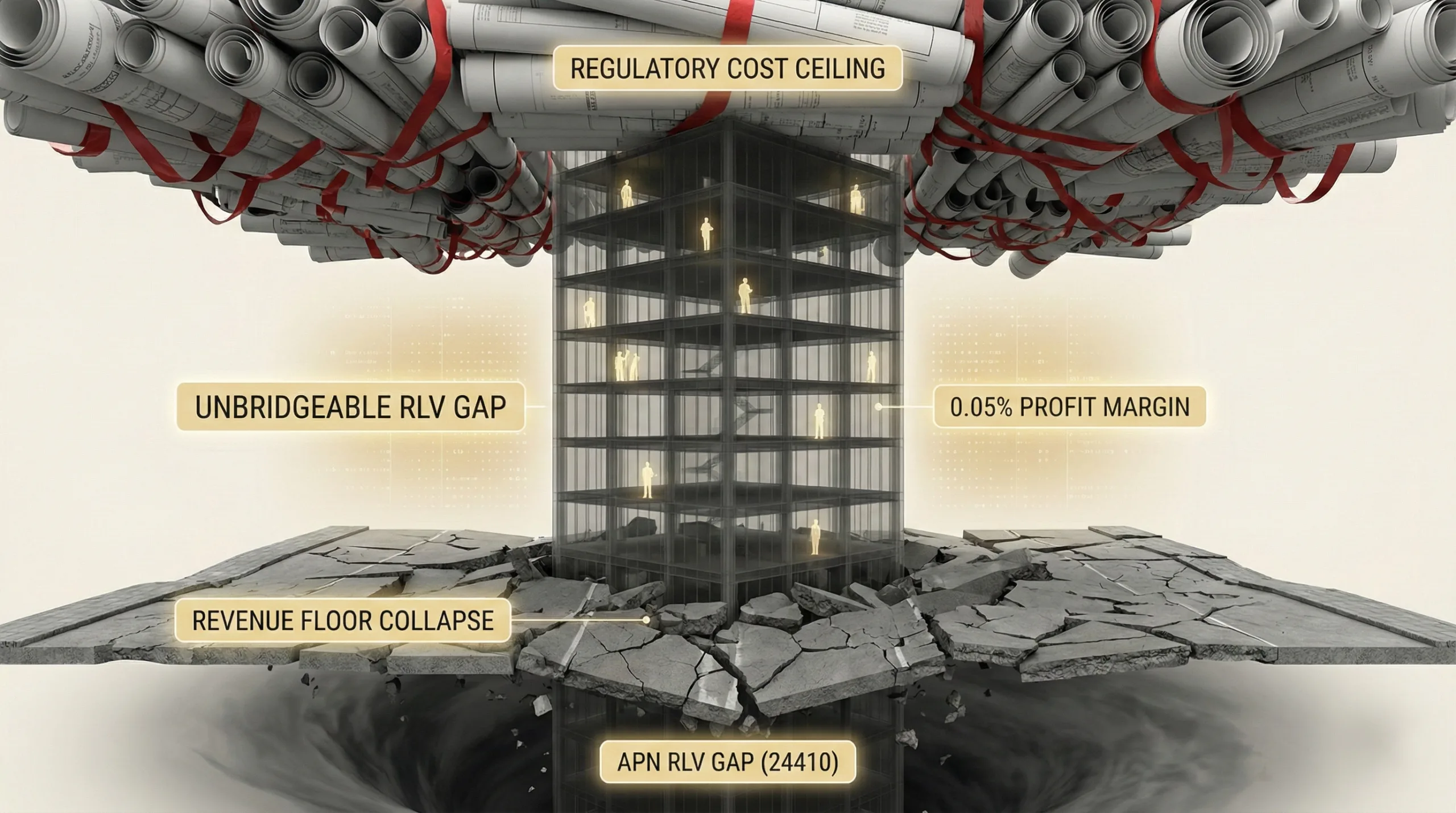

Escaping the Insolvency Zone (APN Replacement Cost Gap™): Traditional “vertical” development is currently constrained by “The Construction Trap” due to the negative equity moat. The “Backyard Pivot” (Granny Flats/Dual Occ) is the only asset class that remains below the replacement cost threshold, allowing for profitable deployment of capital while major projects are constrained.

State-Level Intervention (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The divergence between Federal monetary tightening (The Material Rate Adjustment) and State planning deregulation (Accepted Development) creates a temporary window of opportunity. Strategically positioned capital is utilising this “Intervention Gap” to manufacture yield before the regulatory window potentially closes or costs rise further.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the RBA’s February 2026 monetary policy decision and its transmission into household balance sheets. The key facts are:

- Monetary Policy Shift: On 3 February 2026, the RBA raised the official cash rate by 25 basis points to 3.85%, signalling an end to the preceding period of stability and citing persistently high inflation as the primary driver.

- Repayment Increase Quantified: The rate hike was immediately passed on by major lenders, resulting in a direct monthly repayment increase of $198–$212 for a median-priced house in Sydney and approximately $149 in Brisbane.

- Credit Contraction: The hike triggered an immediate reduction in borrowing capacity of approximately $12,000 for an individual on an average full-time wage, materially constraining the ability of existing borrowers to refinance their loans.

- Regulatory Arbitrage: A notable divergence exists in state planning laws. Queensland allows secondary dwellings to be rented to non-relatives and classifies compliant builds up to 100m² as ‘Accepted Development’ in corridors like Logan, requiring no formal DA. NSW permits non-relative rentals but its CDC pathway is more restrictive (60m² cap, stricter setbacks) and subject to significant council contributions ($11.5k–$15k in Blacktown).

Critical Analysis & Balanced View

The surface-level data presents a ‘Yield Paradox’. The Blacktown corridor offers a marginally higher gross yield (13.3%) compared to Logan (12.9%). For a borrower facing acute affordability constraints, however, this gross yield metric does not adequately reflect the underlying structural constraint of ‘Time-to-Yield’. The primary, determining variable is ‘Time-to-Yield’. The 9-month completion lag for a typical custom-build in Western Sydney constitutes a ‘Construction Trap’. During this period, the borrower must service their primary mortgage, now inflated by the rate hike, *plus* the interest on their construction loan (~$1,343/month), all without any offsetting rental income. This nine-month cash-burn phase of over $12,000 in sunk interest costs exacerbates, rather than relieves, fiscal stress and can trigger insolvency before the asset is ever completed. (the $12,000 sunk interest cost assumes a standard construction loan interest rate of ~6.5%.)

In stark contrast, the Logan modular strategy’s 12-week (3-month) deployment timeline is its defining strategic advantage. The ‘Serviceability Shield’ is activated within a single fiscal quarter. The higher infrastructure charge in Logan (~$28k vs ~$15k) is a secondary consideration; the total turnkey cost remains lower than a Sydney custom build due to factory efficiencies. For a household managing the depletion of its savings, the velocity of cash flow from the Logan strategy is the primary determinant of viability. It transforms the secondary dwelling from a high-risk construction project into a rapid-deployment financial firewall.

Strategic Implications for Property Professionals

- For Mortgage Brokers & Financial Advisors: The ‘Backyard Pivot’ is now a primary tool for client retention and default management. Your role must evolve from simply sourcing a lower rate to structuring a viable capital and cash flow solution. The Logan modular strategy should be your primary recommendation for clients in concentrated fiscal distress due to its speed-to-yield.

- For Developers & Builders: The market is bifurcating. In Sydney, the viable model is high-friction, high-margin custom builds for clients with deep liquidity. In South East Queensland, the structurally advantaged model is high-velocity, standardised modular construction targeting the distressed homeowner market. Your supply chain and methodology must align with the target corridor’s regulatory framework to remain competitive.

- For Agents & Buyers’ Agents: Your property appraisals must now include a ‘Yield Potential’ audit. A Logan property with a flat, accessible backyard is fundamentally more valuable to a serviceability-constrained buyer. Conversely, when advising on a Blacktown property, you must quantify the ‘Construction Trap’ risk, including the 9+ month income lag and significant holding costs.

- For Property Managers: Prepare for accelerated growth in the volume of high-quality, new-build secondary dwellings entering the rental market in key mortgage-belt corridors. This will establish a new premium for modern, self-contained units while placing downward pressure on rents for older, B-grade rental stock in the same areas.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the APN Credit Rationing Index™ (24230) by demonstrating the material impact of contracting borrowing capacity, which forces the ‘Backyard Pivot’. It also validates the APN RLV Gap™ (24410) as a primary filter for development viability, highlighting how construction cost inflation and regulatory friction render the Blacktown strategy unviable for borrowers facing acute affordability constraints.

- Index Calibration: The APN Regulatory Velocity Multiplier™ (APN RVM™) (24210) will be calibrated to weigh ‘Time-to-Yield’ as a primary friction metric. The Logan ‘Accepted Development’ pathway will receive a low friction score, while the Blacktown CDC pathway, with its associated lags and contributions, will receive a high friction score.

- Data Capture: This triggers a new data capture mandate for the APN Symbiotic Intelligence Network™ (24310) to track turnkey costs, build times, and rental yields for secondary dwellings specifically within the Blacktown and Logan-Ipswich corridors, differentiating between modular and custom-build methodologies.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.