‘Commuter Cliff’ Creates Structural Solvency Pressure in 90-Minute Belt

APN ANALYSIS: A-260122-AUS135035

Executive Summary

A structural solvency pressure point, termed the “Commuter Cliff,” is evident across Australia’s eastern seaboard commuter belts. APN analysis confirms that the convergence of rigid five-day return-to-office (RTO) mandates and a sustained high interest rate environment has resulted in a “Double Cost Shock” for a specific cohort of households. The reintroduction of non-discretionary commuting costs, estimated at $15,000-$29,000 annually, is systematically reducing serviceability buffers that were already depleted by the 2022-2025 monetary tightening cycle. This is not a generalised market event; it is a geographically concentrated structural pressure point affecting the “90-minute belt”, specifically Geelong, the Central Coast, and Wollongong, where households that relocated during the work-from-home era are now in technical default.

For property professionals, this analysis is a directive to look beyond national averages that do not adequately reflect underlying structural constraint. The “Commuter Cliff” creates a two-speed market defined by a resilient, well-connected inner-core and a structurally exposed, car-dependent periphery. This geographic decoupling presents both concentrated risks and distinct opportunities. Professionals should now apply hyper-local due diligence, quantifying the “RTO Tax” for clients in these corridors, preparing for an increase in distressed listings, and recalibrating valuation models to account for a new, potent variable: transport reliability. Operational success in this environment is contingent on identifying and pricing this new layer of geographically-specific risk.

Background & Strategic Context

This event validates and calibrates APN’s core macro-theses, demonstrating how state-level interventions directly create divergent economic outcomes and stratify the market. The “Commuter Cliff” is not a random market fluctuation but a predictable outcome of specific policy and infrastructure failures, the effects of which are now being priced into the property market in real-time.

A State-Level Intervention (APN Sovereign Policy Composite Index™): The simultaneous enforcement of rigid RTO mandates by major corporate and government employers represents a substantive, non-legislative state-level intervention. This action, a core focus of the APN Sovereign Policy Composite Index™ (SPCI, 24800), has redrawn the boundaries of economic viability for residential property, effectively imposing a significant financial constraint on peripheral locations and materially reducing the value proposition that drove the WFH-era relocation boom.

A Mechanism of Financial Pressure: This structural pressure point illustrates a mechanism where incumbent, high-equity asset holders in inner-urban areas with diverse transport options are insulated from the impact. In contrast, the financial pressure is concentrated on highly-leveraged, more recent market entrants in the commuter belt, whose financial model was predicated on a WFH cost subsidy that has now been unilaterally withdrawn.

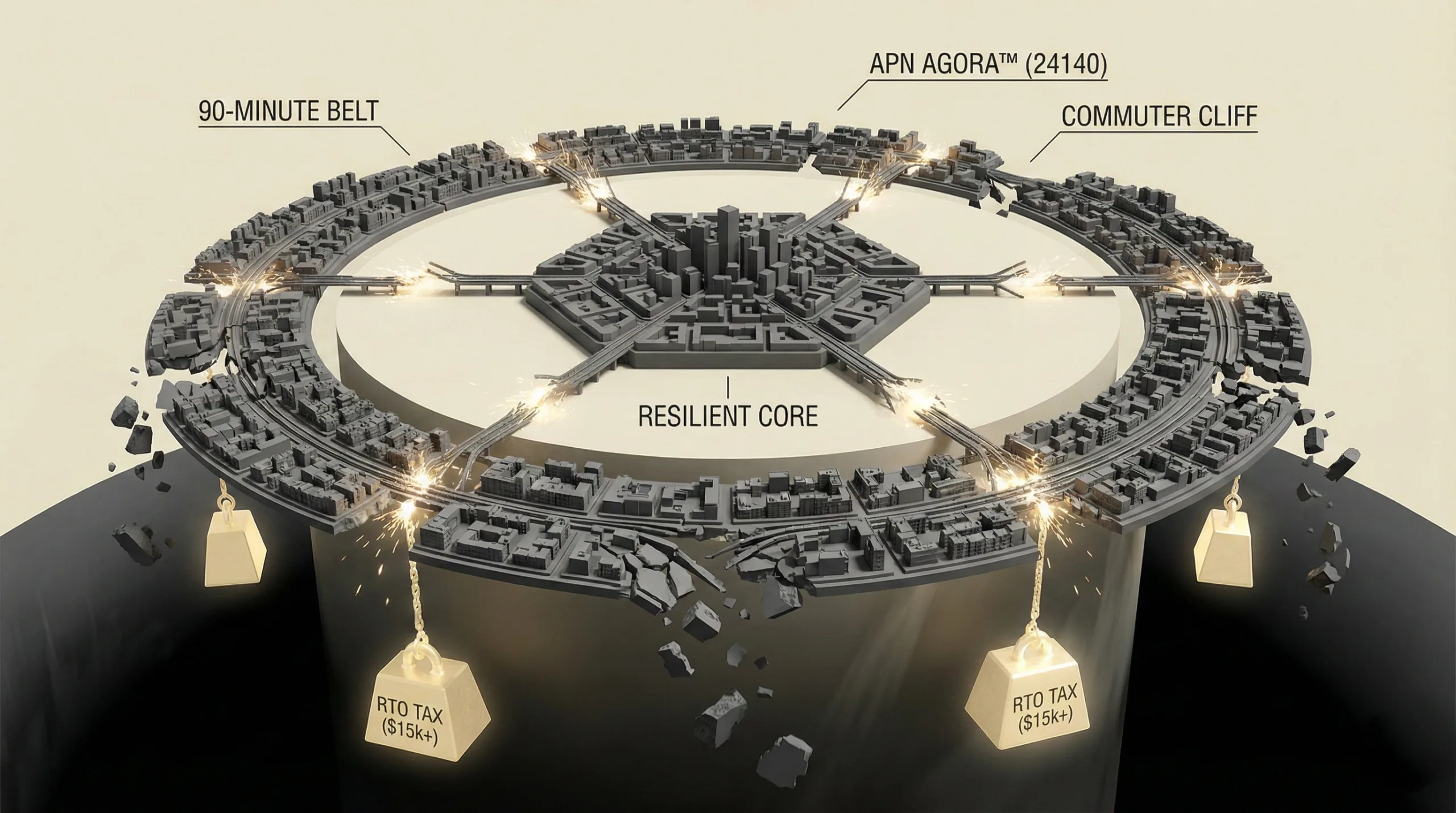

An Infrastructure Failure Catalyst (APN Agora™): The systemic failure of the intercity rail network is the material catalyst that transforms the RTO mandate into a financial pressure point. This failure, a negative calibration of the APN Agora™ (Amenity & Access Index), negates public transport as a viable alternative, forcing a higher-cost substitution to private vehicles. The unreliability of this core infrastructure directly triggers the full financial impact of the “RTO Tax” on exposed households.

Deconstruction of the Source Event

This deconstruction is based on an internal APN intelligence briefing synthesising credit performance audits, transport cost indices, and distressed property listings for January 2026. The key facts are:

- The “Double Cost Shock”: The convergence of rigid 5-day RTO mandates and a sustained 4.10% cash rate has created a solvency pressure point for households in the “90-minute belt” (Geelong, Central Coast, Wollongong), whose mortgage serviceability was calculated in a WFH context.

- The “RTO Tax” Quantified: The mandated return to a 5-day commute imposes a net new annual household expense of approximately $15,891. This post-tax cost requires an additional $23,500 in gross income to fund, effectively acting as a 10-15% pay cut and nullifying any standard salary increases.

- The Arrears Divergence: While national prime mortgage arrears are falling (to 1.13%), loans originated in 2023, a proxy for the “Commuter Cliff” demographic, are recording arrears at more than double the historical average (1.2% arrears vs 0.5% average). This confirms a clear decoupling in credit quality between the resilient core and the structurally exposed periphery.

- The Rail Substitution Failure: Sustained operational failures on key intercity rail lines, with on-time running on the Central Coast and Newcastle line dropping as low as 35%, have rendered public transport an unviable alternative. This forces commuters into cars, directly exposing them to the full, structurally adverse financial impact of the “RTO Tax”.

Critical Analysis & Balanced View

The most significant insight is the emergence of a “Macro-Resilience Facade.” Aggregate data, such as falling national arrears and strong demand for Residential Mortgage-Backed Securities (RMBS), presents a view that does not adequately reflect a structurally sound market. This high-level stability, driven by seasoned loans in prime metropolitan areas, obscures the concentrated, geographically-specific solvency pressure point developing in the 90-minute belt. This is not a cyclical downturn but a structural decoupling of the Australian property market into two distinct entities: a resilient core and a structurally exposed periphery.

The paradox is that the structural pressure point is catalysed by a failure of public infrastructure. The inability of the state to deliver reliable transport, a fundamental component of the social contract for commuter regions, directly translates into a material financial constraint for the households that planners encouraged to move there. This reduces not just household equity but also social capital and trust in public institutions, a key metric tracked by the APN Bedrock™ index. Furthermore, a secondary risk is the second-order impact on local economies within these commuter zones. As household disposable income is reallocated to fund commutes, local small business revenues will decline, amplifying the initial impact and creating a self-reinforcing structural condition.

Strategic Implications for Property Professionals

- For Agents & Buyers’ Agents: Macro-level market reports are now not sufficiently granular. The value proposition is now contingent on hyper-local due diligence. You should quantify the ‘all-in’ holding cost for clients considering commuter belt properties, including a realistic “RTO Tax” calculation. Listing agents in these zones should prepare for an increase in distressed sales and manage vendor expectations accordingly.

- For Valuers & Lenders: Standard valuation models and credit risk assessments should be updated to include a “Commuter Dependency” risk factor. Loan-to-value ratios and serviceability buffers for properties in transport-poor, car-dependent outer suburbs require a specific, negative adjustment to reflect the volatility of the “RTO Tax” and the recorded underperformance of the “Vintage 2023” loan cohort.

- For Developers: The “work-from-home” premium for peripheral greenfield developments has materially reduced and has inverted into a structural liability. Future project viability in the 90-minute belt is now contingent on either genuine, high-reliability transport connectivity (APN Agora™) or the integration of significant local employment hubs to reduce commuter dependency.

- For Property Investors: The strategy of buying in the commuter belt is under elevated pressure, with investor capitulation already evident in markets like the Central Coast. Yields are unlikely to cover elevated mortgage costs, and the risk of capital loss is elevated in the short-to-medium term. Focus must shift to assets within resilient local economies with diverse and reliable transport options.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides validation for the “Geographic Decoupling” hypothesis within the APN Sovereign Policy Composite Index™ (SPCI, 24800), where state-level policy (RTO mandates) and infrastructure failure combine to create distinct, divergent economic outcomes for different property market segments.

- Index Calibration (APN Agora™ 24140): The APN Agora™ (Amenity & Access Index) is recalibrated to increase the weighting of ‘transport reliability’ over mere ‘transport availability’. The sustained failure of the CCN rail line demonstrates that the existence of infrastructure is not functionally material if its operational performance falls below a functional threshold, converting it from an asset to a liability.

- Index Calibration (APN Bedrock™ 24110): The APN Bedrock™ (Social Cohesion Analysis) for postcodes 3220, 2259, and 2500 will be downgraded. The observed conversion of mortgage stress into forced sales indicates a material deterioration in community-level financial resilience and social stability, key inputs for the index.

- Data Capture: This event triggers a new data capture mandate under the APN Symbiotic Intelligence Network™ (24310) to track ‘distress-related’ keywords (e.g., ‘mortgagee in possession’, ‘forced sale’, ‘motivated seller’) in property listings on a postcode-by-postcode basis, creating a real-time ‘Forced Sale Heat Map’.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.