Australia’s ‘Golden Plateau’: How Rate Stability is Structuring a Market of Constrained Households

APN ANALYSIS: A-260119-AUS134872

Executive Summary

The Australian housing market is entering a strategic phase defined by the “Golden Plateau”, a period of sustained interest rate stability with the cash rate projected to remain around 3.6% through 2026-2028. Contrary to expectations that stability would foster market fluidity, it is architecting a structurally constrained society. This phenomenon is driven by a convergence of positive real interest rates, material macroprudential guardrails, and unindexed transaction taxes, which create a level of “Systemic Friction” that decouples housing asset values from their utility. The result is a portability structural pressure point, where the all-in cost of moving house now exceeds the financial capacity of the median household, transitioning the market from a dynamic system of upgrading and rightsizing to a static regime of asset accumulation.

For property professionals, this paradigm shift signals a structural decline in transaction volumes, directly impacting commission-based revenue models. The market is bifurcating into a small, fluid pool of cash-rich buyers and a vast, immobile majority of structurally constrained mortgage holders. The strategic focus must pivot from facilitating high-velocity sales to providing high-value advisory services for complex situations, such as navigating downsizer tax implications, unlocking equity for renovations, and identifying niche development opportunities in affordable market segments. Success in the Golden Plateau era will be defined not by sales volume but by the ability to solve the challenges of immobility.

Background & Strategic Context

This event validates and calibrates APN’s core macro-theses, demonstrating how state intervention is reshaping market dynamics and socio-economic outcomes. The emergence of the structurally constrained society is not an accidental market failure but a direct consequence of policy choices designed to prioritise systemic financial stability over the efficient allocation of housing stock. The resulting friction creates a market defined by who can transact, rather than what is for sale.

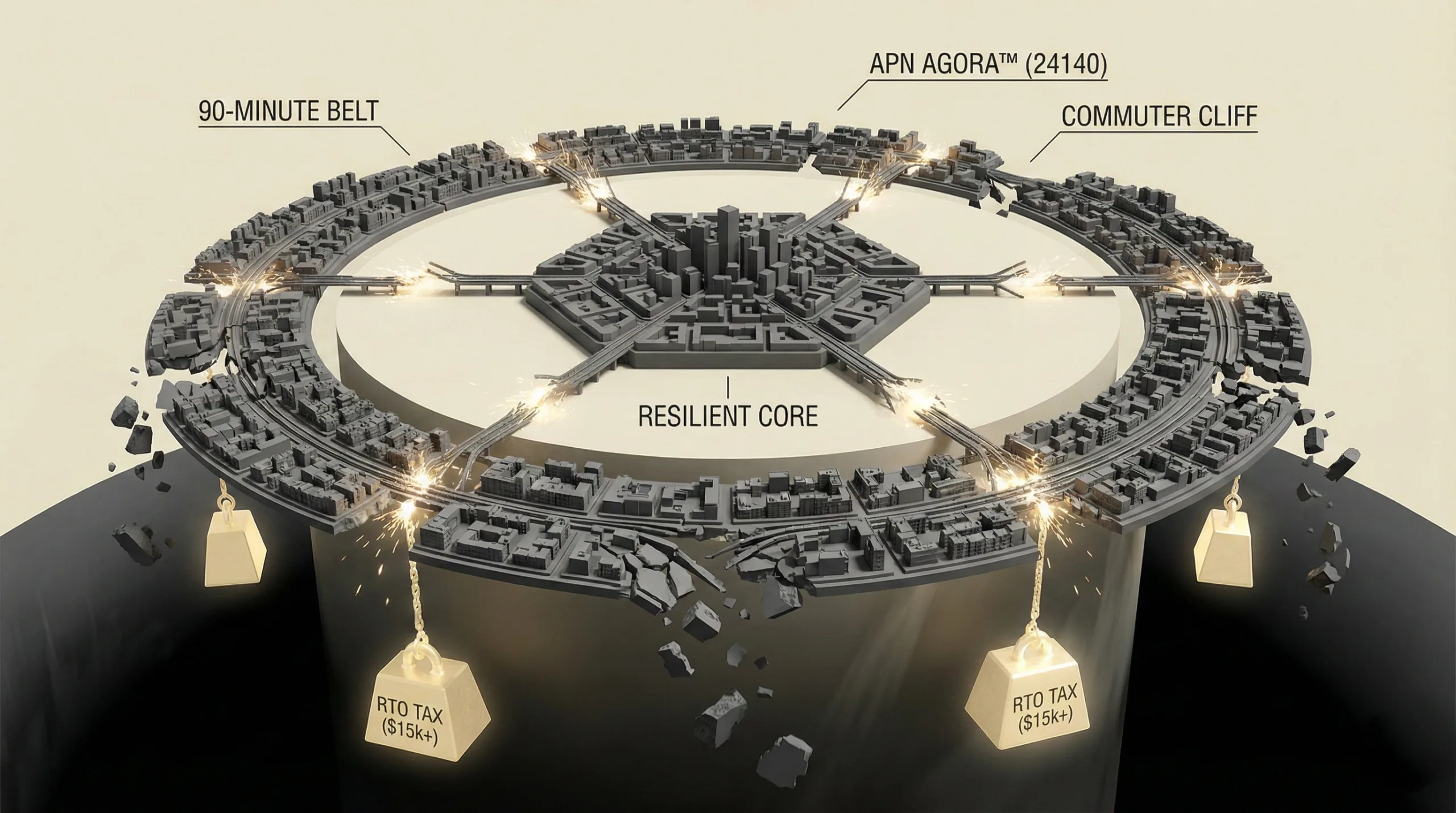

A Case Study in State-Level Market Architecture (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The convergence of the RBA’s monetary policy, APRA’s macroprudential framework (the 3% buffer and DTI caps), and state governments’ fiscal reliance on stamp duty is a clear demonstration of how state actors collaboratively define the boundaries of market activity. These interventions have collectively raised the cost of mobility to prohibitive levels, creating the portability structural pressure point.

A Material Amplifier of Incumbent Asset Holder Advantage: The “Golden Plateau” crystallises the gains of previous cycles for incumbent asset holders while making that wealth illiquid. By constraining existing owners in unsuitable housing and simultaneously excluding potential upgraders from the market, the policy framework concentrates the benefits of housing wealth with cohorts that entered the market in earlier, low-friction eras, exacerbating intergenerational wealth inequality.

A Prioritisation of Stability over Liquidity (APN Risk & Compliance Index™ (24200)): APRA’s explicit decision to maintain its restrictive credit guardrails, despite evidence of them suppressing market turnover, underscores the regulator’s strategic intent. This action signals a long-term risk posture focused on de-leveraging the household sector, even at the cost of material allocative inefficiency in the housing market, an elevated risk vector tracked by this index.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the projected 2026-2028 macroeconomic landscape and its impact on housing market portability. The key facts are:

- The “Golden Plateau”: The RBA Official Cash Rate is forecast to stabilise in a band around 3.6% through 2026-2028. This establishes a “new normal” for standard variable mortgage rates of approximately 6.0% to 6.5%, ending the era of low-cost credit that previously subsidised high transaction costs.

- The 3% Serviceability Buffer: APRA has maintained the 3% serviceability buffer, requiring lenders to assess a borrower’s repayment capacity at a theoretical interest rate of ~9.5%. This creates a large cohort of structurally constrained mortgage holders who can service their existing debt but cannot pass the stress test to refinance or move.

- The Debt-to-Income (DTI) Cap: Effective February 2026, APRA has implemented a hard limit restricting high DTI (greater than 6x) lending. This policy acts as a structural ceiling on borrowing capacity, primarily impacting the “Upgrader” class in high-value markets like Sydney.

- The “Friction Tax” Burden: In 2026, the total cost of transaction taxes (stamp duty) and fees for a median house exchange in Sydney is projected to consume 93.8% of a median household’s gross annual income. This financial barrier effectively makes moving economically irrational for a majority of households.

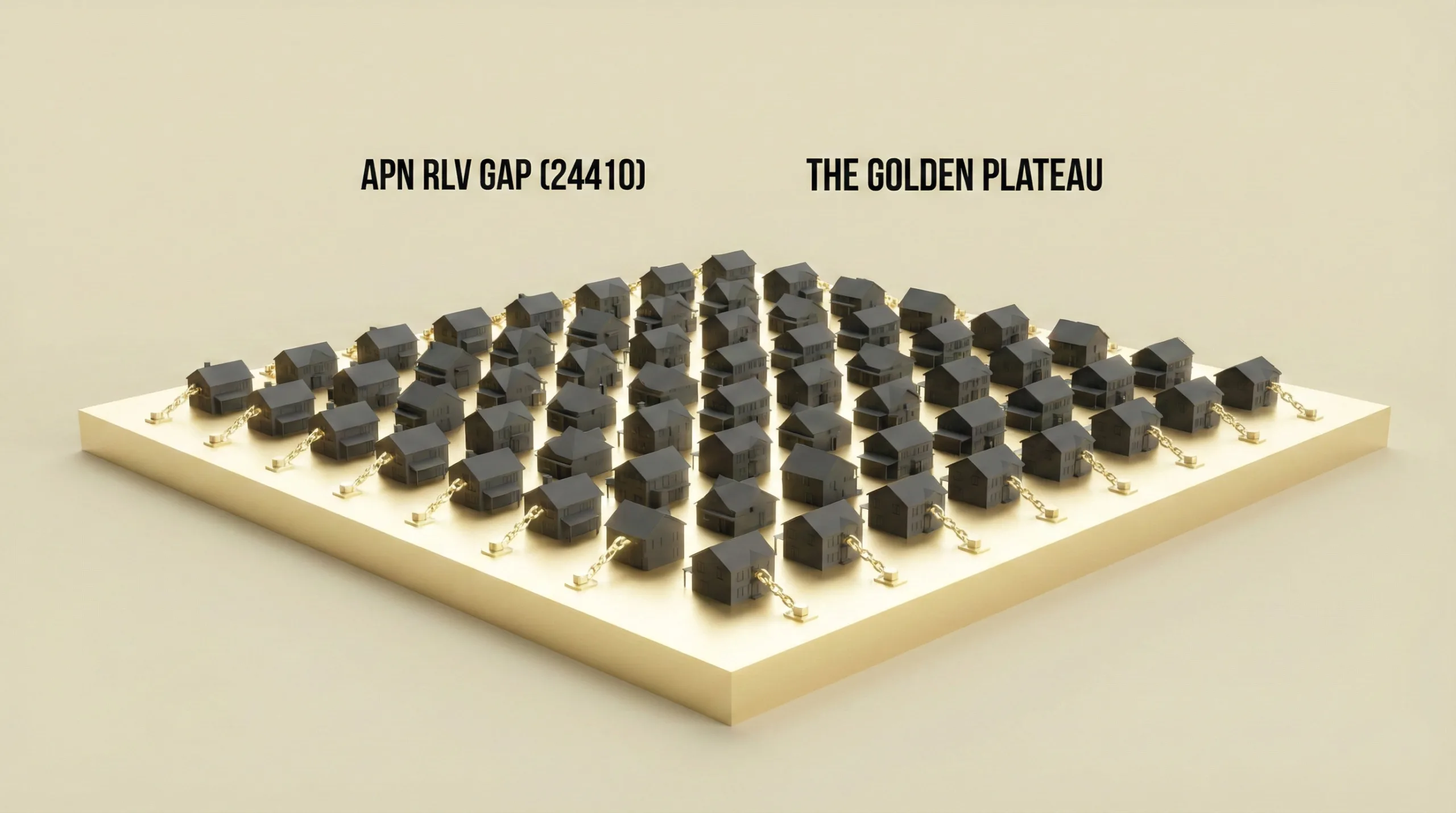

- Systemic Allocative Inefficiency: The combination of these frictions has led to a material misallocation of housing stock, evidenced by over 13 million unoccupied “spare bedrooms” as older households are disincentivised from downsizing, constraining the turnover of family-sized homes and exacerbating supply shortages for younger, growing families.

Critical Analysis & Balanced View

The central paradox of the 2026-2028 housing market is that macroeconomic stability is the primary driver of microeconomic immobility. The RBA’s success in controlling inflation and anchoring the cash rate has structurally constrained households to their existing properties and debt structures. This has decoupled the concept of housing wealth from housing utility; assets have high paper values but low transactional liquidity. Household aspirations are shifting from pursuing an asset accumulation trajectory to maintaining their current housing position.

A critical second-order effect is the “Renovation Constraint.” Unable to afford the friction costs of moving to a more suitable home, households will increasingly divert capital into renovating their existing dwellings. While this addresses immediate needs, it further reduces market liquidity by sinking capital into fixed assets and physically entrenching families in their current locations. This trend will suppress future housing turnover, as the financial and emotional investment in a renovated home makes a future move even less likely.

Furthermore, the market is undergoing a structural bifurcation. The capital reallocation toward lower-priced market segments and outer-suburban corridors is not a sign of a healthy, functioning market but a symptom of the portability structural pressure point. Upgraders, constrained from their target sub-markets, are structurally incentivised to compete in lower price brackets, displacing first-home buyers and inflating prices in segments that should be accessible. The Golden Plateau preserves wealth on paper for established owners but impairs the mechanism for that wealth to facilitate efficient market function.

Strategic Implications for Property Professionals

- For Agents & Buyers’ Agents: The era of high-volume, transactional business is ending. Future viability will depend on pivoting to a high-value advisory model. Specialise in navigating the complexities of the structurally constrained market: downsizer transactions with complex pension implications, sourcing off-market properties for cash-rich buyers, and identifying the cohort of “Upgraders” with sufficient borrowing capacity. Revenue will increasingly come from service fees for strategic advice, not just sales commissions.

- For Developers: The traditional “Upgrader”-focused house-and-land package in the middle-rings faces a structural demand ceiling. The `APN Residual Land Value (RLV) Gap™` (24410) will make many of these projects unviable. The primary opportunity shifts to two key areas: 1) high-quality, low-maintenance downsizer-appropriate stock in established inner- and middle-ring suburbs, and 2) high-density, affordable housing along key transport corridors to capture the displaced first-home buyer and renter markets.

- For Mortgage Brokers & Finance Professionals: The term “structurally constrained mortgage holder” now defines a core client segment. Business models must evolve from simple loan origination to complex debt structuring and refinancing solutions. Expertise in the policies of second-tier and non-bank lenders, particularly those offering streamlined refinancing options, will become a key competitive advantage. Your value proposition is no longer just securing a loan, but providing a pathway to mitigate the mortgage constraint.

- For Property Managers & Asset Managers: Stagnant turnover directly translates to a more stable, and likely more profitable, asset management environment. With households unable to buy, rental demand will remain elevated, supporting strong rental growth. Furthermore, the “renovation boom” creates opportunities for project management services. The focus for investors shifts decisively from capital growth via transactions to maximising yield and capital improvement of held assets.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides validation for the APN Sovereign Policy Composite Index™ (SPCI, 24800) thesis, where the combined actions of the RBA, APRA, and state revenue offices are the primary architects of market structure. It also validates the framework by demonstrating how this structure benefits incumbent, low-leveraged asset holders, while aspiring upgraders and new market entrants face material market-entry barriers.

- Index Calibration: The `APN Risk & Compliance Index™` (24200) is calibrated to reflect the sustained, high-friction environment. The weighting for regulatory stasis (i.e., the maintenance of the 3% buffer) is increased as a primary driver of market immobility. The conceptual ‘Systemic Friction Index’ (SFI) is now formally modelled as a sub-component of this index.

- Data Capture: This analysis triggers a new data capture mandate for the `APN Symbiotic Intelligence Network™` (24310). The network will now track the ratio of renovation-related development applications to property sales listings in key LGAs. It will also seek to quantify the ‘lateral move rejection rate’ from finance partners to directly measure the scale of the structurally constrained mortgage holder cohort.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.