Lifecycle Frictions and Wealth Diversification Drive 55+ Cohort Support for Property Price Moderation

APN ANALYSIS: A-260624-AUS140017

Executive Summary

A structural shift in sentiment has occurred within the Australian residential property market, driven by the evolving preferences of the 55+ demographic. Empirical data from mid-2026 indicates 47 per cent of this cohort, which holds the majority of the nation’s unleveraged housing equity, now actively supports a moderation in property prices. This decoupling of sentiment from historical asset-preservation behaviour is significant because it erodes the political barriers that have traditionally constrained government intervention, expanding the social licence for macroprudential tightening and structural tax reforms.

For property professionals, this sentiment shift represents a durable, structurally embedded change rather than a transient cyclical fluctuation. The analysis indicates that forecasting models assuming older homeowners will universally resist price corrections are now obsolete. The expanded social licence for policy intervention points to an environment of heightened regulatory velocity. This shift also signals the potential for an accelerated release of secondary housing supply as the 55+ cohort increasingly utilises downsizing mechanisms, requiring a strategic pivot in development, financial advice, and asset valuation.

Background & Strategic Context

This analysis validates and calibrates APN’s core macro-thesis regarding the decoupling of demographic sentiment from historical asset-preservation imperatives. The measured preference of the 55+ cohort for property price moderation is analytically significant because it provides an empirical basis for the expansion of the sovereign social licence. By quantifying the erosion of political opposition from this key demographic, the analysis confirms that the risk calculus for property-related policy reform has materially changed, moving from a theoretical possibility to an observable market reality.

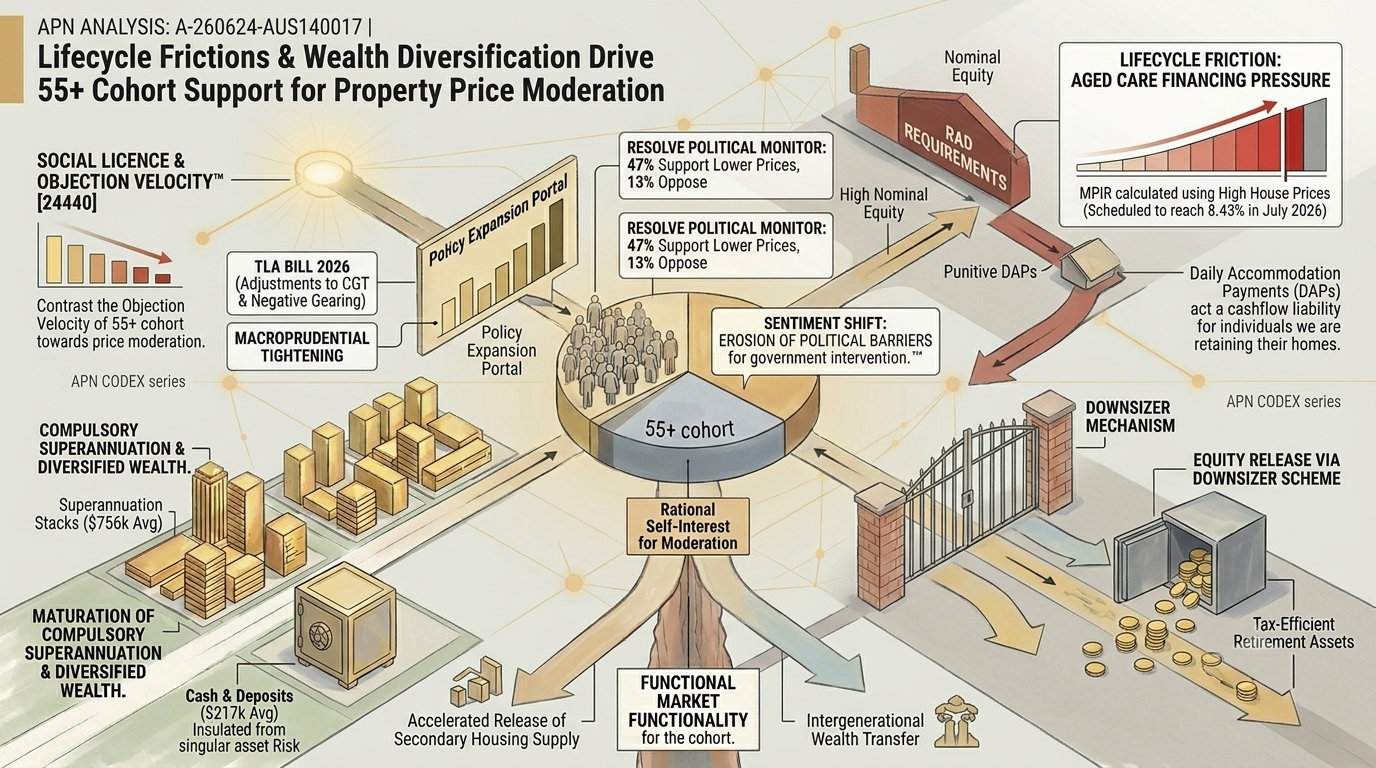

Recalibrating Political Risk (APN Sovereign Policy Composite Index™ (SPCI) (Node 24800)): The minimal opposition to price moderation—just 13 per cent within the 55+ cohort and 11 per cent overall—materially recalibrates the political constraints measured by the SPCI. This demonstrates a structural deterioration in the political capital required to defend nominal asset values, empowering governments to pursue a wider range of policy interventions.

Observing Lifecycle Friction (APN Social Licence & Objection Velocity™ (Node 24440)): The analysis identifies the mechanics of aged care financing (RADs vs DAPs) and the utility of the downsizer superannuation scheme as primary drivers of the sentiment shift. These lifecycle frictions create a rational, self-interested incentive for the 55+ cohort to prefer a moderated market, lowering the ‘objection velocity’ to policies that facilitate this outcome.

Confirming Wealth Diversification (Demographic Analysis): The maturation of Australia’s compulsory superannuation system is a critical contextual factor. Data confirming that the 55+ cohort possesses substantial, diversified wealth outside the primary residence explains their reduced sensitivity to nominal property price fluctuations and their capacity to prioritise liquidity and intergenerational outcomes over pure equity preservation.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Resolve Political Monitor (mid-2026), Australian Bureau of Statistics (ABS) data, and Australian Taxation Office (ATO) statistics. The key facts are:

- Sentiment Shift Among 55+ Cohort: According to mid-2026 Resolve Political Monitor data, 47 per cent of respondents aged 55 and over actively support lower residential property prices, compared to only 13 per cent who oppose them.

- Broad-Based Support for Price Moderation: Across the general electorate, 54 per cent of respondents support lower prices, while only 11 per cent are opposed. This support extends to 55 per cent of encumbered mortgage holders and 62 per cent of property investors.

- Material Wealth Diversification: Analysis of ABS data shows the 55-64 age cohort holds an average of $1.529 million in property, but this is supplemented by an average of $756,000 in superannuation reserves and $217,000 in cash and deposits, insulating them from singular asset class risk.

- Aged Care Financing Pressure: The Maximum Permissible Interest Rate (MPIR), used to calculate Daily Accommodation Payments (DAPs) for aged care, was scheduled to reach 8.43% in July 2026. This transforms high nominal property values into a material cashflow liability for individuals retaining their homes upon entering care.

- Downsizer Mechanism Utilisation: ATO data confirms that the downsizer superannuation contribution scheme is a structurally significant asset recycling pathway, with tens of billions of dollars in contributions made since its inception, allowing for the tax-efficient conversion of housing equity into liquid retirement assets.

Critical Analysis & Balanced View

The analysis reveals a critical paradox: for the 55+ cohort, continued nominal house price inflation has transformed from a wealth generator into a material liquidity risk. Historically, a rising property market was synonymous with increased wealth. However, the interaction of inflated property values with the mechanics of aged care financing has inverted this logic. High house prices directly inflate the Refundable Accommodation Deposits (RADs) required for aged care. For individuals who wish to retain the family home, this results in punitive Daily Accommodation Payments (DAPs) calculated using the high Maximum Permissible Interest Rate (MPIR). In this environment, supporting price moderation is a rational act of liquidity preservation and estate protection, prioritising accessible capital over illiquid, nominal equity.

Furthermore, this durable shift in sentiment acts as a leading indicator of future regulatory velocity. The minimal political backlash to the proposed Treasury Laws Amendment (Tax Reform No. 1) Bill 2026—which includes adjustments to CGT and negative gearing—provides the first concrete evidence of this new paradigm. The social licence granted by the 55+ cohort is not passive tolerance but an active preference for a more functional market that enables intergenerational wealth transfer and ensures their own long-term macroeconomic security. This suggests that forecasting models must now assign a higher probability and lower political friction coefficient to significant, state-led structural market reforms.

Strategic Implications for Property Professionals

- For Developers & Planners: Anticipate increased secondary supply in established, middle-ring suburbs as downsizing accelerates. The strategic focus should shift towards delivering high-amenity, low-maintenance, medium-density housing in these locations to capture the downsizer market, which may prove more resilient than reliance on greenfield development.

- For Financial Advisors & Wealth Managers: The advisory conversation for the 55+ cohort must evolve from maximising nominal asset growth to optimising liquidity and managing lifecycle transition costs. Modelling the financial impact of aged care entry (RAD vs DAP at current MPIRs) and the optimal timing for utilising the downsizer contribution scheme are now critical, non-negotiable services.

- For Valuers & Asset Managers: The historical assumption of a political ‘put’ option underpinning residential property values is materially weakening. Valuation models must now incorporate a higher risk weighting for policy-driven market adjustments, particularly those related to federal taxation (CGT, negative gearing) and macroprudential controls.

- For Real Estate Agents: The value proposition for older vendors is changing. Listing presentations should pivot from a singular focus on achieving a peak sale price to a more holistic discussion around achieving the vendor’s strategic financial goals, such as tax-effective capital release via the downsizer scheme and securing a more suitable, lower-maintenance property.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the APN Sovereign Policy Composite Index™ (SPCI) (Node 24800) by empirically demonstrating the erosion of a key historical constraint—political opposition from older homeowners—which expands the sovereign social licence for market intervention.

- Index Calibration: The APN Social Licence & Objection Velocity™ (Node 24440) is calibrated to reflect a lower baseline of political resistance from the 55+ demographic regarding policies aimed at property price moderation.

- Data Capture: This triggers a new data capture mandate for the APN Sovereign Policy Composite Index™ (SPCI) (Node 24800) to track the legislative progress and market impact of tax reforms (e.g., CGT, negative gearing) that were previously considered politically unviable.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24800) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.