Tax-Driven Capital Reallocation to Face Material Supply Constraints and Primary Market Inflationary Risk

APN ANALYSIS: A-260624-AUS140013

Executive Summary

The Australian Government is implementing significant tax reforms effective 1 July 2027, restricting negative gearing to new builds to redirect investment from the secondary market into new housing supply. This analysis finds that while the policy is supported by a unique shift in investor sentiment, the construction sector lacks the physical and financial elasticity to absorb the capital influx. This creates a material risk of new-build price inflation and secondary market illiquidity rather than a proportional increase in physical supply.

For property professionals, this indicates a strategic pivot is required. Developers face a market where demand-side incentives will likely be capitalised into land and construction costs, not just profit margins. Investors must re-evaluate internal rate of return (IRR) calculations for both primary and secondary markets, accounting for an upfront premium on new stock and reduced liquidity for established assets. Valuers will need to navigate a bifurcated market with a growing ‘replacement cost gap’ and the emergence of a ‘turnover trap’ for grandfathered properties.

Background & Strategic Context

This analysis validates and calibrates APN’s core macro-thesis that sovereign policy interventions, while capable of redirecting capital flows, are ultimately governed by the physical and economic constraints of the underlying market. The proposed tax reforms provide a critical test case, demonstrating that legislative intent cannot unilaterally create supply where the fundamental feasibility equation, as measured by the APN Future Development Pipeline Index™, is negative.

A Rational Sentiment Shift (APN Professional Sentiment Index™ (24300)): The political viability of the reforms is anchored in the finding that 62 per cent of investors support lower house prices. APN analysis identifies this not as paradoxical, but as a rational response to a ‘serviceability trap’ where elevated asset prices prevent portfolio expansion. This sentiment provides the sovereign with the social licence to implement reforms that would have previously been politically untenable.

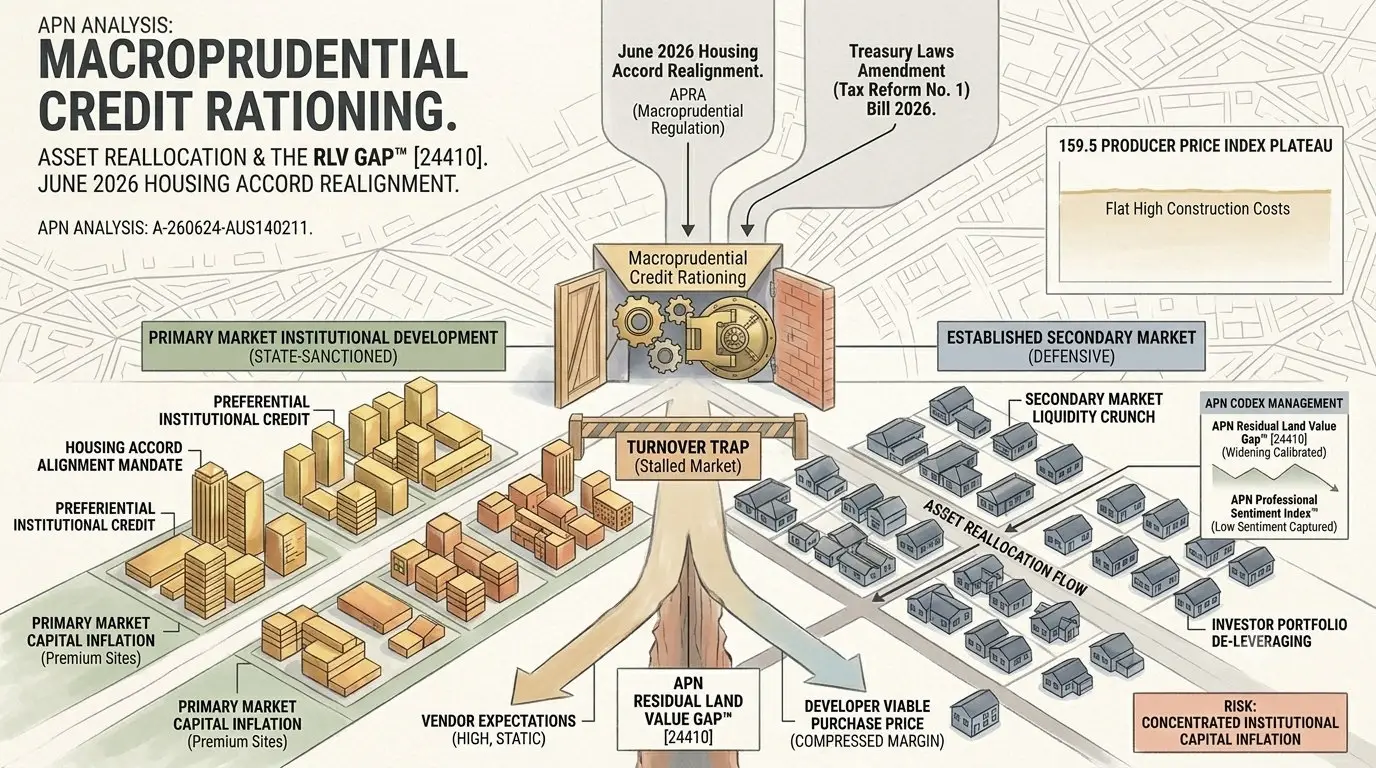

The Feasibility Barrier (APN Residual Land Value (RLV) Gap™ (Node 24410)): While the tax changes can redirect capital, they do not alter the fundamental economics of construction. The RLV Gap, which measures the difference between development costs and end-market value, remains materially negative for many projects due to elevated construction, finance, and holding costs. This gap acts as a structural barrier, preventing the construction sector from scaling up to meet the redirected demand.

The New-Build Premium (APN Replacement Cost Gap™ (Node 24450)): This index measures the divergence between the cost of a new dwelling and the value of an equivalent existing one. Sustained cost inflation has created a significant gap, establishing a high price floor for new builds. This analysis indicates that the value of the negative gearing concession will likely be absorbed by this premium, transferring the financial benefit to developers and landowners rather than improving affordability or yield for the investor.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Treasury Laws Amendment (Tax Reform No. 1) Bill 2026 and associated market data from the Australian Bureau of Statistics (ABS) and the Australian Prudential Regulation Authority (APRA). The key facts are:

- Legislative Mechanism: From 1 July 2027, negative gearing will be restricted to newly constructed dwellings. The 50 per cent Capital Gains Tax (CGT) discount will be replaced with cost base indexation and a 30 per cent minimum tax rate on capital gains, with grandfathering provisions for assets held before 12 May 2026.

- Investor Sentiment Shift: APN research identified that 62 per cent of property investors support lower house prices, a rational response to being locked out of further acquisitions by high prices and stringent serviceability criteria.

- Elevated Construction Cost Base: ABS Producer Price Index data shows the cost of inputs to house construction remains at a post-peak plateau, with the index at 159.5 as of December 2025, indicating a sustained high-cost environment for new builds.

- Contracting Supply Pipeline: ABS Building Approvals data shows high volatility and a contracting trend, with total dwelling approvals falling 7.2 per cent in January 2026. This indicates the pipeline is not expanding in preparation for the capital shift.

Critical Analysis & Balanced View

The convergence of these factors produces two critical second-order implications not immediately apparent from the policy’s headline objectives. Firstly, the social licence underpinning the reform may be more fragile than it appears. The government’s mandate is predicated on investors seeking to escape a serviceability trap. However, if the policy results in new-build price inflation and secondary market illiquidity, it will fail to restore the transactional capacity investors desire. This could lead to a rapid erosion of that social licence post-implementation, as the policy is perceived to have benefited developers at the expense of both investors and prospective first-home buyers.

Secondly, the grandfathering provisions are likely to create a ‘turnover trap’ in the secondary market. An owner selling an established investment property post-July 2027 would forfeit the grandfathered tax status and face the new CGT regime. This creates a powerful disincentive to transact, which will structurally constrain listings of established properties. This reduction in market liquidity will create a defensive price floor for established housing, counteracting the policy’s intended effect on affordability and trapping capital in existing assets, contrary to the primary objective of the legislation.

Strategic Implications for Property Professionals

- For Developers: The redirected capital will likely manifest as increased buyer willingness to meet higher asking prices, but this will be offset by escalating land and construction costs. Success will depend on securing a pipeline of viable projects before the full inflationary impact is priced in by the supply chain.

- For Investors: The choice is between a premium-priced new asset with tax concessions, or a secondary market asset with lower liquidity and no concessions for new purchasers. Portfolio strategy must now account for a bifurcated market and the risk that the tax benefit on new builds is fully capitalised into the purchase price.

- For Financiers: A recalibration of lending risk for both development and investment loans is required. Development finance will face heightened scrutiny on cost escalation and delivery timelines, while investment lending for secondary market assets will need to factor in reduced turnover and potential valuation stagnation.

- For Valuers: Valuations must increasingly differentiate between new and established stock, explicitly accounting for the APN Replacement Cost Gap™. The value of grandfathered tax status for existing properties will become a complex, non-market attribute to assess, particularly in deceased estates and family transfers.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the APN Residual Land Value (RLV) Gap™ (Node 24410) as the primary mechanism constraining the construction sector’s response to demand-side stimulus.

- Index Calibration: The APN Sovereign Policy Composite Index™ (SPCI) (24800) is calibrated to reflect the high probability of contradictory outcomes, where a policy designed to increase supply instead generates primary market inflation and secondary market illiquidity.

- Data Capture: This triggers a new data capture mandate for the APN Replacement Cost Gap™ (Node 24450) to track the premium of new builds over equivalent established dwellings on a national and capital city basis, isolating the component attributable to the capitalised tax concession.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24800) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.