Structural Decoupling in Regional Australia: An Analysis of Metropolitan Capital Reallocation and its Impact on Regional Housing Markets

APN ANALYSIS: A-260225-AUS137666

Executive Summary

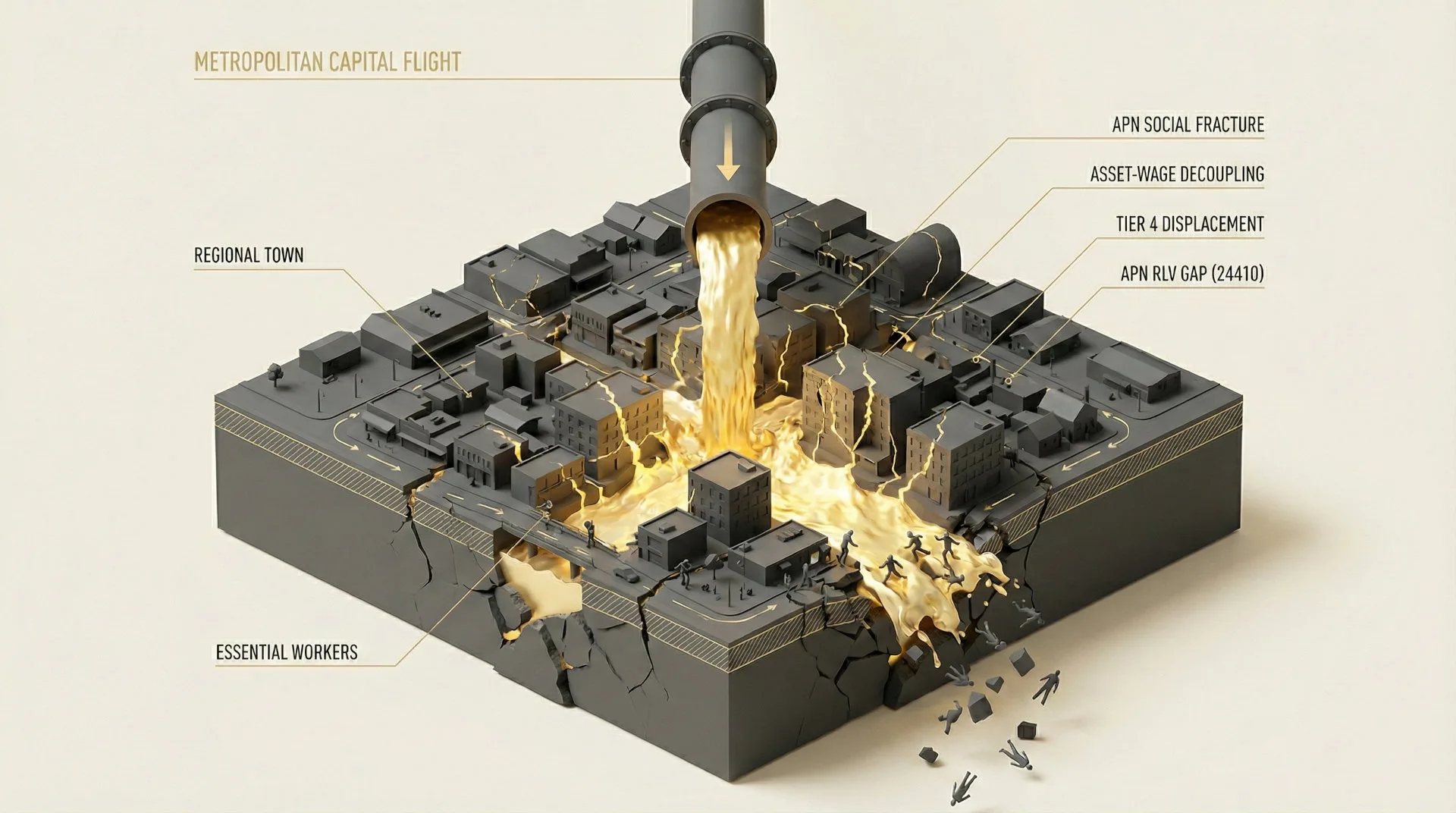

A material structural decoupling is underway in the Australian property market. Material capital reallocation from high-valuation metropolitan centres like Sydney and Perth is being funnelled into regional hubs, creating a pure asset-inflation event that is mathematically untethered from local economic productivity. Regional dwelling values are materially outpacing capital city values, with quarterly growth in high-growth centres like Wagga Wagga (8.1%) nearly 40 times that of Sydney (0.2%). This matters because the influx of metropolitan ‘Equity Refugees’ is absorbing finite housing stock, creating elevated asset-wage decoupling and triggering the secondary displacement of the essential Tier 4 service class, the host population required for regional economies to function.

For property professionals, this analysis serves as an important advisory against pursuing nominal capital growth. The headline figures mask a sustained deterioration in the underlying utility and social resilience of these regional centres. The key forward-looking metric is no longer price velocity, but the operational viability of a location. Assessing the risk of a ‘structural service delivery failure’, in which a town can no longer staff its essential services, is now a primary consideration for accurate valuation, risk management, and the identification of sustainable development opportunities. The highest yields today may belong to the most structurally vulnerable assets tomorrow.

Background & Strategic Context

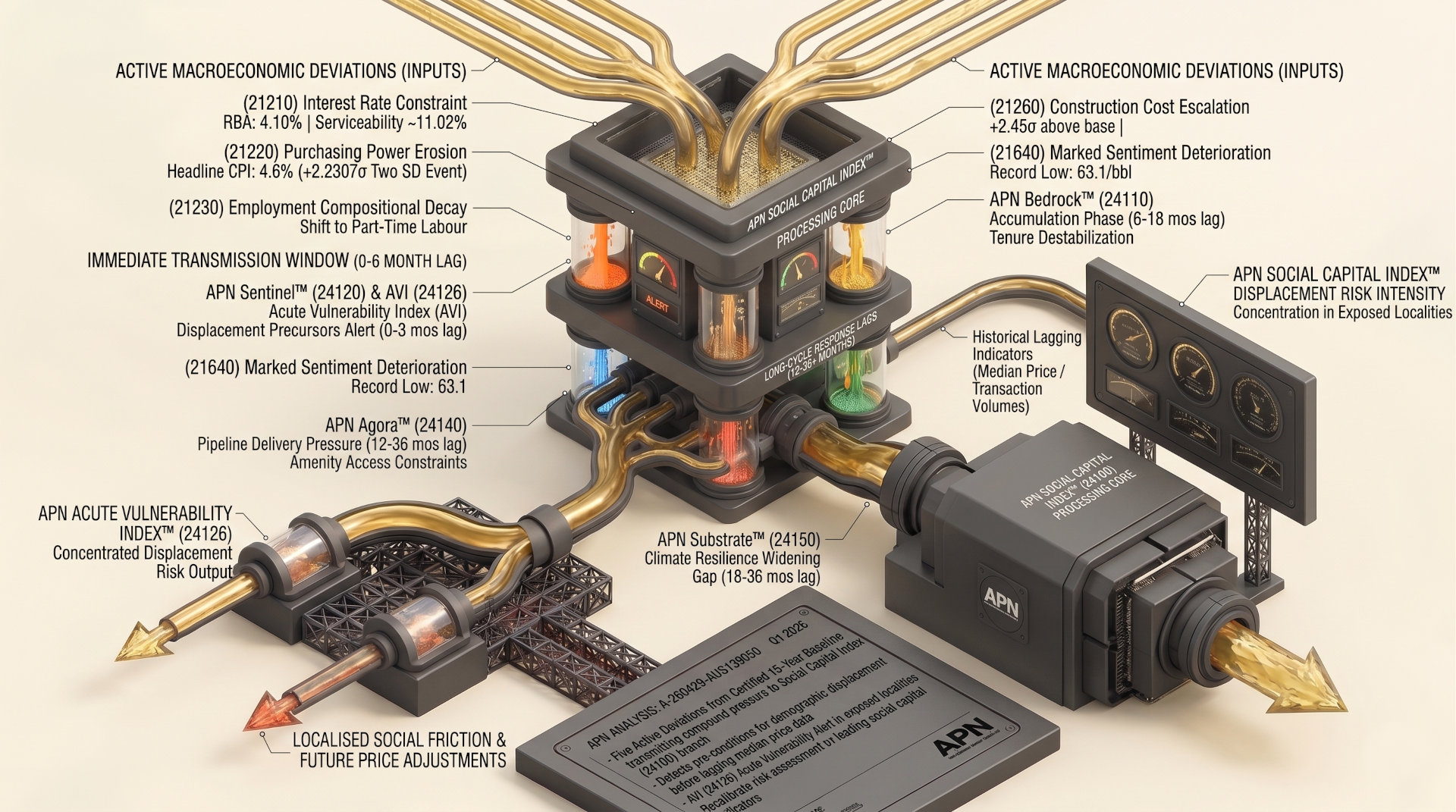

This event validates and calibrates APN’s core macro-theses, demonstrating a clear illustration of asset inflation creating a systemic social and economic structural adjustment. The data provides empirical evidence that state-level policy failures and market dynamics combine to structurally degrade productive regions in favour of static asset holders.

Systemic Capital Reallocation: The dynamic represents a confluence of factors for this framework. Capital is being systematically reallocated from the productive, wage-earning Tier 4 ‘Host Class’ in regional Australia to metropolitan ‘Equity Refugees’ and asset-holders. The 25-percentage-point gap between regional rent inflation (42%) and wage growth (17.5%) over the past five years is a direct, quantifiable measure of this capital reallocation.

Structurally Advantaged Social Displacement (Net State Position™): The analysis confirms the structural adjustment of the ‘Glass House’. We are witnessing the physical displacement of the Tier 4 ‘Host’ class by a cohort with substantial equity leveraging metropolitan asset holdings. This is not economic migration but a structurally advantaged displacement, where the host population is pushed into precarious housing or forced to exit their own communities, creating a negative net state position for the region’s long-term functionality.

Productivity-Value Inversion (Asset-Wage Decoupling Index™): The elevated divergence between regional asset values and local economic output provides a clear calibration for this index. The case of Wagga Wagga, with an 8.1% quarterly price increase against a -1.0% contraction in Gross Regional Product (GRP), moves beyond decoupling into a state of direct contradiction, signalling a pure, externally-fuelled speculative valuation premium.

The Structural Affordability Floor (The Supply Illusion): The structural pressure point is amplified by a constrained supply response. With 88% of regional builders reporting material delays and a national labour shortage, there is no market mechanism to absorb the demand shock. This creates a sustained ‘Supply Floor’ under prices and rents, sustaining the affordability pressure point regardless of local economic performance.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Cotality February 2026 Regional Market Update, supplemented by ABS migration data and regional economic output reports. The key facts are:

- Regional Outperformance Solidified: In the three months to January 2026, combined regional dwelling values rose 3.2%, significantly outpacing the 2.1% growth across combined capital cities.

- Elevated Price Velocity in Hubs: Specific regional centres are experiencing rapid price escalation. Wagga Wagga (NSW) recorded an 8.1% quarterly price increase, while in WA, Albany (7.7%) and Kalgoorlie-Boulder (7.6%) showed similar elevated velocity.

- Productivity Contradiction: The price acceleration is occurring in a vacuum of local economic growth. Wagga Wagga’s Gross Regional Product (GRP) contracted by -1.0% in the year to June 2024, indicating the asset inflation is not supported by underlying productivity.

- Systemic Rental Stress: Over the last five years, regional rents have experienced accelerated growth of 41.9%, while national wages have grown by only 17.5%. This has pushed the ‘24126 Desperation Index’ (rent as a percentage of net income) to ~68% for essential single-income workers in hubs like Wagga Wagga, far exceeding the 45% ‘Structural Adjustment Point’.

- Sustained Displacement Velocity: The net migration loss from capital cities to regions remains structurally elevated, with ‘acute affordability constraint’ replacing ‘lifestyle’ as the primary driver for 37% of metropolitan residents considering a move.

Critical Analysis & Balanced View

The prevailing narrative of a ‘regional boom’ is a misinterpretation with material consequences. This is not a period of accelerated growth; it is the structural erosion of regional Australia. The core paradox is that the very mechanisms driving short-term price growth—capital reallocation and infrastructure projects—are simultaneously degrading the long-term viability of these communities. Large-scale projects, while appearing positive, introduce transient, highly-paid workforces that compete for the same limited housing stock, creating a ‘Corporate Demand’ floor under rents and further displacing the permanent Tier 4 service class.

This creates a self-reinforcing condition of economic constraint. The displacement of the host class leads to workforce attrition in sectors such as retail, hospitality, and healthcare. This reduces the ‘Liveability’ and ‘Utility’ of the hub, diminishing the very amenity that attracted the ‘Equity Refugees’ in the first place. The current market is therefore a high-velocity speculative valuation premium, sustained by capital responding to acute affordability constraints, but the underlying asset is becoming functionally degraded. The risk is not a standard market correction, but a complete ‘Utility Contraction’ when the social fabric of these towns finally degrades, rendering the high-priced assets illiquid and undesirable.

Strategic Implications for Property Professionals

- For Developers: The opportunity is not in speculative residential development, which faces a declining local buyer pool. The strategic opportunity is in addressing the structural deficit of key worker housing. Build-to-rent models with allocations for the Tier 4 class, potentially in partnership with local councils or large employers, represent a de-risked, long-term revenue stream that also enhances a project’s social licence to operate.

- For Agents & Buyers’ Agents: Client advisory must evolve beyond capital growth charts. Professionals must now act as risk managers, guiding clients with new metrics. Quantify the ‘structural service delivery failure’ risk by assessing local vacancy rates, service class staff shortages, and the ratio of median rent to award wages. A high APN Bedrock™ (24110) score is now a more valuable indicator of long-term stability than short-term price increases.

- For Investors: The current high rental yields in regional hubs are a misleading short-term indicator. They are predicated on a level of rental stress (~68% of income) that is structurally unsustainable. The lead indicator for future capital loss is the attrition of the local service class. Investors must pivot from assessing asset yield to assessing community resilience, as a town without workers is a town without a functioning economy or tenant pool.

- For Valuers & Lenders: Current valuations based on comparable sales are reflecting elevated market activity, not intrinsic value. A ‘structural service delivery failure’ risk premium must be factored into valuations in markets exhibiting elevated asset-wage decoupling. Lenders should scrutinise the GRP-to-price-growth ratio as a measure of speculative valuation premium risk and consider the long-term serviceability of loans in regions facing a potential contraction in essential services.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides validation for the APN Asset-Wage Decoupling Index™ (24610), with the 25-point gap between rent and wage growth serving as a new benchmark for ‘Elevated’ decoupling. It also validates the core mechanism of capital reallocation from wage-earning cohorts to asset holders and the social stratification outcomes tracked by the Net State Position™ (24600) framework.

- Index Calibration: The proprietary ‘24126 Desperation Index’ analysis, which measures housing stress on the service class, is now formally integrated as a critical input for the APN Bedrock™ (24110) social cohesion score. A reading above 45% (rent-to-net income) is set as a trigger for a ‘Structural Service Delivery Failure’ alert, materially downgrading a location’s resilience rating.

- Data Capture: This analysis triggers a new data capture mandate to continuously monitor the GRP-to-dwelling-value ratio in Australia’s top 30 regional SA4s. This ‘Productivity Contradiction Ratio’ will serve as a primary input for identifying markets driven by ‘Pure Asset Inflation’ rather than organic economic growth.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24600) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.