A Clash of Symptoms, A Union of Cause: Deconstruction of “FULL DEBATE: What’s REALLY Causing Australia’s Housing Crisis?”

Source: Punters Politics Podcast

Host: Konrad Benjamin

Participants: Leith van Onselen (Macrobusiness), Matt Grudnoff (The Australia Institute)

Executive Summary

The debate between Leith van Onselen and Matt Grudnoff is a clash over proximal causality. It is not a debate about if the housing market is “cooked” (1:16), but which government-controlled lever is the primary culprit.

- Leith van Onselen’s thesis is that the rental crisis (which he views as the “bigger tragedy” (2:44)) is overwhelmingly driven by a state-led demand shock via “excessive immigration” (2:49), far exceeding the physical capacity to supply new dwellings.

- Matt Grudnoff’s thesis is that the house price and affordability crisis is overwhelmingly driven by a state-led speculative incentive via “the capital gains tax discount” (5:58) and negative gearing, which defines the market mechanics under The Wealth Funnel.

Crucially, while the debate is framed as a “clash,” the participants are on a “unity ticket” (37:03) on the most significant structural drivers: the distortionary impact of tax concessions, the gross misallocation of capital by banks, the failure of successive governments, and the urgent need for state-built public housing. The primary disagreement is one of sequencing and emphasis.

Core Theses & Statistical Battlegrounds

The “clash” element of the debate rests on conflicting statistics and interpretations of the supply/demand balance.

1. Leith van Onselen (Focus: The Rental Crisis)

- Core Argument: Leith bifurcates the crisis. He concedes tax concessions inflate prices (2:38) but argues they “don’t necessarily do much to the rental market” (2:44). He posits that the rental crisis is a simple, physical supply-and-demand problem, with immigration being the “biggest driver” of demand (3:52).

- “Silver Bullet”: A “much smaller and better targeted immigration system” (52:39). He ranks this above tax reform because it directly and immediately addresses the rental crisis (53:16).

- Key Data Points:

- Blame Allocation: Immigration is 75% to blame for the rental market crisis and 25% for house prices (5:17-5:34).

- Vacancy Rate: Cites the all-time record-low rental vacancy rate (1.4%) as indisputable proof of a physical shortage (13:21).

- Population Stat: Counters Matt, stating population has grown 45% since 2000, not 33% (11:02).

- Rent Stats: Cites Cotality and HILDA data showing rents are at a record high as a share of income and have surged 40% in 5 years (12:15-12:42).

- NHSAC Report: Cites the government’s own report forecasting a 79,000-home shortage over 5 years, which would become a 40,000-home surplus if population growth were 15% lower (19:26).

2. Matt Grudnoff (Focus: The Price & Affordability Crisis)

- Core Argument: The crisis is one of speculation, not a physical shortage. The 1999/2000 CGT discount is the “villain,” creating a speculative asset class (6:04). This allows “rich cashed-up investors” (7:43) to outbid first-home buyers (FHBs), driving prices far beyond fundamentals and reducing homeownership.

- “Silver Bullet”: Abolish the Capital Gains Tax discount for residential property (53:53). This not only removes the distortion but also raises billions that can be funnelled into public housing (54:11).

- Key Data Points:

- Blame Allocation: Tax-driven speculation is 80-90% to blame for house prices (8:35). Immigration is “0 to 1%”… “a tiny factor, a rounding error” (10:33).

- The Divergence: Cites the 25-year divergence between house prices (up fivefold) and rents (up 115%, just above CPI at 103%) as proof it is not a population-driven shortage (8:49-9:55). If it were, both would rise together.

- Dwelling Stat: Claims that over 25 years, population grew 33% while dwellings grew 39% (7:03). He repeats this for the last 10 years (16% pop vs 19% dwellings) (20:47), arguing “we are building houses faster than the population is growing.”

- Recent Rent Spike: Concedes the recent 3-year rent spike (15:14) but attributes it to a post-COVID “bounce back” and general inflation, not a long-term structural driver (15:37-16:07).

Critical Points of Agreement (The “Unity Ticket”)

The areas of agreement are far more structural and strategically significant than the disagreements. Both participants effectively validate APN’s core frameworks.

- The Wealth Funnel (Incumbent Benefit):

- Both are in “100%” agreement (36:57) that tax concessions (CGT/NG) are the central engine of the price crisis.

- Matt describes The Funnel’s mechanism: “investors are buying up the stock… at the expense of owner occupiers” (35:49), forcing FHBs to “continue renting” (35:43).

- Leith provides a perfect case study: Victoria “whacked property investors” with land taxes, causing Melbourne prices to flatline and become the most affordable capital (37:14-37:50).

- Project Overlord (State-Led Intervention):

- The entire debate is an argument about which Overlord lever (immigration vs. taxation) is the root cause.

- Both identify the 5% Deposit Scheme as a “terrible policy” (42:50) and “pouring petrol on a bonfire” (43:35). They correctly identify it as a state subsidy for demand, not supply.

- Matt explicitly calls out the political misdirection of Project Overlord: Federal Minister Clare O’Neil knows the federal lever is tax, but she “busily” blames “supply” because it’s a state problem, not hers (57:59-58:18).

- Gross Misallocation of Capital (Systemic Distortion):

- Leith (39:19) and Matt (40:40) agree the system has created a “gross misallocation of capital” away from productive businesses and into sterile housing speculation.

- They identify the enablers:

- Banks: Profit ($200k per mortgage) from “very, very safe” mortgage lending vs. risky business lending (Matt, 40:53).

- Regulation: Basel Capital Rules explicitly incentivise this by requiring less capital to be held against mortgages (Leith, 41:40).

- The Ultimate Solution (Public Housing):

- When asked about a public housing developer, both immediately respond: “Good. Do it.” (54:36).

- Matt cites Singapore as the global model: a land-constrained nation with affordable housing because “the government builds housing” at cost (54:47-55:19).

- They agree this solves multiple problems, including creating a training pipeline for tradies, which was destroyed by privatisation (55:25-56:52).

APN Intelligence Analysis & Strategic Implications

This debate reveals the fractured public narrative and the deep-seated structural flaws underpinning the market.

- Framework Validation: The debate is a perfect public-facing articulation of APN’s core frameworks. Project Overlord (state intervention via tax, immigration, subsidy) created The Wealth Funnel (speculative-driven incumbent benefit), which was enabled by Project Cerberus Oz (risk-transfer regulations like Basel/5% deposit) and has now resulted in a critical failure of Project Conduit (supply).

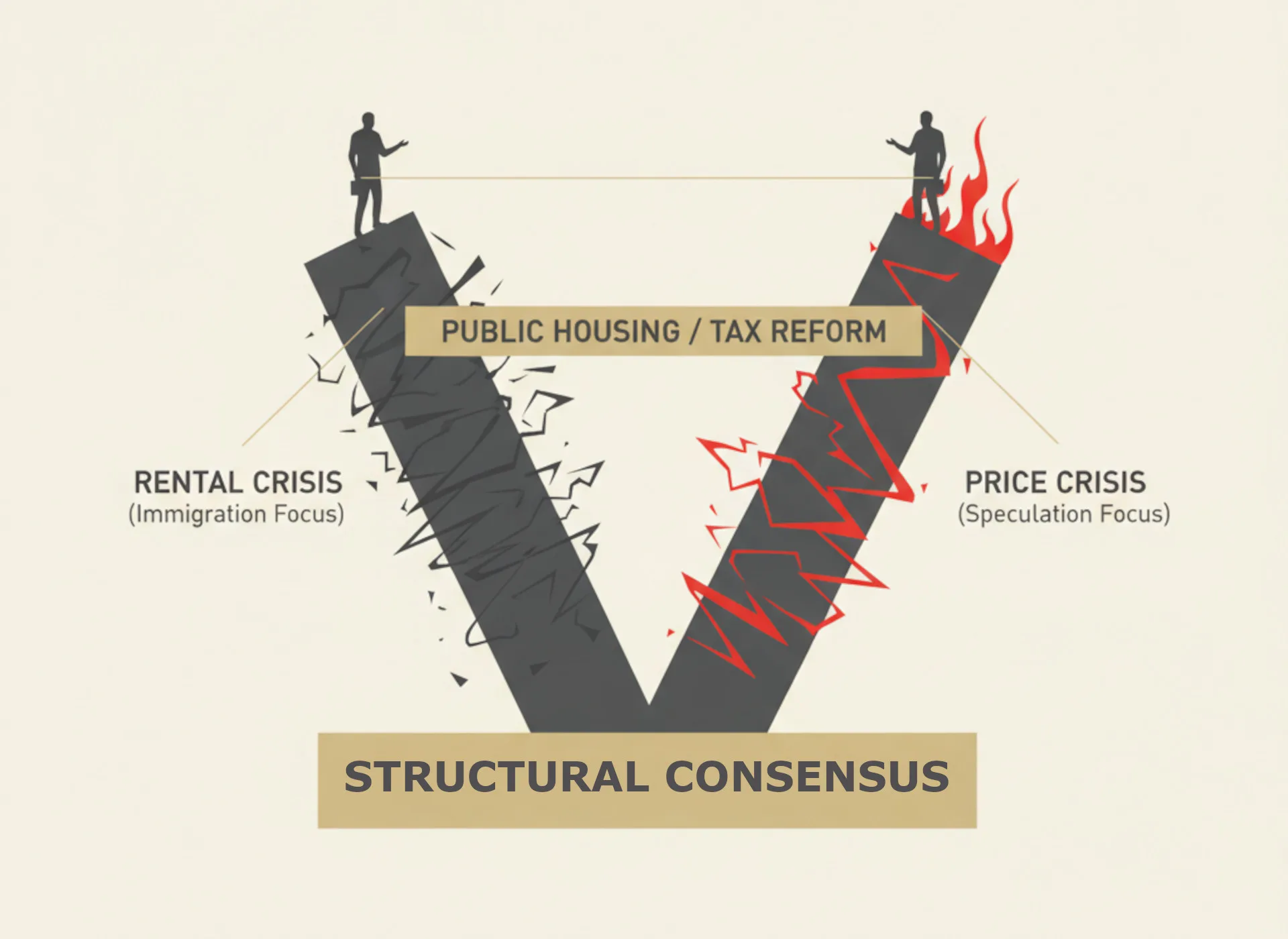

- The “Rental Crisis” vs. “Price Crisis” Distinction is Critical:

- Leith’s 1.4% vacancy rate (13:21) is the single most important current data point. It is the “canary in the coal mine” and validates his thesis of an acute physical shortage in the rental market, driven by a demand/supply mismatch right now.

- Matt’s 25-year price/rent divergence (9:09) is the single most important structural data point. It validates his thesis that price is decoupled from physical reality and is instead a financial phenomenon driven by speculation.

- Conclusion: They are both correct. We have two distinct, though related, crises.

- The Supply Debate Misses the Point (The RLV Gap):

- The statistical argument over “dwellings vs. population” (7:03, 20:47) is a red herring. It misses the APN concept of the Residual Land Value (RLV) Gap.

- Leith gets close by noting we built “shoe box apartments” (27:22) – this is because that is what was viable for developers to build.

- Matt gets close by noting developers “don’t build affordable housing… because they don’t have any money” (45:14).

- The real supply issue, unstated, is that private developers cannot profitably deliver housing at a price point that low/middle-income earners can afford. This viability gap is the true bottleneck, which is why both participants land on public housing as the only non-market solution.

- Strategic Implications for APN:

- For Investors: The market is now balanced on two government levers. Monitor migration policy (for rental yields and short-term demand) and tax policy (for long-term capital values). The “unity ticket” on tax reform suggests this risk is increasing, though Leith’s cynicism (58:29) about political will is well-founded.

- For Developers: The “missing middle” and affordable housing segments are non-viable for the private market. The only solution presented is state-led development (the Singapore model). This represents a massive threat to the current development model but a colossal opportunity for firms that can partner with or build for a future “Housing Australia” public developer.

- Political Risk: Matt’s final point (1:00:01) is the key. The “political calculus” is shifting because the growing “renter class” is “really pissed off.” This demographic shift is the single biggest threat to The Wealth Funnel. The party that successfully captures this vote will be the one to enact genuine structural change.

This analysis is based on a video from the Punters Politics Podcast YouTube Channel, featuring a well-facilitated debate by host Konrad Benjamin, titled “FULL DEBATE: What’s REALLY Causing Australia’s Housing Crisis? Econmists Clash“. You can find the original content here: https://www.youtube.com/watch?v=1GhgBTsgBj4

Disclaimer

The analysis and information contained in this analysis are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on internal APN intelligence, data, and information believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events. Property values and market conditions can go down as well as up.

Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.