Lifestyle-Fiscal Decoupling: The Structural Impact of Tax Policy on Non-Primary Residential Assets

APN ANALYSIS: A-260114-AUS134271

Executive Summary

A convergence of federal and state tax policy has structurally undermined the financial viability of the leveraged Australian holiday home, creating a “Lifestyle-Fiscal Decoupling” event. The Australian Taxation Office’s reclassification of these assets as non-deductible “Leisure Facilities” (TR 2025/D1), combined with Victoria’s expansion of its Vacant Residential Land Tax (VRLT), has created a structurally significant increase in holding costs exceeding $100,000 per annum for a typical asset. The resulting 18.4% material increase in listings is not a material valuation correction driven by diminishing lifestyle appeal, but a “forced liquidity” event as the non-institutional investor cohort is structurally displaced by regulatory changes.

For property professionals, this “Lifestyle-Fiscal Decoupling” represents a generational transfer of assets. The widespread divestment of leveraged, tax-sensitive investors creates a significant acquisition opportunity for the equity-rich owner-occupier class and developers focused on asset repositioning. Understanding the bifurcation in regional resilience, where markets like the Mornington Peninsula are absorbing the structural adjustment via a “Permanent Pivot” to residential living, while others like Byron Bay face structural vulnerability, is now of elevated importance to capital allocation and client advisory for the FY25/26 cycle.

Background & Strategic Context

This event validates and calibrates the APN Sovereign Policy Composite Index™ (SPCI, 24800), demonstrating how state-level intervention acts as the primary force reshaping market boundaries and asset class viability. The convergence of federal tax reinterpretation and state-based levies has created convergent regulatory actions, accelerating the wealth transfer dynamics between distinct capital cohorts and stress-testing the resilience of local lifestyle economies.

The Primacy of State-Level Policy (SPCI, 24800): The coordinated, albeit unintentional, convergent regulatory actions between the ATO (federal) and the Victorian SRO (state) are a clear illustration of state actors defining market outcomes. The reclassification of holiday homes from tax-advantaged investments to post-tax consumption items is a direct intervention that has structurally invalidated an entire ownership model, demonstrating that regulatory change is the primary driver in Australian property.

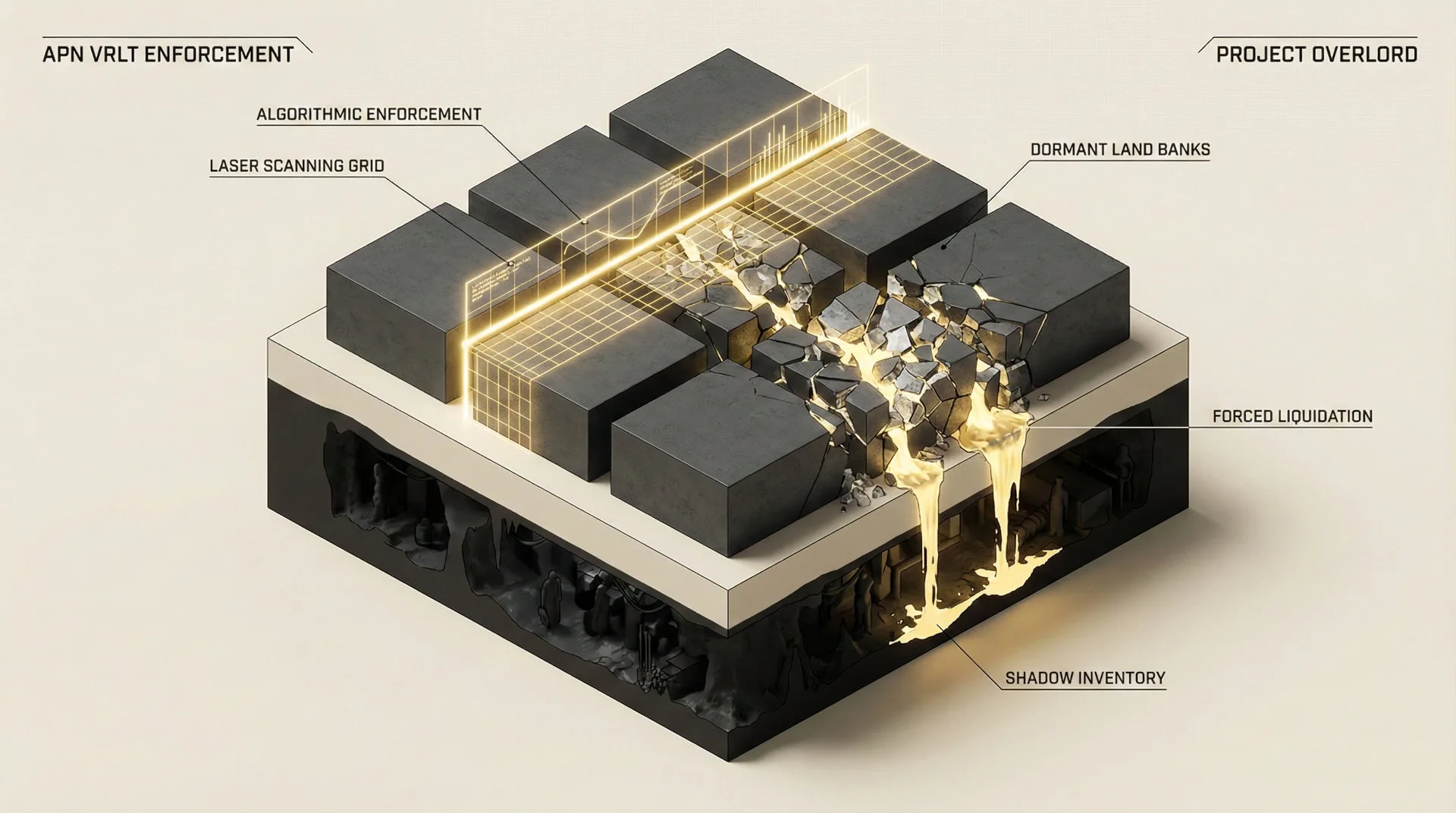

Regulatory Enforcement Velocity (APN Risk & Compliance Index™ (24200)): The ATO’s release of Draft Ruling TR 2025/D1 and PCG 2025/D7 represents a significant increase in regulatory velocity. The “traffic light” risk matrix and the reversal of the burden of proof onto the taxpayer quantifies the operational risk of non-compliance, forcing a market-wide exit before the 1 July 2026 compliance deadline and validating the predictive power of our risk frameworks.

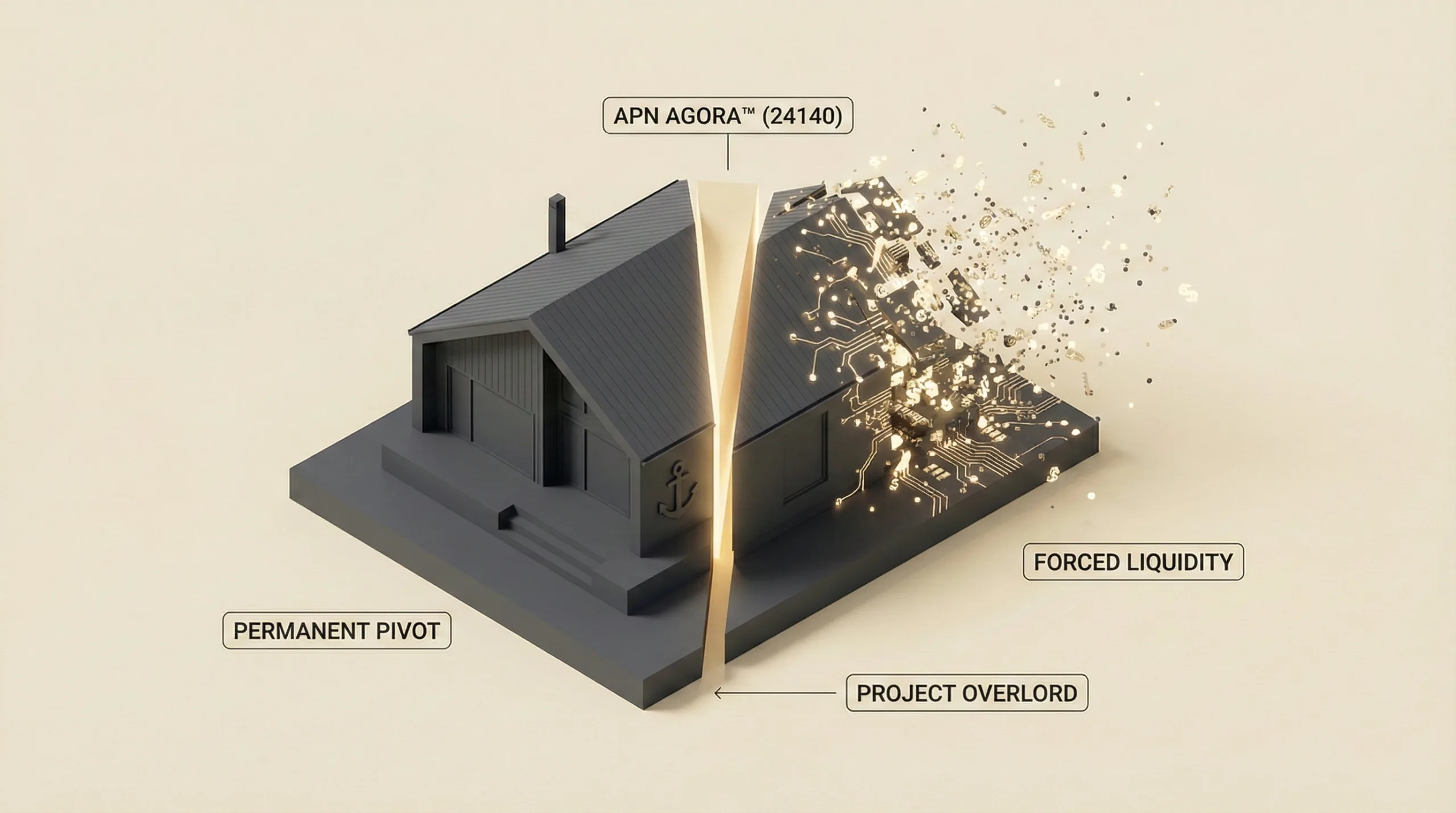

Lifestyle Ecosystem Resilience (APN Agora™): The analysis serves as an elevated stress test for this index. The core question is whether the underlying amenity and access value (the “Agora”) is sufficiently robust to attract a new class of permanent residents to absorb the supply-side adjustment, or if the fiscal pressure on owners will propagate through the commercial ecosystem, diminishing the Agora itself and triggering a more material valuation correction.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of regulatory filings from the Australian Taxation Office (ATO) and the Victorian State Revenue Office (SRO), combined with market listings data and municipal budget analysis. The key facts are:

- Federal Reclassification (TR 2025/D1): The ATO has reclassified holiday homes used or held for personal use as “Leisure Facilities,” denying all deductions for ownership costs like interest and rates under Section 26-50 of the ITAA 1997. This is a binary switch from a tax-advantaged asset to a post-tax consumption item.

- Convergent State-Level Levy (VRLT Expansion): From 1 January 2026, Victoria’s Vacant Residential Land Tax (VRLT) expands statewide, imposing a 1% tax on the Capital Improved Value (CIV) of properties vacant for over six months. This rate escalates to 3% by the third consecutive year of vacancy.

- The Structural Policy Conflict: A “holiday home” exemption exists for the VRLT if an owner proves personal use of at least four weeks. However, this very act of proving personal use provides the ATO with the evidence needed to classify the property as a “Leisure Facility,” thereby triggering the loss of all federal tax deductions.

- Quantified Financial Impact: For a typical $3.0M leveraged holiday home, the combined effect of losing federal deductibility (approx. $67k) and incurring new state taxes (approx. $30k+ VRLT) increases annual holding costs by over $100,000, transforming the asset from a manageable investment into an asset generating a structural loss.

- Forced Liquidity Event: The observed 18.4% material increase in holiday home listings is a direct, rational response to this financial impact and the ATO’s “transitional compliance” window, which effectively acts as a divestment deadline for owners to exit before 1 July 2026.

Critical Analysis & Balanced View

The central paradox of this event is the “Lifestyle-Fiscal Decoupling.” The underlying value proposition of these coastal hubs, their “Agora” of lifestyle, community, and natural amenity, has not diminished. In fact, it is this very appeal that is attracting the “Permanent Pivot” of equity-rich downsizers and remote professionals. The structural pressure point is not one of demand, but of the ownership model. The market is not undergoing a material valuation correction; it is gentrifying into permanence.

However, this transition is not uniform. The analysis reveals a material bifurcation. In the Mornington Peninsula, the “Permanent Pivot” is robust, supported by its integration into Melbourne’s commuter infrastructure. This provides a solid demand floor to absorb the divested assets. In contrast, Byron Bay’s elevated price-to-income disconnect and its relative isolation create a “liquidity trap.” Without a natural buyer pool of permanent residents, the forced sales risk a more material price correction and a second-order contraction in the commercial sector, transitioning a high-amenity, low-integration market into a locality with diminished economic activity.

The long-term risk, particularly for regions like Byron Bay, is the degradation of the APN Agora™. As councils face constraints with a mismatched ratepayer base and high tourist load, they may resort to “user-pays” models and infrastructure trade-offs. This can erode the very “Natural Commons” and “Third Place Density” that justify the price premium, creating a self-reinforcing structural condition where fiscal pressure adversely affects the real economy.

Strategic Implications for Property Professionals

- For Agents & Buyers’ Agents: Segment your client base immediately. The “leveraged professional” is now a motivated seller; target them for listings. The “equity-rich owner-occupier” is the new buyer; educate them on the opportunity to acquire divested assets in high-amenity zones for permanent living. The key is to reframe the conversation from “investment yield” to “lifestyle acquisition”.

- For Developers & Renovators: Focus on the “Permanent Pivot” conversion. The highest-value opportunity lies in acquiring dated “weekenders” in regions with strong commuter links (e.g., Mornington Peninsula) and repositioning them as high-spec permanent residences. This involves upgrading insulation, heating, and home office connectivity to meet the standards of the incoming Work-from-Anywhere professional class.

- For Valuers & Financiers: Your risk models must be updated. An asset’s valuation is now materially dependent on its owner’s tax status and its suitability as a Principal Place of Residence (PPOR). A property with a clear path to PPOR status has a valuation floor, as it is immune to the VRLT and the ATO’s “Leisure Facility” ruling. Conversely, assets suitable only for holiday letting now carry a significant “holding cost” discount.

- For Commercial Property Managers: The stability of retail precincts in these zones is now directly linked to the success of the “Permanent Pivot.” In Mornington, expect a shift towards service-based tenants (medical, professional services, high-end grocery). In Byron Bay, anticipate continued high churn and vacancy risk in secondary locations as the commercial core faces constraints from a diminishing local economy.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides validation for the APN Sovereign Policy Composite Index™ (SPCI, 24800) macro-thesis, confirming that state-level regulatory and fiscal changes are the primary drivers of market structure. It also stress-tests the APN Agora™ (24140) index, confirming its utility in predicting regional resilience based on underlying amenity and connectivity.

- Index Calibration: The APN Regulatory Velocity Multiplier™ (24210) is calibrated upwards to reflect the ATO’s heightened enforcement posture via PCG 2025/D7. The weighting within the APN Agora™ (24140) index will be adjusted to increase the importance of “commuter infrastructure” as a key indicator of a region’s ability to absorb fiscal pressures through the “Permanent Pivot” mechanism.

- Data Capture: This event triggers a new data capture mandate for the APN Symbiotic Intelligence Network™ (24310). We will now actively track the delta between listing prices for “holiday-only” assets versus “PPOR-convertible” assets within the same postcodes to quantify the “Permanent Pivot” premium and absorption rate.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.