Confirmed: ‘Stacked’ Land Model Establishes New Valuation Floor, Rendering Grazing No Longer Structurally Viable on Marginal Land

APN ANALYSIS: A-251127-AUS131239

Executive Summary

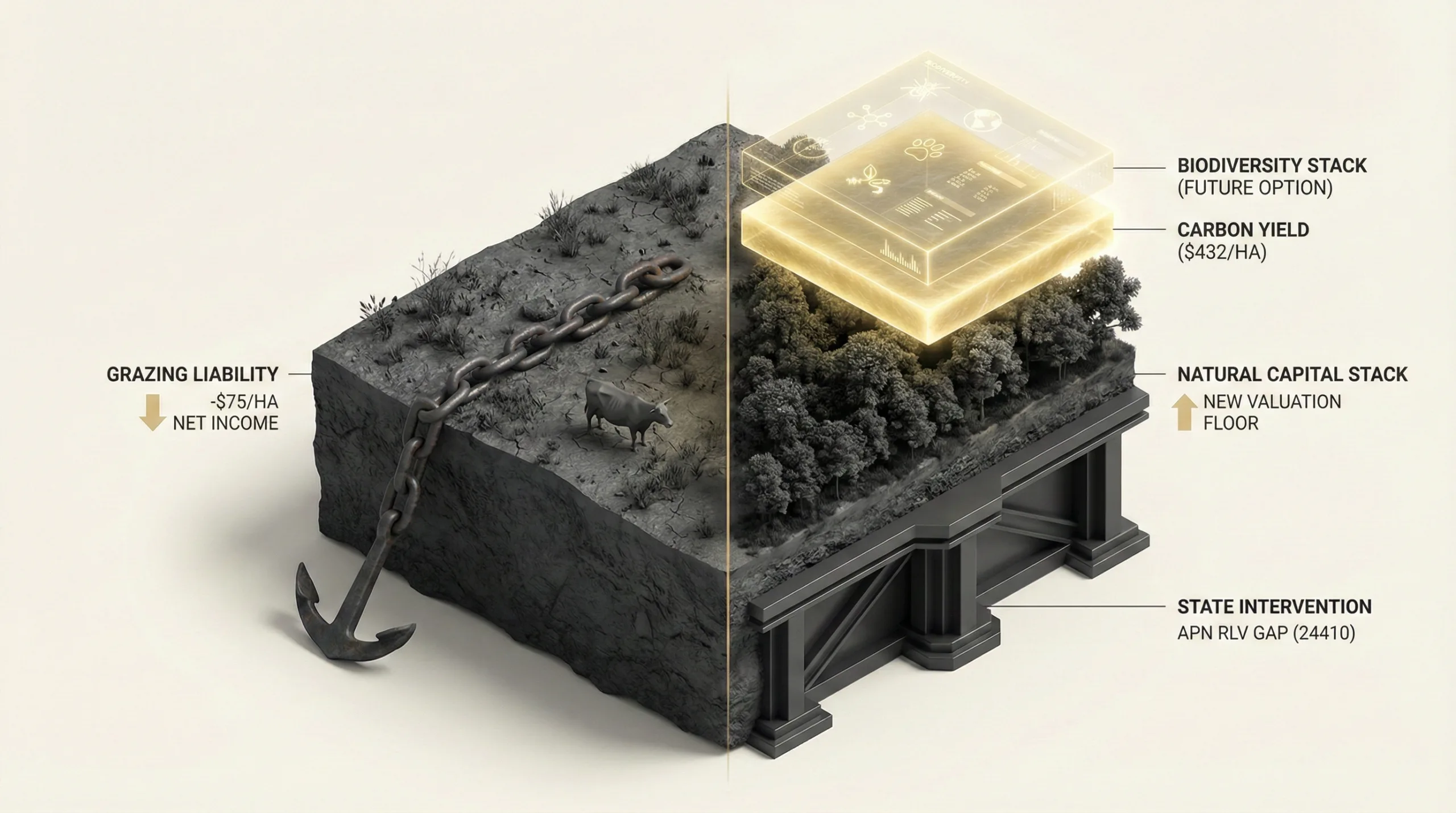

Silva Capital has successfully registered Australia’s first ‘stacked’ environmental project, concurrently generating carbon credits and biodiversity certificates on the same parcel of land at its Cooplacurripa Station. This registration (Project ID NR001014) provides the first legal and financial proof-of-concept for a ‘Natural Capital Yield’ model, validating the hypothesis that revenue from ecosystem services can structurally outperform traditional agriculture on marginal land. APN analysis of the project’s economics reveals the carbon-only revenue stream is approximately 500% higher than the net operating profit from grazing on the same ‘unimproved’ land class.

For property professionals, this event signals a fundamental and irreversible shift in rural asset valuation. The long-standing ‘Beast Area Valuation’ (BAV) model is now directly challenged by a ‘Natural Capital Yield’ (NCY) framework, particularly for land previously considered low-value. This creates a new class of buyer—institutional, compliance-driven capital—and establishes a new highest-and-best-use case for substantial tracts of Australia’s grazing country. Valuers, agents, and investors must now recalibrate their assessment of marginal assets to account for their potential as high-yielding environmental securities.

Background & Strategic Context

This event validates and calibrates APN’s core thesis that state-level intervention is the primary driver of market value (APN Sovereign Policy Composite Index™ (SPCI, 24800)). The creation of the Nature Repair Market and its legislated ability to interact with the existing ACCU scheme is a clear example of a regulatory act creating a new asset class and a new form of property right from a previously under-valued substrate. The Cooplacurripa project is the first registered application for this new market architecture.

A Direct Act of State Intervention (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The legal ability to ‘stack’ a Nature Repair project on top of a Carbon Farming project does not exist in an un-regulated market; it was explicitly created by the Federal Government through the Nature Repair Act 2023 and its interaction with the Carbon Credits (Carbon Farming Initiative) Act 2011. This is a direct sovereign policy intervention that has established a new mechanism for land monetisation.

A Framework Favouring Institutional Capital: The model’s complexity, long-term (100-year) commitment, and reliance on specialised carbon and ecological expertise create high barriers to entry, favouring participation by institutional entities. The Silva Capital joint venture, backed by compliance buyers like Qantas and Rio Tinto, demonstrates a structural outcome where capital is allocated towards entities with the balance sheet and technical capability to navigate these new regulatory markets, which presents a material entry barrier for traditional family-scale operators.

The Financialisation of Climate Compliance (APN Climate-Risk Asset Devaluation Index™ – 24500): The project is a direct response to the compliance liabilities created by the Safeguard Mechanism. Corporates are acquiring these ‘Green Premium’ assets to de-risk their balance sheets against legislated emissions reduction targets, in response to regulatory requirements rather than for non-commercial objectives. This is a tangible example of the APN Financial Climate Sensitivity™ (24510) in action, where land is repriced based on its utility in mitigating climate-related financial risk for its institutional owners.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Clean Energy Regulator’s Biodiversity Market Register, property transaction records, and corporate disclosures. The key facts are:

- Project Registration: Silva Capital Operating Company Pty Ltd successfully registered Project ID NR001014 on 12 August 2025, the first project under the new Nature Repair Market framework.

- The ‘Stack’ Confirmed: The official register provides direct evidence of the model, stating a 100% material overlap between the 438.54-hectare biodiversity project area and a pre-existing ACCU Scheme project (ERF201057).

- The Acquisition Premium Paradox: Silva Capital acquired the ~23,000ha Cooplacurripa Station for ~$50 million in September 2024. The 42.8% price uplift since its 2021 sale correlates closely with regional grazing land inflation (~46.1%), indicating no ‘green premium’ was paid at acquisition. The carbon and nature rights were effectively a free option.

- The Disproportionate Yield Delta: APN analysis indicates the ‘stacked’ model generates an estimated gross revenue of ~$432/ha/year from carbon credits alone (priced at a premium for their environmental co-benefits). This materially exceeds the estimated net operating profit of ~$60-75/ha/year from traditional grazing on the same ‘unimproved’ land.

- The Liquidity Structure: The model is de-risked via a built-in offtake agreement. The fund’s investors (Qantas, Rio Tinto, BHP) are compliance buyers who need the ACCUs to meet their Safeguard Mechanism obligations. The Biodiversity Certificates, for which no market currently exists, are held as a zero-cost, long-term option.

Critical Analysis & Balanced View

The ‘Zero to One’ hypothesis is confirmed, but its operational reality is nuanced. The model’s financial viability currently rests on a single pillar: its dependence on carbon credit revenue. The entire revenue stream depends on the ACCU price, specifically the significant premium that high-integrity ‘Environmental Planting’ credits command over generic units. The Biodiversity Certificate’s current role is not as a direct revenue source, but as a ‘quality multiplier’ that validates the premium pricing of the carbon credits. Should that premium erode or the ACCU price undergo a material contraction, the model’s superior returns would be materially reduced, as the biodiversity market itself remains in a condition of material liquidity constraint.

Furthermore, the ‘Pilot vs. Portfolio’ scale discrepancy is material. The registered ‘stacked’ activity covers only 438.54 hectares, or less than 2% of the total 23,000-hectare station. This reveals a prudent risk-mitigation strategy, proving the model at a pilot scale before encumbering the entire asset with a 100-year land-use commitment. The ‘valuation floor’ thesis, while proven, is currently active on only a micro-segment of the property.

The strategic efficacy of the model lies in its ‘Land Class Arbitrage’. By targeting land that is ‘unimproved’ and agriculturally marginal, Silva Capital has acquired a substrate that is a liability for grazing but a prime asset for reforestation-based carbon and nature repair methodologies. They have successfully arbitraged the gap between two competing valuation logics, using institutional capital to reprice the station’s lowest-value hectares into its highest-yielding asset class.

Strategic Implications for Property Professionals

- For Valuers & Rural Agents: The ‘Beast Area Valuation’ (DSE/ha) is now an incomplete metric for assessing marginal land in high-rainfall zones. A ‘Natural Capital Yield’ (NCY) assessment, which audits a property’s eligibility for carbon and nature repair methodologies, is now essential. Expect a two-tiered market to emerge for ‘unimproved’ land, separating eligible from ineligible parcels.

- For Investors & Fund Managers: The Cooplacurripa project provides a replicable template for acquiring rural assets at agricultural parity and manufacturing a ‘green premium’ post-acquisition. The key success factor is securing compliance-driven offtake for the carbon component to de-risk the investment and fund the initial CapEx, while retaining the biodiversity asset as a future upside option.

- For Agribusiness & Pastoral Companies: Owners of large-scale grazing aggregations with significant tracts of ‘unimproved’ or historically cleared country are now holding a potentially valuable, unrealised financial option. A strategic review of land portfolios is indicated to audit for eligibility under environmental market methodologies and to calculate the opportunity cost of continued grazing versus a transition to natural capital production.

- For Buyers’ Agents & Consultants: A new client class has been solidified: compliance-driven corporates and institutional funds seeking nature-based solutions. Servicing these clients requires deep expertise in environmental markets, regulatory frameworks (CER, Safeguard Mechanism), and project methodologies—a skillset that represents a significant competitive advantage over traditional rural property advisory.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the core tenets of the APN Sovereign Policy Composite Index™ (SPCI, 24800), demonstrating how federal legislation (Nature Repair Act 2023) directly creates new asset classes and reprices land. It also provides a direct case study for the APN Climate-Risk Asset Devaluation Index™ (24500), showing a ‘Green Premium’ being manufactured to satisfy compliance demand from Safeguard Mechanism facilities.

- Index Calibration: The APN Regional Green Premium Uplift™ (24520) will be calibrated to track the valuation delta between land eligible for ‘stacking’ and purely agricultural land within the same region, using Cooplacurripa as the baseline. The APN Regulatory Velocity Multiplier™ (APN RVM™) (24210) will now incorporate the registration and issuance rates from the Biodiversity Market Register as a new data feed to measure market maturity.

- Data Capture: This triggers a new data capture mandate under the APN Symbiotic Intelligence Network™ (24310) to monitor all projects on the Biodiversity Market Register, specifically tracking the percentage of ‘material overlap’ with ACCU scheme projects. This will provide a leading indicator for the adoption rate of the ‘stacking’ model across the Australian land sector.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.