Synthesising findings from the APN Research Report: The Australian Property Market: Economic Driver or Diversification Drag?

The APN Research Report, “The Australian Property Market: Economic Driver or Diversification Drag?”, paints a complex picture of the Australian economy. While acknowledging the significant economic contributions of the property and construction sectors (Section II.A, ref 5, 7), its deeper analysis points towards structural vulnerabilities and reinforcing mechanisms that, if left unaddressed, could steer Australia towards a future far less prosperous and dynamic than its current high-income status suggests. The report provides compelling evidence to argue that our failure to diversify, innovate, and break free from the gravitational pull of established sectors like property and resources risks not just slower growth, but a potential future stagnation with limited opportunities for subsequent generations.

The Flashing Red Light: Declining Economic Complexity

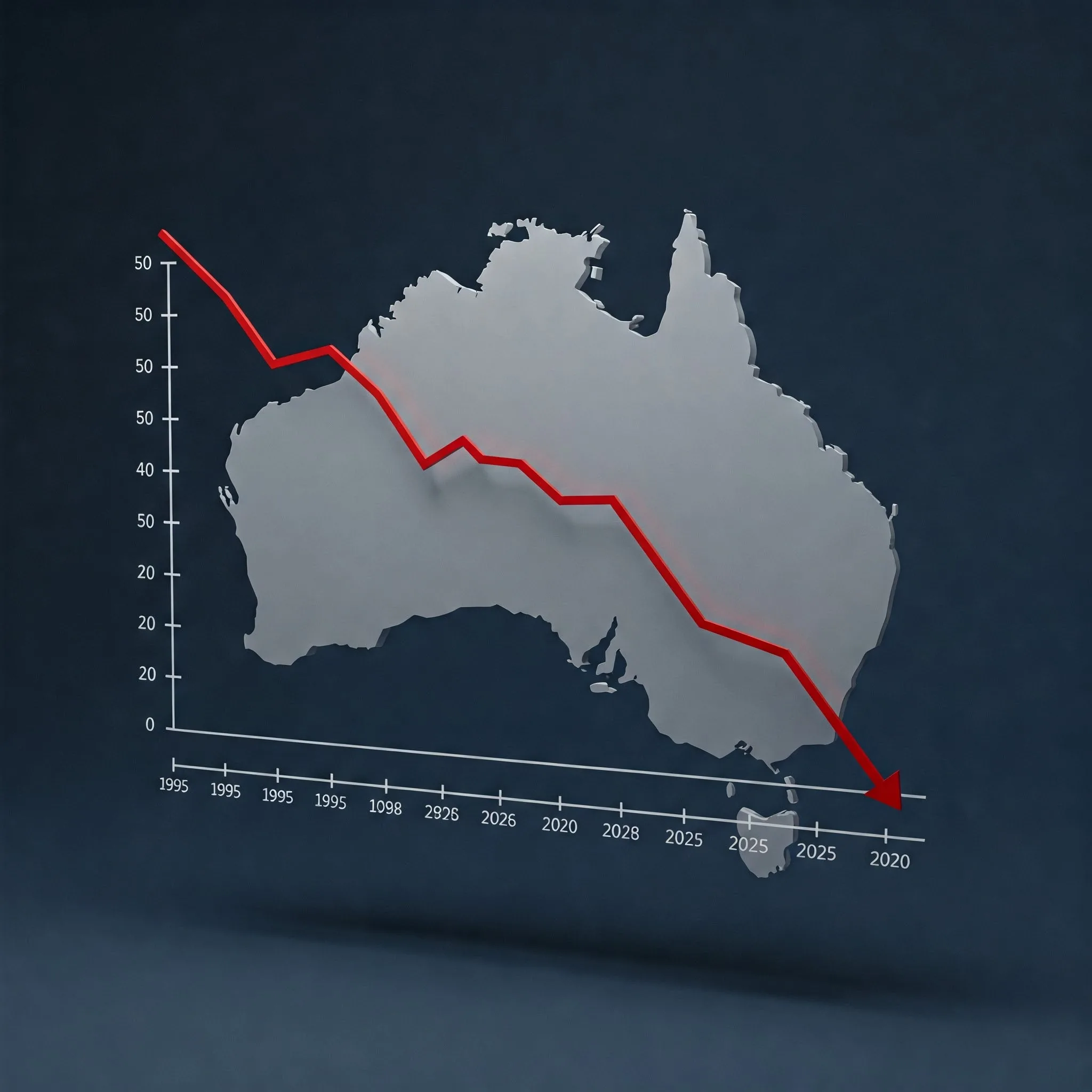

The most potent warning signal highlighted in the report is Australia’s performance on the Economic Complexity Index (ECI) (Section IV.A). This isn’t merely an academic footnote; it’s a fundamental measure of the productive knowledge and capabilities embedded within our economy, revealed through the sophistication and diversity of what we export (Section IV.A, ref 45, 46). The findings are stark and deeply concerning:

- Alarmingly Low Ranking: Australia ranks 99th out of 145 countries (2023 data), placing us consistently as the lowest-ranked OECD nation, sometimes by a significant margin (Section IV.A, ref 3, 4). This puts us alongside developing nations like Uganda and Pakistan in terms of economic structure, despite our vastly higher GDP per capita (Section IV.A, ref 4).

- Worsening Trend: Critically, this isn’t a static problem; it’s getting worse. The ranking has declined significantly over time – from 55th in 1995, fluctuating in the 60s-90s through the 2000s/2010s, and hitting 99th recently (Section IV.A, ref 4, 50, Table 4). We are actively losing ground relative to other nations in developing sophisticated, productive capabilities.

- Root Cause – Lack of Diversification: The report identifies the primary driver as a persistent failure to diversify our export base beyond low- and moderate-complexity products, overwhelmingly dominated by minerals and some agricultural goods (Section IV.A, ref 1, 3). We simply haven’t added enough new, complex products to what we sell the world (Section IV.A, ref 52).

This backward progression on the ECI is the central pillar of the potential negative trajectory. It signifies an economy whose underlying structure is becoming less sophisticated relative to global peers, directly contradicting the path typically taken by advanced nations.

Reinforcing Mechanisms: How Property and Resources Lock Us In

The report argues that this low-complexity trap isn’t accidental; it’s reinforced by powerful structural dynamics where the property market plays a significant role:

- Capital Allocation Bias: The sheer scale of the property market and its deep integration with the financial system creates a powerful gravitational pull for capital. Residential mortgages dominate bank loan books (Section II.C, ref 15, 24, Table 1). The report cites evidence suggesting this focus can “crowd out” lending to businesses, particularly innovative SMEs that lack the property collateral banks often prefer (Section V.A, ref 30, 31). Billions in capital flow towards housing assets, potentially starving the nascent, complex industries needed for diversification of essential funding. This isn’t just about less funding; it’s about systematically favouring lower-complexity asset accumulation over higher-complexity productive investment.

- Human Capital Misallocation: A complex economy requires a skilled workforce deployed effectively. While Australia has educated citizens, the report points to significant labour market frictions. Skills mismatches see qualified individuals working below their capacity (Section IV.B, ref 63, 64), representing wasted potential. Furthermore, the immense demand from the large property/construction and resources sectors likely draws a disproportionate share of skilled labour (engineers, project managers, trades) away from potentially smaller, emerging high-tech sectors where they are also critically needed (Section IV.B, ref 56). We might be training people for the future, but deploying them primarily in the industries of the past.

- Innovation Deficit: While the report specifically highlights the construction sector’s low rate of innovation uptake (Section II.A, ref 10), the broader context of declining ECI implies a wider national challenge. An economy focused heavily on extracting resources and trading existing properties may lack the incentives, risk appetite, and ecosystem support required for the deep, technology-based innovation that underpins complexity growth in sectors like advanced manufacturing, biotech, or complex services.

- Path Dependency and Policy Inertia: The historical success built on resources and property has shaped our institutions, financial systems, regulations, and even political discourse (Section V.C). This creates powerful feedback loops – rising property prices encourage more property investment, policy debates fixate on housing affordability rather than industrial strategy, and the financial system optimises for mortgage lending (Section V.C, ref 15). This ‘path dependency’ makes it incredibly difficult to pivot towards new economic structures, even when the need is apparent. The focus remains locked on managing the existing, lower-complexity model rather than actively building a new one.

Painting the Potential Future: Stagnation, Vulnerability, and Diminished Opportunity

If these trends identified in the report continue unchecked, the long-term outlook deviates significantly from the narrative of perpetual Australian prosperity. The potential negative elements emerge not as a sudden collapse, but as a slow erosion of dynamism and opportunity:

- Persistent Economic Stagnation: The Harvard Growth Lab’s forecast of 1.0% annual growth to 2033, based on our low ECI, is a direct consequence (Section IV.A, ref 3). This isn’t just a temporary slowdown; it reflects a future where Australia consistently underperforms compared to more complex, adaptable economies. Living standards may plateau or even decline relative to global peers.

- Heightened Vulnerability and Lack of Resilience: An economy heavily reliant on volatile commodity exports (Section V.B, ref 2) and a sensitive property market (Section V.B) is inherently fragile. It’s poorly equipped to handle external shocks, whether they be fluctuations in resource prices, global pandemics, geopolitical tensions impacting trade partners (Section V.B, ref 1), or the profound structural shifts underway globally – particularly the transition away from fossil fuels (directly threatening our major exports) and the rise of AI and automation (favouring economies with high-tech capabilities) (Section V.B, ref 54). Without diverse, complex industries, we lack the shock absorbers and alternative growth engines needed to navigate turbulence.

- Shrinking Opportunities for Future Generations: This is perhaps the most concerning implication. A stagnant, low-complexity economy primarily offering jobs in resource extraction, construction, and related services provides a narrower range of high-value, knowledge-intensive career paths for our children and grandchildren. They inherit an economy less capable of generating cutting-edge industries and the high-paying jobs associated with them. The “lucky country” moniker becomes tragically ironic if future generations face constrained choices and lower relative prosperity due to the structural limitations solidified today. Their opportunities will be dictated by the legacy of our failure to diversify.

- Exacerbated Social Divisions: The report touches on how rising property values benefit existing owners while harming renters and first-home buyers, widening wealth inequality (Section II.B, ref 22, 23). An economy overly reliant on asset inflation and resource rents, rather than broad-based productivity gains in diverse industries, risks further entrenching these divisions. A stagnant economy with concentrated wealth is often a less fair and stable one.

- Erosion of National Standing and Agency: An economy that primarily supplies raw materials and imports complex technologies risks becoming a perpetual price-taker in global markets. Our influence diminishes if we are not contributing significantly at the forefront of innovation. We become increasingly dependent on the technological and economic dynamism of others, potentially limiting our strategic autonomy and control over our national destiny.

Conclusion: A Call to Redirect Based on Evidence

The APN Research Report, through its meticulous analysis of Australia’s economic structure, declining complexity, the reinforcing role of the property market, and associated vulnerabilities, lays out a clear and evidence-based warning. While avoiding overly dramatic predictions, the findings strongly point towards a potential future of relative economic decline, increased fragility, and significantly constrained opportunities if current trends continue unchecked. The backward slide on the ECI, coupled with the identified structural impediments to diversification and innovation, signals serious risks to long-term prosperity.

Avoiding this negative trajectory requires acknowledging the profound risks highlighted in the report and undertaking a conscious, strategic effort to break the path dependency. It necessitates policies that actively rebalance incentives away from excessive property speculation, foster genuine technological innovation, improve capital allocation towards productive, complex industries, address labour market frictions, and ultimately, shift the national focus from merely managing existing assets to building the diverse, sophisticated, and resilient economy needed for the 21st century. The alternative, strongly suggested by the report’s findings, is a slow drift towards a future where Australia’s economic dynamism fades, and the opportunities for its descendants are notably diminished compared to the potential.

Disclaimer: This exploration synthesises interpretations and findings presented in the “APN Research Report: The Australian Property Market: Economic Driver or Diversification Drag?”. Readers are encouraged to consult the full report for detailed analysis and specific references.