AUS-156-S — The New Contract: What Australia’s Structural Sentiment Shift Means for the Property Market from 2027

Research Preface

Australian Property Network (APN) is an independent property intelligence platform. It carries no commercial affiliations, accepts no advertising revenue, and maintains no relationships with real estate industry bodies, developers, or financial institutions. Its sole purpose is to provide honest, evidence-based analysis of the Australian property market, a domain where commercially conflicted voices predominate and genuinely independent research is scarce.

This editorial belongs to the APN 22000 Series — forward-looking insight, operating at the highest editorial risk tier within the APN Codex architecture. The inference-boundary protocol applies throughout: forward claims extend only as far as the evidence established in the cited research series supports. This piece does not present new primary data. It synthesises the analytical conclusions of AUS-156 through AUS-156-4 into a forward-facing editorial read on the structural operating environment the Australian property market is entering.

The APN Clinical Authority standard governs the register throughout. The conclusions presented are measured, evidence-bound, and bounded by probability rather than certainty.

The Contract That Is Ending

For the better part of three decades, the Australian residential property market operated under an arrangement that was never formally written down but was understood by every government that sought office. The arrangement was straightforward: the sovereign’s role was to ensure that the nominal value of residential property did not fall. Fiscal policy, monetary policy, taxation architecture, and planning frameworks were all, to varying degrees, calibrated around this obligation. The political calculus behind it was equally straightforward — the majority of voting-age Australians owned property, and property owners, it was assumed, would punish at the ballot box any government that permitted their wealth to erode.

This was not a conspiracy. It was a rational response to incentives that were genuinely operative. The arrangement held for long enough to become structural — embedded in tax law, in bank lending practice, in superannuation policy, in urban planning, and most importantly, in the mental model that institutional capital used to price risk in the Australian property sector.

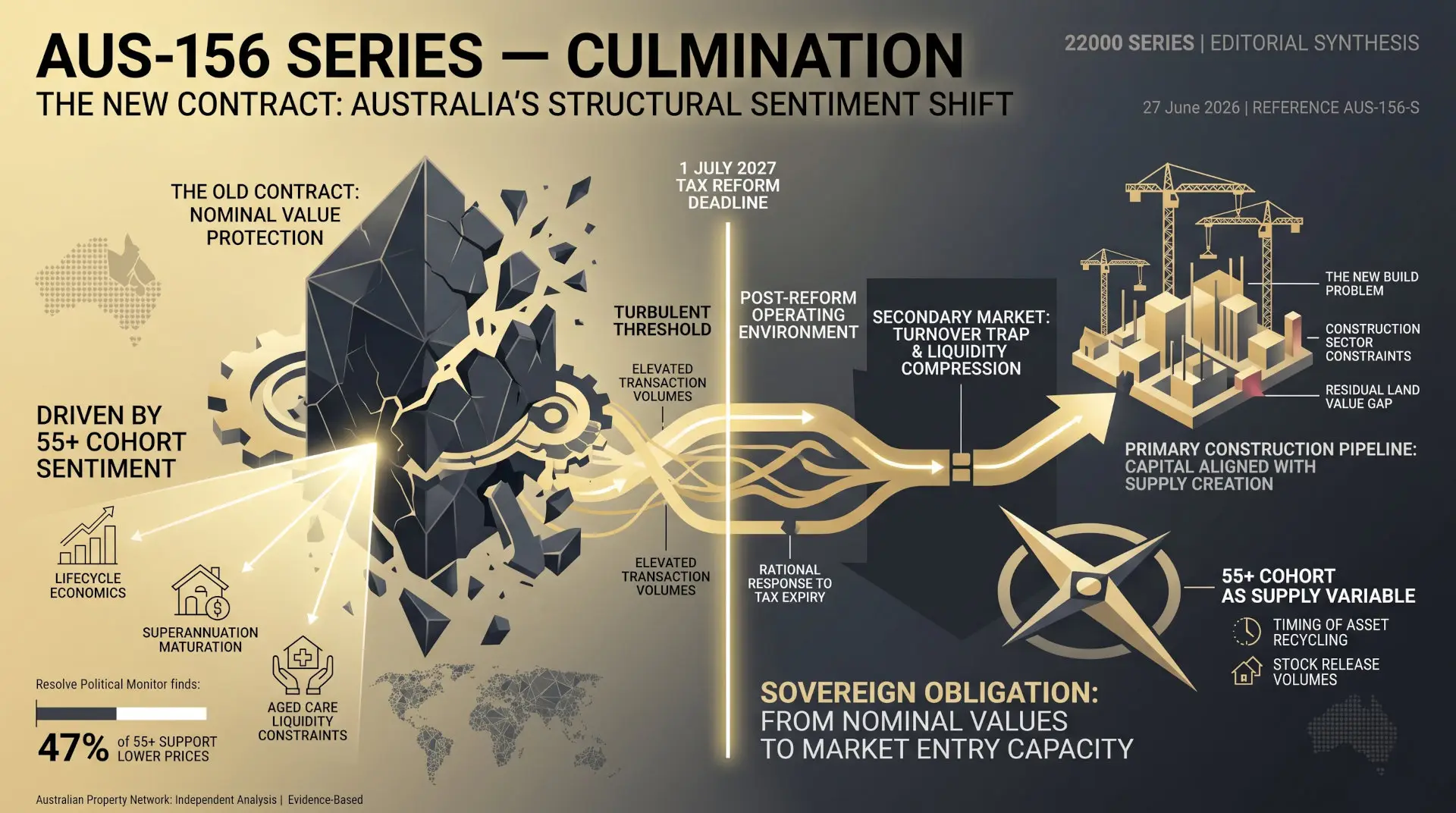

The research collected in the AUS-156 Series documents, with empirical precision, the dissolution of that arrangement. It does not document a softening. It documents a structural transition between operating paradigms — one that is already sufficiently advanced to have produced its first major legislative expression in the Treasury Laws Amendment (Tax Reform No. 1) Bill 2026, and that the weight of evidence suggests will continue to produce further expressions in the years ahead.

The new contract is not yet fully written. But its terms are visible in the data, and they are materially different from the old one.

Why the Shift Is Structural

The most consequential analytical finding across the AUS-156 Series is not the headline statistic — that 54 per cent of the Australian electorate supports lower house prices. Headline polling shifts. The consequential finding is the mechanism driving the 55+ cohort’s position.

This is the demographic that holds the dominant share of unleveraged, freehold residential equity in Australia. Under the logic of the old contract, this cohort was the foundational constituency for nominal equity preservation — the group with the most to lose from any downward movement in asset values, and therefore the group most likely to vote against any government that permitted one. The Resolve Political Monitor records that 47 per cent of this cohort now actively supports lower prices, with only 13 per cent opposed.

AUS-156-4 established why. The answer is not ideological drift. It is lifecycle economics.

The maturation of the compulsory superannuation system has produced a cohort of retirees whose financial security is no longer exclusively anchored to the nominal value of their primary residence. Average superannuation balances for the 60–64 cohort now approach $400,000 for men and $313,000 for women. When the family home is no longer the sole financial lifeline, its nominal inflation becomes less essential to survival — and its associated frictions become more visible.

Those frictions are material. The residential aged care funding model transforms nominal house price inflation into a liquidity constraint. As Refundable Accommodation Deposits track local property values — and the Maximum Permissible Interest Rate has escalated to 7.96 per cent as of April 2026, rising to 8.43 per cent from July — a higher priced local market translates directly into a higher daily accommodation cost for those who cannot immediately liquidate their primary residence. The family home, in this context, is no longer a source of security; it is a liability whose inflation makes the final transition of life more costly, not less.

Simultaneously, the downsizer superannuation contribution scheme — expanded to age 55 in January 2023 — has provided a tax-efficient mechanism for converting illiquid residential equity into liquid retirement capital. The scheme has consistently processed between $4 billion and $5 billion in annual contributions since its inception. The $600,000 per couple cap commands greater purchasing power in a moderated market than in an inflated one. The incentive structure, once understood, points toward moderation rather than inflation.

Add to this the observable fiscal arithmetic: the 2023 Intergenerational Report projects government spending growing from 24.8 per cent to 28.6 per cent of GDP by 2062–63, driven substantially by aged care and health costs in a population where homeownership among the 30–34 cohort has contracted by 18 percentage points since 1981. The 55+ cohort understands, at a practical level, that a retirement system built on the assumption of outright homeownership cannot function if the cohort entering retirement in 2040 is carrying mortgage debt or renting from the private market. Their support for price moderation is, in part, a vote for the sustainability of the system they rely on.

This is not a sentiment that reverses when interest rates move. It is anchored in demographics, lifecycle economics, and fiscal arithmetic. That is what makes it structural.

The Turbulent Threshold

Understanding why the social licence has shifted is necessary but not sufficient. The equally important analytical question is: what does the market actually do now?

The answer, established across AUS-156-1 and AUS-156-3, is that the transition will not be linear. The mechanics of the moment create a period of considerable distortion before the new operating environment takes hold.

The Decoupling Paradox documented in AUS-156-1 remains operative. Property markets clear at the financial margin, not the statistical median. The 54 per cent of Australians who support lower prices do not set the clearing price — the marginal buyer with the deepest credit access does. With investor lending growing at 25.3 per cent annually and 236,858 dwellings trapped in a construction pipeline that is not delivering them, the physical scarcity that maintains the price floor has not disappeared. The expanded social licence changes what governments are permitted to do. It does not change the supply-demand arithmetic in the short term.

What it does change — and this is the source of the turbulence — is the tax structure governing the secondary market from 1 July 2027. That date creates a defined temporal boundary, and defined temporal boundaries in regulatory environments generate predictable behavioural responses. Rational market actors holding investment properties grandfathered under the legacy negative gearing and CGT regime face a choice: sell before July 2027 and realise capital gains under the concessional rules that have governed the sector for decades, or hold and retain the grandfathered status while accepting that future disposals will incur the 30 per cent minimum tax on real gains.

The data indicates that a material proportion of that cohort will choose to sell before the deadline. This is not speculation — it is the expected rational response to an expiring tax concession, consistent with how similar regulatory boundaries have operated in analogous international contexts. The secondary market in the 12 months preceding July 2027 is likely to be characterised by elevated transaction volumes, regulation-driven rather than demand-driven, potentially producing a temporary escalation in prices as competing buyers — themselves seeking to acquire grandfathered assets before the deadline — absorb the increased listings.

The paradox of reform, in its opening phase, is that it may briefly accelerate the very conditions it is designed to alleviate.

After the deadline passes, the secondary market enters the phase AUS-156-3 identified as the turnover trap. Incumbent holders who did not sell retain their grandfathered status and have every incentive to preserve it. Any transaction — upgrading, downsizing, rebalancing — forfeits the legacy tax treatment and triggers the new regime. The rational holding strategy for a grandfathered investor is to hold. Secondary market listings will contract. Transaction velocity will fall. The market will become thinner, less liquid, and harder to read.

This is not a price crash. It is a structural liquidity compression — and for institutional actors calibrated to the old operating environment’s continuous secondary market churn, it represents a material change in how the asset class functions.

The New Build Problem

The legislative architecture of the new contract is designed to redirect investor capital from the secondary established market into the primary construction pipeline. The mechanism is straightforward and theoretically sound: remove the tax advantage from secondary market holdings, preserve it exclusively for new builds, and watch capital flow toward supply creation.

AUS-156-3 established why this will be more complicated in practice than it is in theory.

The Australian construction sector is operating under material structural constraint. The ABS 6427.0 Producer Price Index for construction inputs has escalated from a base of 116.9 in December 2020 to 159.5 by December 2025 — a sustained 36 per cent uplift in the cost base that has not reversed. The APN Residual Land Value Gap™ — the chasm between what land vendors expect to receive and what developers can afford to pay after accounting for construction costs, financing margins, and risk — is wide and not narrowing. High-density approvals contracted 26 per cent in a single month in January 2026. The pipeline is not in a position to receive a large capital inflow and translate it efficiently into completed dwellings.

The international evidence is instructive. The UK Help to Buy scheme and the Canadian First Home Savings Account both directed capital toward primary market participation in supply-constrained environments. In both cases, the capital did not produce proportionate supply — it capitalised into elevated purchase prices for the constrained pool of available new dwellings, transferring the value of the tax concession to developers and landowners rather than to buyers or supply volume. Singapore avoided this outcome by imposing mandatory five-year completion timelines on developers and maintaining direct state land supply — mechanisms the Australian framework does not replicate.

The likely transitional outcome in the Australian primary market is not affordability. It is a structural premium on deliverable new build stock, as redirected investor capital competes for a pipeline the construction sector cannot rapidly expand. Whether this resolves into sustained supply growth depends not on the tax mechanism — which can only alter capital flows, not construction physics — but on whether the underlying structural constraints in the construction sector are independently addressed.

This is where the new contract remains unwritten. The fiscal and regulatory architecture is in place. The supply delivery architecture is not.

The 55+ Cohort as the Supply Variable

The most consequential unknown in the Australian property supply equation over the next decade is not the construction pipeline. It is the timing and volume of the 55+ cohort’s decision to release housing stock back into the secondary market.

AUS-156-4 established the structural logic driving this cohort toward eventual asset recycling: the aged care liquidity mechanics, the superannuation incentives, the diminishing utility of holding large family homes with elevated maintenance costs and no further compounding tax advantage. The direction of the incentives is clear. The timing is not.

The Productivity Commission has documented that older Australians face material barriers to downsizing — inadequate age-specific housing stock, inconsistent state planning frameworks, and punitive stamp duty transaction costs that erode the financial rationale for moving even when the economic logic is sound. These barriers mean that the sentiment shift documented in the Resolve Political Monitor does not immediately translate into supply. The willingness to see prices moderate does not automatically produce the listing behaviour that would achieve it.

If sovereign policy continues to reduce transaction friction for this cohort — through stamp duty reform, accelerated planning approvals for age-specific housing, and further expansion of the downsizer mechanism — the release of large family homes into the secondary market at scale represents an organic supply response that the construction sector cannot provide. The secondary supply that the 55+ cohort holds is located overwhelmingly in established, infrastructure-rich suburban corridors — precisely the locations where demand from younger cohorts is most concentrated. If that stock releases in volume, it addresses the affordability problem more directly than new greenfield supply. If it defers, the liquidity compression of the turnover trap deepens.

The 55+ cohort’s asset recycling behaviour is not a side variable in the Australian housing supply equation. It is a central one.

The Cascade Has Momentum

One of the clearest conclusions from AUS-156-2 is that the CGT and negative gearing reform is explicitly characterised by its architects as a prototype, not a final state. The regulatory cascade it documents — federal taxation reform, state planning overrides, APRA macroprudential calibration — is a coordinated architecture with institutional momentum.

APRA has signalled readiness to deploy investor-focused lending limits if the DTI framework does not sufficiently moderate speculative secondary market activity. State governments in New South Wales and Victoria have stripped discretionary refusal powers from local councils — a structural change to planning frameworks that cannot easily be reversed without legislative action. The Senate Select Committee on Intergenerational Housing Inequality is building the empirical justification for further interventions in residential tenancy law and social housing provision.

The question is not whether further regulatory intervention occurs. The structural logic of the expanded social licence and the acknowledged inadequacy of a single tax reform to resolve a multi-decade supply deficit makes further intervention likely. The question is what form it takes, and what the sequencing implies for capital allocation in the intervening period.

What This Demands

The APN 22000 Series does not issue recommendations. What it offers is a forward assessment of the operating environment, derived from the weight of the evidence.

The evidence accumulated across the AUS-156 Series describes a market undergoing a genuine structural transition — not a cyclical correction, not a policy experiment that will be reversed at the next election, but a durable shift in the political economy governing residential property in Australia. The foundations of that shift — demographic economics, fiscal arithmetic, superannuation maturation, aged care mechanics — are structural by definition. They do not respond to sentiment management or short-term rate adjustments.

Institutional frameworks calibrated to the old contract — frameworks that assumed continuous secondary market liquidity, sovereign protection of nominal values, and the political impossibility of structural tax reform — are operating on outdated assumptions. The risk they carry is not that the market will fall sharply. It is that the structural geometry of the asset class is changing in ways that make the old models systematically misleading about where value resides, where liquidity will be available, and where regulatory friction will accumulate.

The new contract’s core terms, as the AUS-156 Series establishes them, can be stated plainly. The sovereign’s obligation is no longer to protect nominal values — it is to ensure market entry capacity. Capital that aligns with that objective, by participating in genuine supply creation, will operate with the explicit support of the taxation system, the credit framework, and the planning architecture. Capital that does not will face increasing structural friction.

The transition between these two operating environments — across the turbulent threshold of 2026 and 2027 — will be characterised by distortion, dislocation, and the collision of old behavioural heuristics with new regulatory realities. That is the nature of genuine structural change. The research does not suggest the transition will be smooth. It suggests it is already underway.

Findings are presented on the basis of data and evidence alone.