APN 23000 Series – Industry Voices: 23200 Discovery Layer

APN OPINION: O-260611-139731-HIGH

Observation date: 11 June 2026

22000 Node: 22430 Technological & Innovation Insight

23000 Node Activated: 23200 Industry Voices

Trigger event: Policy Shock & Multi-Node Convergence (OCR 4.35% | APRA Buffer +3.00pp)

Data anchors: Node 21210 (Interest Rates) — Z-Score +1.37σ | Node 21350 (Banking & Lending Regulation) — Z-Score −1.4085σ | Node 21620 (Market Psychology & Herd Behaviour) — Z-Score +0.847σ

Significance rating: HIGH

23000 Series — Scope & Inclusion Criteria

The APN 23000 Series constitutes the attributed opinion and industry voices layer of the APN Codex. Content published under this series presents the recorded perspectives of identified practitioners, researchers, and subject matter experts whose observations carry direct evidential relevance to active node conditions. Inclusion is governed by the APN 23000 Series Curation Protocol: contributors must hold demonstrable professional standing within their domain, statements must be sourced and provenance-certified, and the perspective must materially advance or challenge the analytical position established in the corresponding 22000 Series node. This publication is triggered by a Policy Shock & Multi-Node Convergence event and presents discovery-layer voices under Node 23200 (Industry Voices) in direct relation to the findings of APN INSIGHT I-260609-139710-HIGH.

Attributed Perspective — Luke Metcalfe, Founder, Microburbs

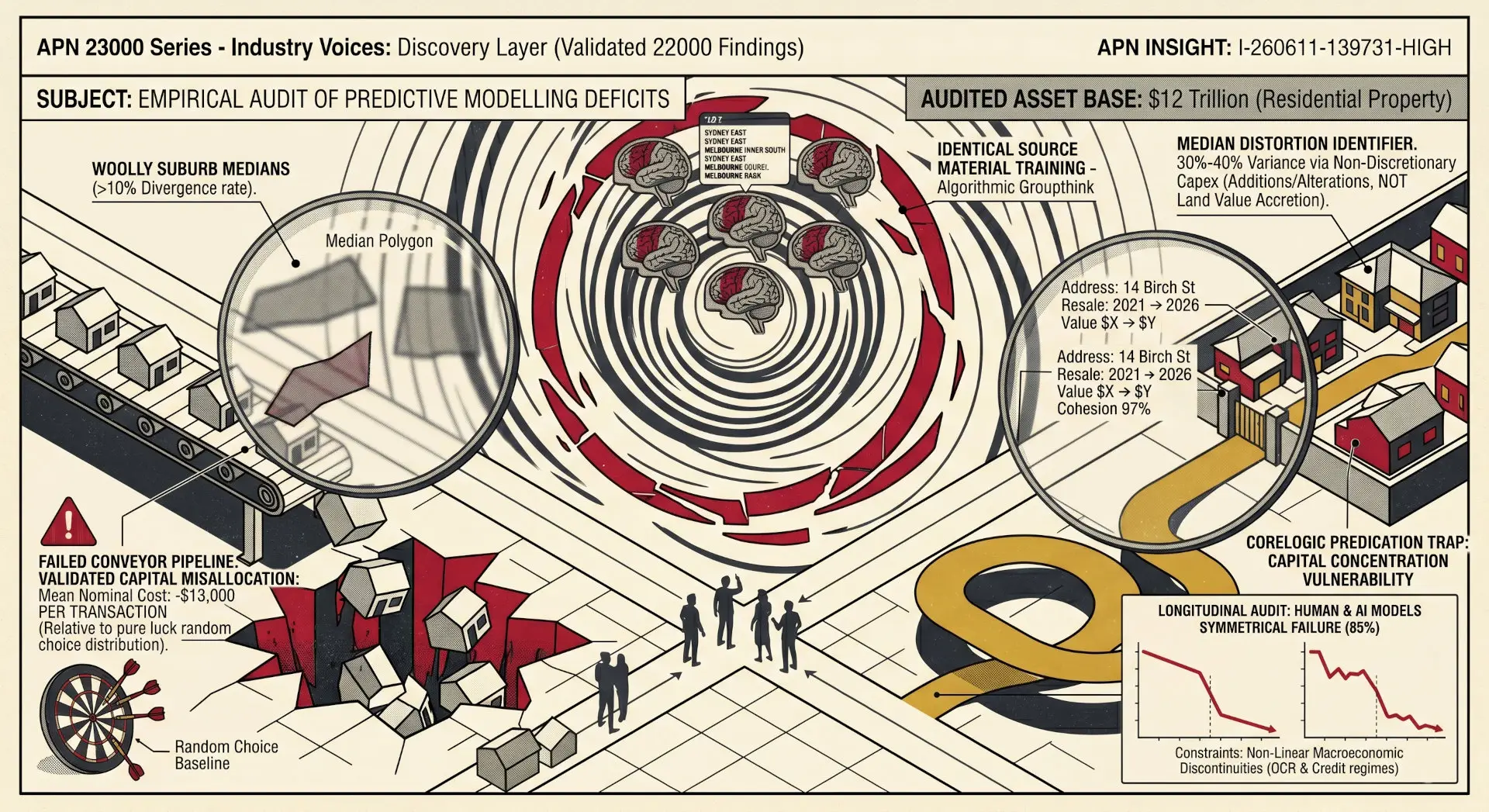

“Imagine you asked seven different analysts to pick Australia’s top growth suburbs and they all came back with the same list. Not because they compared notes or even used the same methodology, but because they’d all inadvertently been trained on identical source material before they’d even started. If that could happen, every investor using an AI tool to find the next growth opportunity is essentially asking the crowd what the crowd already believes and paying a premium to buy into it.

The upshot is that it underperformed the market. So you would have been better off choosing at random. If you threw a dart at each capital city across the country across time, it underperformed the market. On average you would have lost about $13,000 listening to ChatGPT versus just randomness — pure luck. It was really bad at forecasting and of course it’s not designed to do forecasting. It’s not trained on the future like that. It’s trained on the next word. So it’s coming up with things that sound good, things that fit — commentary that fits your question — but it’s trained on all these top lists that are coming out, all this promotional copy, and it comes up with very generic answers.

All this whole spreadsheet modelling based on these woolly medians — the median, you can debate endlessly what a median price is anyway. So much of our research, increasingly I try to do all of our research now looking at resales and not median values. What is the actual return? An individual bought one home on this date, they sold later at this date — what’s the growth, what are their costs? On that basis it’s much better because you can look at the actual fine-grain location context.”

Source: The Elephant In The Room Property Podcast, Episode: “Luke Metcalfe: Why AI Can’t Pick Property Winners” | Hosts: Veronica Morgan and Chris Bates | https://youtu.be/h2MEhzrXHbE?si=mxh927Ic1WLXu2NG | Retrieval date: 9 June 2026

APN Clinical Reframing

The empirical testing executed by Metcalfe establishes an explicit underperformance baseline for linguistic autoregressive models applied to spatial value forecasting. In a calibrated baseline audit tracking seven discrete transformer configurations across 17,000 historical suburb records over a 38-month observation window, 6 out of 7 models systematically underperformed simple randomised distribution variables. This structural deficit incurred a mean nominal capital misallocation cost of $13,000 per transaction relative to baseline market momentum.

Metcalfe’s data confirms that generative systems optimise for structural semantic alignment rather than economic rationale, processing commercial promotional text and legacy consensus indexing into a redundant feedback loop. The practitioner’s evidence verifies that the resultant output induces capital allocation replication, structurally funnelling uncalibrated buyers into highly contested asset coordinates that already reflect fully priced-in public narratives. Metcalfe further identifies that the over-reliance on aggregated suburb median price indices introduces a compounding distortion: approximately 30% to 40% of observed positive variance in median prices is driven by non-discretionary capital expenditure on structural additions and alterations rather than actual land value accretion — a distinction that both human and algorithmic forecasting models consistently fail to isolate.

Attributed Perspective — Veronica Morgan & Chris Bates, Hosts, The Elephant In The Room Property Podcast

“Predicting what’s going to happen in the property market — or predicting price growth or price falls for that matter — in any period more than a year, for a human being, has been almost impossible. We wrote five forecaster reports where we reviewed year on year the forecasts that had been made. The best year, 15% of them were somewhat accurate. That means 85% on a good year are way off beam. Most, hands down, were way off beam. So we know that humans can’t predict into the future with property. And what we now know is the AI can’t do it either.”

Source: The Elephant In The Room Property Podcast, Episode: “Luke Metcalfe: Why AI Can’t Pick Property Winners” | https://youtu.be/h2MEhzrXHbE?si=mxh927Ic1WLXu2NG | Retrieval date: 11 June 2026

APN Clinical Reframing

The longitudinal audit data maintained by Morgan and Bates establishes a structural symmetry between the failure rates of generic computational architecture and traditional human forecasting models. Longitudinal tracking across a five-year observation matrix demonstrates that 85% of institutional and media macro-forecasters fail to project transactional or pricing trajectories accurately over extended horizons — returning an identical underperformance vector to that observed in generic automated modelling. The hosts’ observations confirm that both human and algorithmic systems are subject to the same fundamental constraint: an inability to incorporate non-linear macroeconomic discontinuities — policy shocks, credit regime shifts, and structural budget interventions — that fall outside the boundaries of historical training data.

Exploration Candidates

The qualitative data surfaced in the 23200 discovery layer opens material analytical inquiries that warrant formal codification and integration into the downstream research queue:

- The Street-Level Cohesion Rule: Metcalfe’s tracking isolates an acute drop-off in data cohesion across geographic boundaries. While national cohesion tracks at 66% and suburb-level median cohesion features a 1-in-10 divergence rate, street-level transactional records demonstrate a 97% cohesion rate. Further research must formalise a data-ingestion pipeline to isolate street-level resale variables, bypassing woolly suburb medians entirely.

- The CoreLogic Predication Trap: The revelation that commercial PropTech intermediaries rely on identical centralised median data arrays requires an alignment audit to identify capital concentration vulnerabilities before they alter localised credit velocity indicators.

Disclaimer

The analysis, information, and opinions contained in this article are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

The views, thoughts, and opinions expressed in this text belong solely to the author and do not necessarily reflect the official policy or position of the Australian Property Network (APN).

This content may be based on data from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

Property values and market conditions can go down as well as up. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.