AUS-157-S — The Compression Cohort

What structural overservice across Australia’s real estate professional services means for the market’s institutional layer from 2027.

Australian Property Network (APN) is an independent property intelligence platform. It carries no commercial affiliations, accepts no advertising revenue, and maintains no relationships with real estate industry bodies, developers, or financial institutions. Its sole purpose is to provide honest, evidence-based analysis of the Australian property market, a domain where commercially conflicted voices predominate and genuinely independent research is scarce.

This editorial belongs to the APN 22000 Series — forward-looking insight, operating at the highest editorial risk tier within the APN Codex architecture. The inference-boundary protocol applies throughout: forward claims extend only as far as the evidence established in the cited research series supports. This piece does not present new primary data. It synthesises the analytical conclusions of AUS-157 through AUS-157-4 — four independent research streams examining structural overservice and constraint across the Australian real estate sales agency, buyers agent, mortgage broking, and property valuation professions — into a forward-facing editorial read on the structural operating environment those professions are entering.

The APN Clinical Authority standard governs the register throughout. The conclusions presented are measured, evidence-bound, and bounded by probability rather than certainty. Findings are presented as the data dictates, not as any commercial interest would prefer them to be.

The Contract That Is Ending

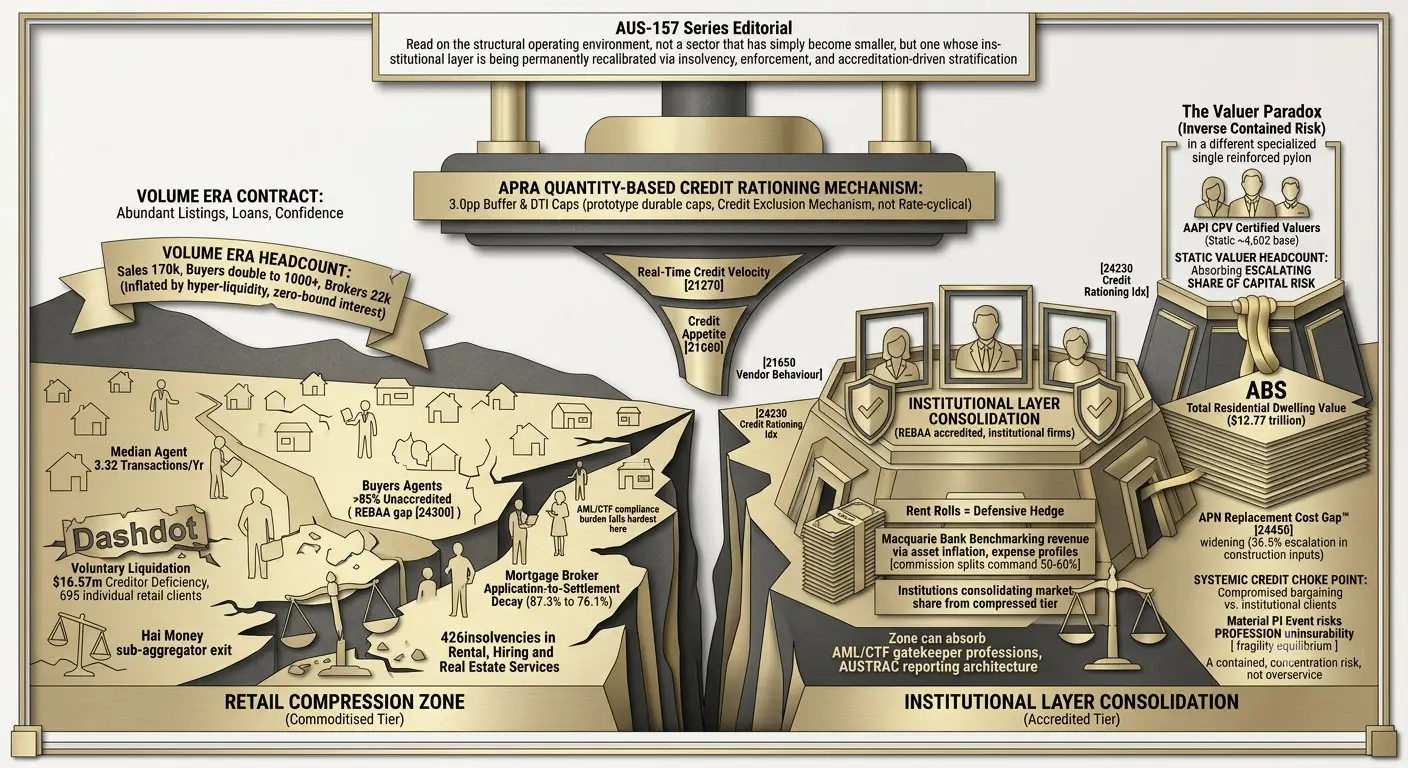

For the better part of a decade, Australia’s residential property professional services layer operated under an arrangement that was never formally written down but was understood by every practitioner who entered the industry after 2013: volume begets viability. More listings meant more agents could survive on thinner per-transaction margins. More loan applications meant more brokers could sustain a business on trail commission alone. More capital in motion meant a buyers agent could enter the market with little more than a phone, a licence, and the confidence that the next boom was never far away. The zero-bound interest rate environment of 2020 and 2021, amplified by the HomeBuilder program and a historic pull-forward of transactional demand, did not simply inflate asset prices — it inflated headcount across every professional tier that services a transaction. The AUS-157 Series establishes the scale of that inflation with precision: an estimated 170,000 licensed real estate agents and representatives operating nationally, a buyers agent cohort that more than doubled from roughly 500 in 2016 to over 1,000 by 2025–26, and a mortgage broker population that reached a record 22,265 in late 2024 — a 34.0 per cent expansion over the preceding five-year baseline.

That headcount was built for a market that, by every empirical measure the Series traces, no longer exists. National residential transactions peaked at approximately 650,175 in 2021. By 2024 they had contracted to 531,573 — a fall of 18.2 per cent — before a modest 2025 recovery to 565,073, a figure that remains 13.1 per cent below the cyclical peak and 6.2 per cent below the trailing five-year average. The professional services layer, in other words, expanded on the assumption of a transaction volume that has not returned and, on the weight of the evidence assembled across this Series, is unlikely to return. The contract that made that expansion rational — cheap credit, abundant transactions, low barriers to entry — has ended. It ended not through a single policy announcement but because the sovereign settled on a fundamentally different mechanism for managing systemic credit risk, one this editorial turns to next.

Why the Shift Is Structural, Not Cyclical

The most consequential finding across the AUS-157 Series is not any single headcount or transaction figure. It is the mechanism by which the Australian Prudential Regulation Authority has re-engineered how credit — and therefore transactional opportunity — is rationed. In 2019, APRA applied a 2.50 percentage point serviceability buffer above the contract mortgage rate when assessing borrower capacity. In October 2021, in response to rising systemic risk, that buffer was raised to 3.00 percentage points — and it has been held there through two subsequent formal reviews, in December 2023 and July 2025, despite the cash rate itself moving substantially in the intervening period. In February 2026, APRA layered a second constraint on top of the buffer: a hard cap limiting new residential lending at debt-to-income ratios of 6x or greater to a maximum of 20 per cent of each lender’s total new loan portfolio.

This distinction matters more than its technical framing suggests. A buffer that sits above the cash rate is, functionally, price-based friction — it tightens and loosens in sympathy with the monetary cycle, and borrowing capacity recovers when rates fall. A DTI cap is quantity-based rationing. It does not loosen when the cash rate falls; it establishes a hard ceiling on the volume of high-leverage credit the system will permit, full stop. The AUS-157 Series terms this the Credit Exclusion Mechanism, and its fingerprints are visible in every professional tier examined. Mortgage broker application-to-settlement conversion rates have decayed from a cyclical peak of 87.3 per cent in mid-2022 to 76.1 per cent by late 2024 — an 11.2 percentage point contraction in the efficiency of converting client intent into settled transactions. Registered auction bidder depth, the clearest real-time measure of actionable buyer liquidity, fell from an average of 8.4 per property at the September 2021 peak to 4.7 by mid-2025, before a marginal stabilisation to 5.1 in early 2026 — a structural contraction of nearly 40 per cent in the deployable buyer pool per available asset. And the agent-to-transaction ratio across the sales agency sector compressed from 3.82 transactions per practitioner in 2021 to 3.32 by 2025.

None of this reverses on a rate cut, because none of it was caused by the price of credit. It was caused by a ceiling on its quantity. Independent modelling commissioned by the Finance Brokers Association of Australasia and conducted by CoreData quantifies the scale of the exclusion directly: reducing the serviceability buffer from 3.00 to 2.50 percentage points would expand national borrowing capacity by an estimated $276 billion and allow approximately 270,000 more Australians to access a median home loan, including nearly 400,000 first-home buyers aged 25 to 34. APRA has shown no indication of making that adjustment. That is what makes this shift structural rather than cyclical — the sovereign’s tool for managing systemic risk has moved from a lever that tracks the interest rate cycle to a cap that does not, and the professional services layer built to service pre-2022 transaction volumes is now operating against a ceiling that a future rate cut will not lift.

The clearest expression of this is what the parent AUS-157 brief terms the revenue illusion. New mortgage commitment values reached $115.2 billion in the December 2025 quarter — nominally exceeding the December 2021 boom peak of $97.2 billion. On its face this looks like recovery. It is not. The corresponding loan commitment count series, published quarterly by the ABS only since December 2024, tells the real story: 149,434 commitments in the December 2025 quarter fell to 139,794 by March 2026, a 6.2 per cent contraction in count terms occurring in the same quarter the dollar value also retreated from $115.2 billion to $92.3 billion. The same, or fewer, transactions are simply clearing at higher prices — not more transactions sustaining more practitioners. Against a national mortgage broker density of one broker for every 1,211 Australian residents, that distinction is the entire structural story in miniature: headline dollar figures can mask a workforce that is still mathematically overserved relative to physical transaction count, no matter how the nominal value series reads.

The Valuer Paradox

Not every profession examined in this Series follows the overservice pattern, and the valuation cohort’s own numbers carry a reconciliation flag worth stating plainly. AUS-157-4 benchmarks against approximately 4,602 active AAPI Certified Practising Valuers — the lender-facing operational cohort. The parent AUS-157 brief’s aggregate headcount table, drawing on the API’s 2024 Annual Report, records a broader institute membership of 7,336, of which over 5,000 are classified as professional valuers. The two figures describe overlapping but not identical populations — CPV-certified lender panel members versus total professional API membership — and this editorial treats the narrower, lender-facing 4,602 figure as the operationally relevant one for settlement-ratio purposes, while flagging the reconciliation as an open item for the Series register rather than resolving it by assumption.

Whichever figure is used, the headcount trajectory itself did not follow the sales agent, buyers agent, or broker pattern of 2020–22 expansion. Statutory deregulation in several jurisdictions removed formal licensing requirements over the past decade, but rather than lowering barriers to entry and expanding practitioner supply, the vacuum was filled by two forces working in the same direction: private lenders imposing their own compliance architecture — mandatory AAPI CPV status, continuous professional development audits, and professional indemnity insurance thresholds most non-institutional operators cannot economically satisfy — and the proliferation of Automated Valuation Models, which the parent brief identifies as having absorbed a material share of standard, low-risk residential valuation work. The profession is bifurcating rather than overserving: algorithmic systems handle high-volume residential originations, while human capital concentrates in complex commercial assessments, specialised agribusiness valuations, and climate-risk modelling. This is a materially different mechanism from the credit-exclusion story driving the other three professions, and it partially insulates valuers from the volume-driven overservice pressure documented elsewhere in this Series — even as it concentrates the surviving human workforce’s liability exposure.

The consequence is a broadly flat headcount absorbing an escalating share of national capital risk. Benchmarked against PEXA’s verified 686,040 national residential settlements for calendar year 2024, the 4,602-strong lender-facing practitioner base implies approximately 149 settlements per valuer annually — before accounting for the refinancing, equity release, and debt consolidation instructions that independently require a fresh security valuation and are not captured in settlement figures at all. Over the same period, the ABS records the total value of Australian residential dwellings rising to $12.77 trillion. The APN Replacement Cost Gap™ — the widening divergence between the cost of constructing an equivalent new dwelling and the market price of existing stock, driven by a sustained 36.5 per cent compound escalation in construction inputs since 2020 — has entrenched a structural floor beneath established asset prices even as physical transaction turnover falls. Every valuation instruction a practitioner signs now carries materially higher absolute dollar exposure than the same instruction carried five years ago, with no corresponding growth in the human workforce absorbing that exposure.

This concentration produces a single-point-of-failure risk that does not exist in the overserved professions. Industry-led initiatives such as the PropSec Discretionary Trust have engineered a plateau in professional indemnity premium escalation, but the underlying structural reality is unchanged: a mathematically capped human headcount, compromised individual bargaining power against institutional client demands, and a liability burden that has never been more asymmetric. A material professional indemnity event affecting a large national valuation firm would not behave like the isolated liquidations documented elsewhere in this Series. It would risk reverting the profession to a state of uninsurability, directly contracting the lending panel capacity of every institution that relies on it — a systemic credit chokepoint distinct in kind from the overservice pattern the rest of this editorial addresses.

The Commercial Escape Valve

Not every practitioner squeezed by the Credit Exclusion Mechanism is exiting the industry. A material cohort is redirecting capacity into commercial lending, and the scale of that pivot is one of the parent brief’s sharpest findings. In the six months to September 2024, the number of brokers writing commercial loans rose 24.21 per cent year-on-year to a record 7,023 practitioners — 31.54 per cent of the entire active broker population. Settled commercial loan values reached $22.68 billion, up 31.2 per cent year-on-year, and the total commercial loan book managed by brokers expanded from $43.1 billion to $85.9 billion over the five years to September 2024. This is a structural bypass, not a diversification strategy in the ordinary sense: practitioners are redirecting operational focus toward a segment where macroprudential intervention has historically been lighter and per-transaction margins are superior, precisely because the residential channel they were built to serve no longer supports full-time viability at 76 per cent conversion.

The concentration of new business is equally telling. MFAA data shows that 72 per cent of top-performing brokers’ new business now originates from existing client networks — 44 per cent repeat clients, 28 per cent referrals. Cold acquisition, the channel a new entrant depends on to establish a book, has become structurally residual. Combined with the commercial pivot, this describes an industry where the viable path forward is not volume growth but relationship depth and product diversification — exactly the institutional-grade capability set that the retail, volume-trained cohort of the 2020–22 expansion was never built around.

The Turbulent Threshold

The professional services layer’s excess capacity is not clearing gracefully, and 2026 through 2027 is where the visible casualties concentrate. The most structurally significant single event in the retrieval window was the voluntary liquidation of Dashdot, one of Australia’s most prominent buyer advocacy firms, on 28 May 2026. The firm ceased operations immediately, made over 40 staff redundant, and left a $16.57 million creditor deficiency — including 695 individual retail clients owed a combined $10.59 million in prepaid fees and refunds. Notably, 96 per cent of Dashdot’s shares had been transferred to an offshore holding company in the British Virgin Islands prior to the collapse. Dashdot’s founder attributed the failure to a convergence of external shocks: the February 2026 DTI caps, RBA rate hikes peaking at 4.35 per cent, the May 2026 federal budget’s 30 per cent minimum tax on real capital gains from July 2027, and restricted negative gearing eligibility. Peak industry bodies rejected that framing outright. PIPA Chair Cate Bakos attributed the collapse directly to financial mismanagement and unsustainable rapid growth; REBAA Vice President Zoran Solano identified the specific mechanism — a volume-based model extracting $15,000 to $20,000 upfront fees to cover operational deficits, built on the assumption that historically low interest rates were permanent rather than cyclical. A subsequent review of the 50 referral agents Dashdot’s liquidator provided to displaced clients found many were part-time operators, several open for less than six months, and a number not even registered for GST — implying annual turnover below $75,000. That is the practical, ground-level texture of the accreditation gap this editorial returns to below.

Dashdot was not an isolated failure. ASIC recorded 426 formal insolvencies in the Rental, Hiring and Real Estate Services sector in the 2025–26 financial year to date. In the mortgage broking channel, the exit of sub-aggregator network Hai Money triggered a wave of forced consolidation among smaller brokerages that had relied on its back-office infrastructure. Regulatory enforcement has escalated in step: NSW Fair Trading’s 2024–25 compliance operations resulted in disciplinary action against 20 real estate agents, $173,500 in financial penalties, eight licence cancellations, and nine immediate management disqualifications for trust account audit failures — part of a broader financial year in which the regulator conducted 2,200 inspections, issued $1.58 million in aggregate fines, and suspended or cancelled 84 licences. On the credit side, ASIC’s Best Interests Duty regime for mortgage brokers carries statutory penalties of up to $1.05 million per breach, a compliance cost structure with no equivalent in the pre-2021 operating environment.

Layered on top of this attrition is the Anti-Money Laundering and Counter-Terrorism Financing Amendment Act 2024’s Tranche 2 reforms, commencing 1 July 2026. The legislation reclassifies real estate agents, buyers agents, and purchaser-facing developers as high-risk gatekeeper professions, bringing an estimated 70,000 additional businesses into AUSTRAC’s reporting architecture, with mandatory enrolment required between March and April 2026 and ongoing obligations including Suspicious Matter Reports and annual compliance documentation. The compliance cost this imposes is not evenly distributed. Independent, low-volume operators — precisely the cohort that entered the industry during the 2020–22 expansion with the least institutional infrastructure, and precisely the profile the Dashdot referral network review exposed — are structurally the least equipped to absorb it. This is the mechanism by which the sector clears its excess capacity: not through an orderly wind-down, but through insolvency, enforcement, and a compliance burden that falls hardest on the operators with the thinnest margin for absorbing it.

The Accreditation Divide: Who Survives

The most consequential unresolved variable this Series identifies is not whether the professional services layer contracts — the data leaves little doubt that it will — but which segment of each profession survives the contraction, and on what terms. The pattern that recurs across all three overserved professions is a widening bifurcation between an institutional, accreditation-heavy tier and a commoditised retail tier facing sustained structural pressure.

In the buyers agent sector, this divide is starkly quantifiable. Against an estimated total practitioner headcount exceeding 1,000, the Real Estate Buyers Agents Association of Australia holds approximately 140 accredited members — meaning over 85 per cent of active buyers agents in Australia currently operate entirely outside peak-body accreditation, professional indemnity standards, and ethical oversight. REBAA’s own leadership has attributed this accreditation gap directly to the systemic influx of inexperienced operators drawn in by low barriers to entry during the 2020–22 upswing. In the sales agency sector, the same dynamic manifests as pareto concentration: elite, top-decile agents and corporate networks now command 50 to 60 per cent commission splits from their employing agencies under the credible threat of defection, while the median practitioner absorbs the sector’s shrinking 3.32-transactions-per-year reality directly. Macquarie Bank’s benchmarking data confirms the mechanism funding this — total industry revenue grew 113 per cent between FY2020 and FY2024, driven almost entirely by asset price inflation rather than transaction volume growth, while expense profiles, particularly commission splits to retained top performers, escalated in parallel.

Property management rent rolls have emerged as the clearest institutional hedge against this volatility. Well-capitalised agencies are actively acquiring the rent roll portfolios of exiting or distressed competitors specifically to capture the recurring, annuity-style income that sales commission cannot currently guarantee — a defensive consolidation strategy that further concentrates market share among the operators already best positioned to absorb the AML/CTF compliance burden. The mortgage broking channel shows the same concentration in a different form: 72 per cent of top-performing brokers’ new business now comes from existing client networks rather than new acquisition, and a persistent 15 per cent inactive broker cohort — down from a 22 per cent peak in the depths of the 2022–23 tightening cycle, but still structurally elevated — signals that further attrition is likely even before the next sub-aggregator consolidation event occurs. Across every profession this Series examined, the institutional tier is not merely surviving the compression — it is positioned to consolidate a disproportionate share of a shrinking pool at the direct expense of the retail tier.

The Cascade Has Momentum

None of the mechanisms driving this compression are one-off interventions. Each sits within a broader regulatory trajectory that the parallel AUS-156 Series has independently documented as a coordinated architecture, not a single reform in isolation. The February 2026 DTI caps are themselves widely understood within the sector as a prototype rather than a final settling point — the same quantity-based rationing logic that APRA has signalled it would extend further, through investor-focused lending limits, should the current settings prove insufficient to moderate speculative secondary market activity. The FBAA and CoreData continue to lobby for a reduction in the serviceability buffer; APRA’s decision to hold it at 3.00 percentage points through its July 2025 review, against that pressure, is itself a signal that the current settings are considered durable rather than transitional.

On the compliance side, Tranche 2 AML/CTF is a phased implementation, not a single event — enrolment, program build-out, and enforcement activity will extend through 2026 and into 2027, with ASIC’s enforcement posture already demonstrating a willingness to cancel licences and impose material penalties on non-compliant operators. The insurance market’s PropSec-engineered premium plateau remains, on the Series’ own analysis, a fragile equilibrium rather than a resolved structural condition. What the AUS-156 Series established at the level of the asset class — that the sovereign has shifted from protecting nominal property values to managing systemic entry and exit capacity — is now visibly reshaping who is permitted to operate the professional infrastructure around that asset class, not merely who is permitted to buy into it.

What This Demands

The APN 22000 Series does not issue recommendations. What it offers is a forward assessment of the operating environment, derived from the weight of the evidence assembled across four independent research streams.

That evidence describes a professional services layer that has been operating on human capital assumptions inherited from a credit environment the sovereign has deliberately and durably closed off. Institutions that plan around historical headcount, historical commission structures, or historical conversion rates are extrapolating from a hyper-liquid period that will not return on the next rate cut, because it was never primarily a function of the rate cycle. The professionals and firms that survive this transition will not be the ones who transacted the most in 2021. They will be the ones whose businesses were structurally built to operate at 3.32 transactions a year, at 76 per cent loan conversion, at 149 settlements per valuer, and at a compliance cost structure that assumes AUSTRAC reporting obligations as a fixed input rather than an existential threat.

That is the operating environment the AUS-157 Series describes: not a professional services sector that has simply become smaller, but one whose institutional layer is being permanently recalibrated — through insolvency, regulatory enforcement, and accreditation-driven stratification — to the actual, mathematically constrained scale of the transactions it now serves. The transition is not complete. On the weight of the evidence, it is already well underway.

Findings are presented on the basis of data and evidence alone.