APN ANALYSIS: A-251014-AUS79

Executive Summary

The 2022 acquisition of Console by Reapit, backed by private equity firm Accel-KKR, has been validated as the pivotal event that consolidated the Australian PropTech market. Three years on, the strategic concerns of “platformisation” and market dominance have been fully realised. The combined entity has successfully locked in its majority market share, creating a “super-platform” or “operating system” for the industry.

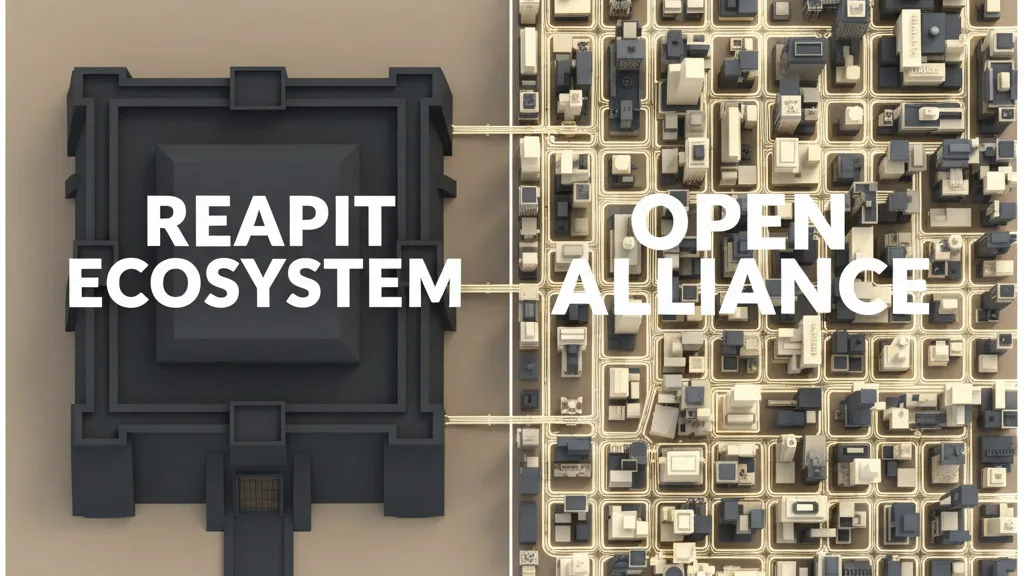

The primary effects felt by the market have been twofold: 1) significant, widespread price increases across the newly consolidated product suite, and 2) the emergence of a “challenger alliance” of independent PropTechs marketing themselves on “openness” and “fair pricing.” For agency principals, the 2022 acquisition has drawn a clear line in the sand, forcing a long-term strategic choice between the walled garden of the dominant ecosystem and the federated, open model of its competitors.

Background & Strategic Context

The 2022 acquisition was a market-defining event that created the dominant player in the industry. The long-term effects, viewed three years later, confirm the original strategic theses.

- The Power Play (Project Atlas): The private equity-backed power play was a complete success. By acquiring Console, Reapit and its backer Accel-KKR successfully captured a dominant market share (over 50%). As predicted, they have now moved to the “value extraction” phase of the private equity playbook, implementing significant, above-inflation price hikes across their captured user base in 2024 and 2025.

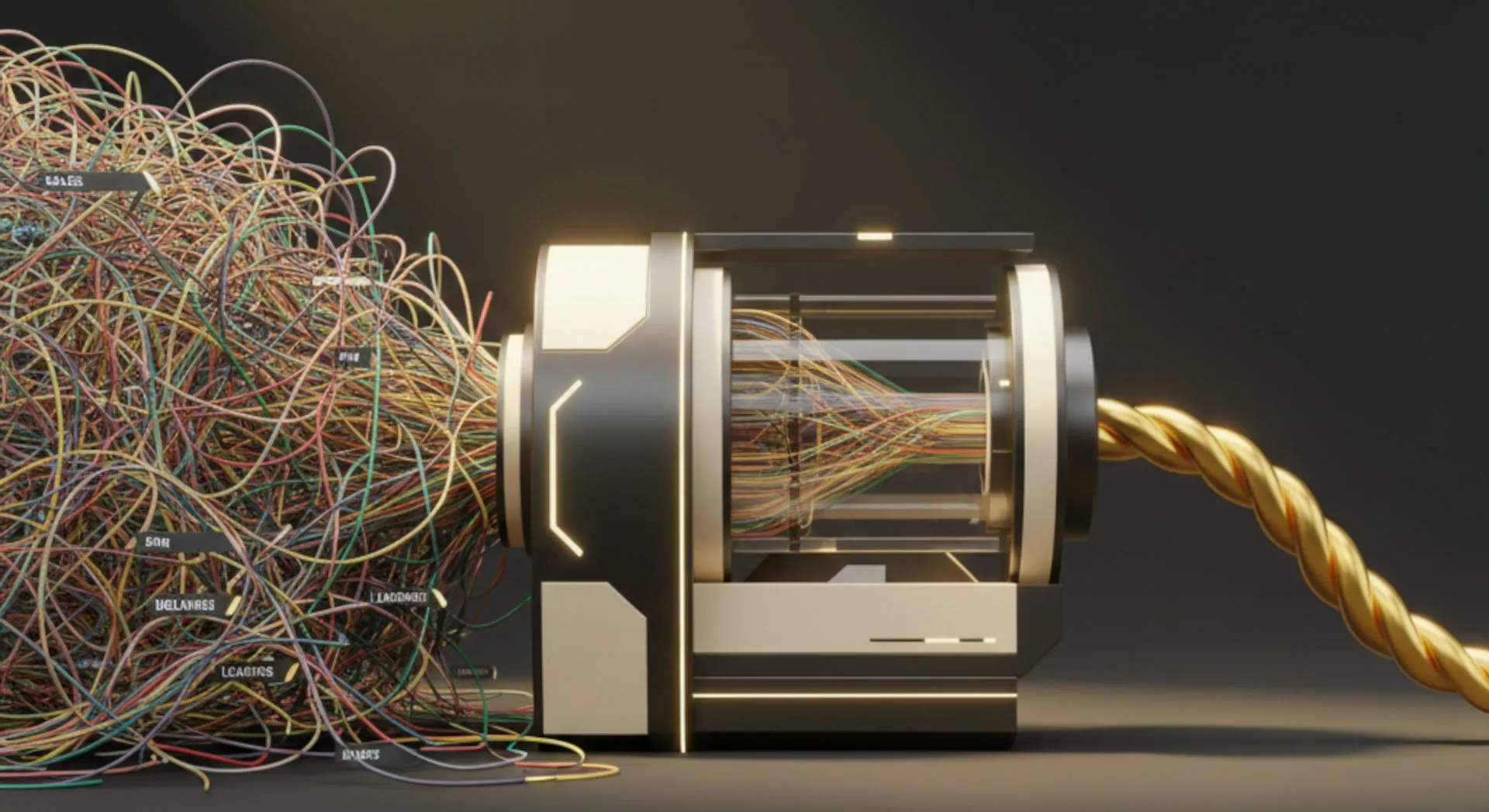

- The End of Data Silos (Tech Disruption): The core value proposition of the merger, ending data silos, has been the central focus of Reapit’s development. The integration of Agentbox (CRM) and Console (PM) has been technically complex, but it has resulted in the “Golden Profile” (which we have analysed previously), a feature designed to create a single client view and, more strategically, to create an integrated data moat that makes the ecosystem incredibly “sticky” and difficult for agencies to leave.

Deconstruction of the Acquisition’s 3-Year Impact (2022-2025)

The 2022 acquisition was not just a merger; it was the catalyst for a fundamental reshaping of the market. The key, observable effects are:

- Systemic Price Hikes: After a period of integration, Reapit began a series of significant price increases, with widespread industry reports of 20-30% hikes in 2024 and 2025. This confirms the hypothesis that acquiring market share was the prelude to aggressive financial extraction by its private equity owners.

- Consolidation of the Core Stack: The merger has successfully tied the two key pillars of an agency (sales and property management) into a single vendor. This has simplified the tech stack for many, but at the cost of eliminating choice and competition.

- The “Golden Profile” Data Moat: Reapit’s key post-acquisition innovation has been the “Golden Profile,” a tool that unifies data from its CRM and PM platforms. This feature is now the primary defence against churn, creating a powerful “vendor lock-in” by making an agency’s own data difficult to export in a unified way to a competing platform.

- Emergence of a “Challenger Alliance”: The acquisition’s aggressive nature created a market vacuum that smaller, independent PropTechs have rushed to fill. A “challenger ecosystem” of independent CRMs and PM platforms has emerged, building open APIs and marketing themselves as the “open” and “fair” alternative to the Reapit “walled garden.”

Critical Analysis & Balanced View

Looking back, the 2022 acquisition was less of a technology play and more of a classic private equity-driven market consolidation. The primary goal was not to build a better product, but to buy a dominant market position and leverage it for pricing power. This strategy has been executed almost perfectly. The “franken-platform” risk (the fear that the products would be poorly integrated) was a secondary concern for the acquirer; the primary goal was to control the user base.

The promised efficiencies of a unified platform are real, but they have come at a significant cost to the industry. The market is now less innovative and more expensive than it was in 2022. The 50% of the market outside the Reapit ecosystem is now defined by its opposition to it, and this has become the new central dynamic of the ANZ PropTech sector.

Balanced View: The 2022 Reapit-Console acquisition was a profound financial and strategic success for its owners. It created the “super-platform” that was intended and has successfully extracted significant value. For the property industry, it has been a clarifying event, demonstrating the high price of vendor lock-in. It has forced a new maturity on the market, where an agency’s choice of core software is no longer a simple operational decision but a long-term, defining strategic commitment to either a closed, dominant ecosystem or an open, federated alliance.

Strategic Implications for Property Professionals (Updated for 2025)

- For Agency Principals: The long-term cost of your 2022-2025 tech decision is now clear. If you are inside the Reapit ecosystem, your operational efficiency is high, but you have limited-to-no leverage on pricing. If you are outside, you must actively manage a “best-of-breed” stack of allied competitors.

- For PropTech Competitors: The “challenger alliance” is the only viable strategy. You must compete on “openness,” “fair pricing,” and seamless integration with other independents. Your primary marketing message is “freedom of choice” and “own your data.”

- For PropTech Investors: The opportunity to fund a single “point solution” is over. The next major opportunities lie in funding the “challenger alliance” to create a credible, integrated, and open alternative to the Reapit super-platform.

- For All Professionals: The 2022 acquisition proved that an agency’s data is its most valuable asset. The battle for the next five years will be over who ultimately controls that data: the agency or the platform they rent.