Structural Margin Contraction: Agency Margins Contract as Vendor-Paid Advertising Becomes a Fixed Transaction Cost

APN ANALYSIS: A-260109-AUS134168

Executive Summary

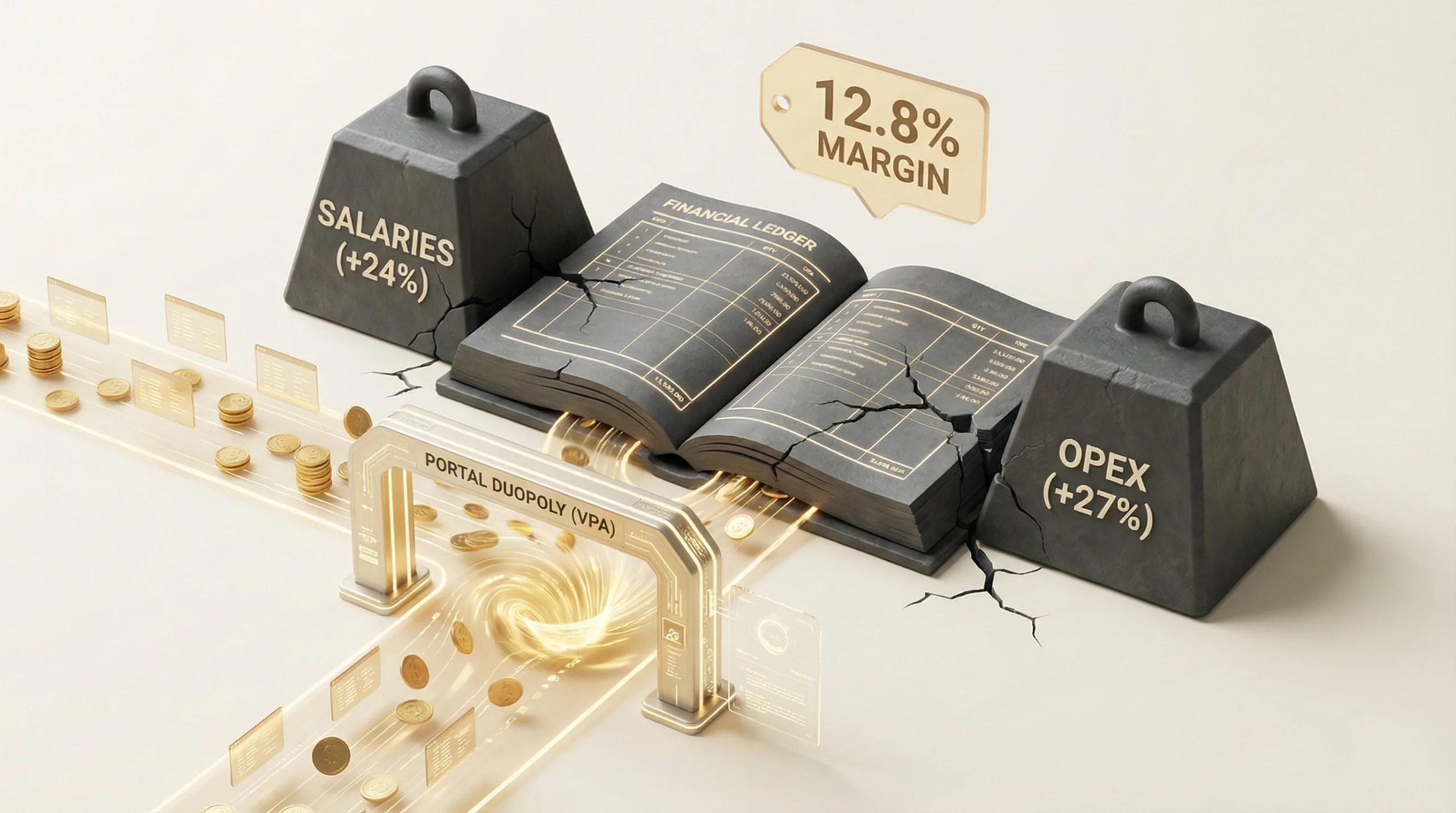

The Australian real estate agency model is undergoing a structural financial shift, defined by a material margin contraction and the universal adoption of Vendor-Paid Advertising (VPA). While asset values have provided a revenue buffer, rising operational costs (up 27% YoY) and salary pressures (up 24% YoY) are contracting agency profit margins from 13.3% to 12.8%. This internal pressure, combined with commission rate compression in competitive metropolitan markets, has solidified VPA not as a value-add, but as a substantial, non-negotiable transaction cost passed directly to the vendor, primarily to fund listings on the REA/Domain duopoly.

For property professionals, this environment demands a fundamental reorientation in value proposition. With marketing costs now a fixed, vendor-funded expense, an agent’s ability to justify their commission hinges on strategic advice, quantifiably improved negotiation outcomes, and the structural alignment of incentives. For vendors and asset managers, the focus must shift from negotiating the headline commission rate in isolation to scrutinising the total cost of sale, demanding transparency on marketing budgets, and deploying performance-based fee structures to ensure agent incentives are directly tied to maximising the final sale price.

Background & Strategic Context

This analysis of agency cost structures validates and calibrates APN’s core theses on how market boundaries are set and how value is captured within them. The interplay between deregulated fee environments and the rise of digital monopolies provides a clear case study of market evolution under specific policy and commercial pressures.

The Regulatory Architecture (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The report confirms that state-level deregulation, most notably the removal of commission caps in jurisdictions like Queensland, is the foundational policy action that created the current fragmented and hyper-competitive fee landscape. This regulatory withdrawal has allowed market forces—agent density, asset value, and geography—to become the primary determinants of commission rates, leading directly to the observed divergence between metropolitan and regional pricing.

The Digital Tollgate: The analysis provides clear evidence for the ‘Portal Wars’ sub-project, framing the REA/Domain duopoly as a structural tollgate on property transactions. Their pricing power has effectively transformed marketing from a discretionary agency service into a mandatory, vendor-funded infrastructure cost. This symbiotic relationship, where agents act as resellers for portal advertising, is a structurally significant dynamic shaping the total cost of sale for vendors.

The Incentive Misalignment (APN Professional Sentiment Index™ 24300): The margin contraction on agencies directly amplifies the classic ‘principal-agent problem’. Under a flat-fee model, the diminishing financial return for securing a premium price incentivises agents to prioritise transaction velocity over price maximisation. This report’s focus on tiered or ‘kicker’ fee structures is a direct market response to this misalignment, attempting to recalibrate agent behaviour to better serve vendor outcomes.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the ‘Strategic Benchmarking of Australian Real Estate Agency Fees and Marketing Expenditures: A 2024-2026 Industry Report’. The key facts are:

- Agency Margin Contraction: Agency profit margins have tightened from 13.3% to 12.8%, driven by a 27% year-on-year increase in the agency cost base and a 24% rise in staff salaries.

- Commission Rate Divergence: National average residential commissions sit between 2.0% and 2.5%. However, high-competition metro markets like Sydney see rates fall to 1.6%-1.9% for premium assets, while regional and low-liquidity markets command rates of 2.5% to over 3.5%.

- VPA as a Fixed Cost: Vendor-Paid Advertising (VPA) is now a structurally embedded transaction cost. A standard metropolitan marketing campaign budget now ranges from $4,500 to $9,800, with the bulk allocated to ‘Premiere’ or ‘Platinum’ listings on REA and Domain.

- Performance-Based Structures: Tiered or ‘kicker’ commission models (e.g., a base rate plus a higher percentage on value achieved above a threshold) are identified as a key strategic tool to align agent incentives with vendor interests, directly countering the economic rationale of a quick sale under a flat-fee model.

- Sector-Specific Benchmarks: Commercial sales commissions show an inverse relationship with asset value (2-4% for sub-$5M assets vs. 0.5-1.5% for institutional grade). Commercial leasing fees are benchmarked at 10-15% of first-year gross rent. Rural commissions are higher (2.5-4.0%) and require significant print marketing budgets (e.g., ~$7,836 for a full-page ad in The Land).

Critical Analysis & Balanced View

The core structural tension emerging from this analysis is that while digital technology has democratised property *visibility*, it has simultaneously concentrated pricing power, leading to an inflation of transaction costs for the vendor. The REA/Domain duopoly has become positioned as essential infrastructure, shifting the financial risk of marketing entirely from the agency to the seller through the VPA model. This is not merely a cost but a structural change in the financial mechanics of a property sale.

The margin contraction on agencies is a catalyst, not just a condition. It accelerates the adoption of the VPA model as agencies find it commercially unviable to carry marketing costs. Furthermore, it drives agencies towards ancillary revenue streams, such as ‘Pay Later’ marketing finance products. While these services improve vendor cash flow, they can obscure the true cost of a campaign and introduce a new layer of financialisation and potential conflicts of interest that require careful scrutiny by vendors.

Finally, the report highlights a growing bifurcation in the required skillset of a real estate professional. In high-volume, homogenous metro markets, the agent’s role is increasingly that of a marketing project manager, executing a formulaic digital campaign. Conversely, in commercial, rural, and unique residential sales, the traditional skills of network leverage, complex negotiation, and strategic problem-solving remain paramount and are the primary justification for the commission fee.

Strategic Implications for Property Professionals

- For Agents & Agency Principals: Justifying fees based on marketing reach is no longer a sufficient strategy. Your value proposition must be anchored in negotiation strategy, process management, and demonstrable alignment with the vendor’s financial success. Proactively introduce tiered commission structures as a point of differentiation. Operationally, you must systematically pursue efficiencies to protect margins, leveraging technology to automate low-value tasks, not just to bill vendors for them.

- For Vendors & Asset Managers: The negotiation framework must expand beyond the commission percentage to the ‘total cost of sale’. Demand an unbundled marketing schedule and query whether agency-negotiated portal discounts are being passed on. Make tiered ‘kicker’ commissions your default proposal to incentivise outperformance, ensuring the incentive threshold is set at a realistic, yet ambitious, market value.

- For Commercial Landlords & Investors: Fee structures are a direct lever on your Net Operating Income. For leasing, mandate that fees are calculated on the Net Effective Rent (post-incentives) to ensure agents are financially disincentivised from offering excessive incentives. For property management, demand a granular schedule of ‘included’ versus ‘extra’ charges to prevent fee erosion from ancillary costs like lease renewals or tribunal attendance.

- For Buyers’ Agents: This market structure enhances your strategic value. Your ability to deconstruct the total cost of sale and understand the selling agent’s incentive structure provides a material negotiation advantage. Use insights into commission models and VPA pressures to accurately assess an agent’s motivation and a vendor’s price flexibility, delivering quantifiably improved outcomes for your client.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides empirical validation for the APN Sovereign Policy Composite Index™ (SPCI, 24800), showing how government deregulation of fees created the conditions for the current market structure. It also validates the core thesis of the ‘Portal Wars’ sub-project, confirming the duopoly’s role as a private, price-setting utility in the property ecosystem.

- Index Calibration (APN Professional Sentiment Index™ 24300): The index is calibrated to reflect the margin contraction as a negative pressure on agency profitability and business confidence. However, it will now also track the adoption rate of tiered commissions and marketing finance products as positive indicators of strategic adaptation and revenue diversification within the sector.

- Data Capture (APN Symbiotic Intelligence Network™ 24310): This analysis triggers a new data capture mandate to monitor and benchmark the ‘total cost of sale’ as a percentage of asset value, segmenting by geography and asset class. This includes tracking the ratio of commission-to-marketing spend and the prevalence of different commission structures (flat vs. tiered) in agency agreements.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.