Sentiment Divergence and Narrative Contradiction Following the December 2025 CPI Release

The release of the December 2025 Consumer Price Index (CPI) data by the Australian Bureau of Statistics (ABS) on January 28, 2026, represents a transformative moment in the Australian macroeconomic discourse. After a period in late 2025 characterised by a fragile “disinflation” narrative, the latest data revealed a sharp acceleration in price pressures, with headline inflation climbing to 3.8% annually, up from 3.4% in November.1 This statistical pivot effectively scuppered prevailing market hopes for a “Christmas rate cut” and shifted the collective focus toward a potential interest rate hike by the Reserve Bank of Australia (RBA) in early 2026.3 The reaction across the media landscape was not uniform; rather, it exposed a profound “Sentiment Divergence” between institutional incumbents, public sector reporters, and independent realist analysts. This audit performs a forensic examination of these reactions, mapping the rhetorical strategies used to frame the return of “sticky” inflation.

The Statistical Foundation: Deciphering the December 2025 ABS Release

The December 2025 CPI data was released at 11:30 am AEDT on Wednesday, January 28, 2026, marking the first time the “complete” monthly CPI series became Australia’s primary gauge of headline inflation.2 The data revealed that the All Groups CPI rose 3.8% in the 12 months to December 2025, significantly exceeding the market consensus of 3.6%.6 This acceleration was driven by structural costs in housing, energy, and the service sector, presenting a significant challenge to the RBA’s mandate to maintain inflation within the 2-3% target band.2

Core Inflation and the Trimmed Mean Methodology

While headline figures capture public attention, the RBA’s preferred measure, the trimmed mean, provided the most critical policy signal. Trimmed mean inflation, which calculates price changes by “trimming” away the most volatile 30% of items (the top 15% and bottom 15% of price changes), rose to 3.3% annually in December, up from 3.2% in November.2 On a quarterly basis, the trimmed mean gained 0.9% in the December quarter, exceeding the RBA’s own forecast of approximately 0.75% published in the November Statement on Monetary Policy.10

The relationship between headline inflation CPIheadline and the trimmed mean CPItrimmed is essential for understanding the underlying momentum. In the December release, the trimmed mean demonstrated that inflationary pressures were no longer transient but were firmly embedded in the “sticky” service sectors. This persistence can be modelled by examining the weighted contribution of various expenditure classes:

$$CPI_{Total} = \sum_{i=1}^{n} w_i \left( \frac{P_{i,t}}{P_{i,t-1}} \right)$$

Where wi represents the weight of the category and P represents the price index. For the December 2025 period, the weights for Housing (23%) and Food (17%) played the most dominant roles in the upward movement.6

Primary Drivers of the December Acceleration

The 3.8% headline figure was primarily influenced by a combination of government subsidy roll-offs and structural demand in the housing and services sectors. The largest contributor was Housing, which rose 5.5% annually, driven by a combination of new dwelling costs and persistent rental inflation.2

| Category | Annual Change (%) | Quarterly Change (%) | Key Narrative Drivers |

| All Groups CPI | 3.8% | 0.6% | Energy subsidies ending, holiday travel spikes 2 |

| Trimmed Mean (Core) | 3.3% | 0.9% | Embedded service inflation, “sticky” prices 7 |

| Housing | 5.5% | N/A | Rents (+3.9%) and new building costs 2 |

| Electricity | 21.5% | N/A | Expiry of QLD/WA state government rebates 2 |

| Services | 4.1% | N/A | Domestic holiday travel (+9.6%), insurance 2 |

| Food & Beverages | 3.4% | N/A | Supermarket price persistence 1 |

The electricity sector witnessed a staggering 21.5% annual increase, a direct result of households in Queensland and Western Australia utilising the last of their state-based energy rebates.1 Without the impact of these temporary rebates, electricity prices would have risen by a more modest 4.6%.2 This created a “base effect” that complicates the narrative of genuine disinflation.

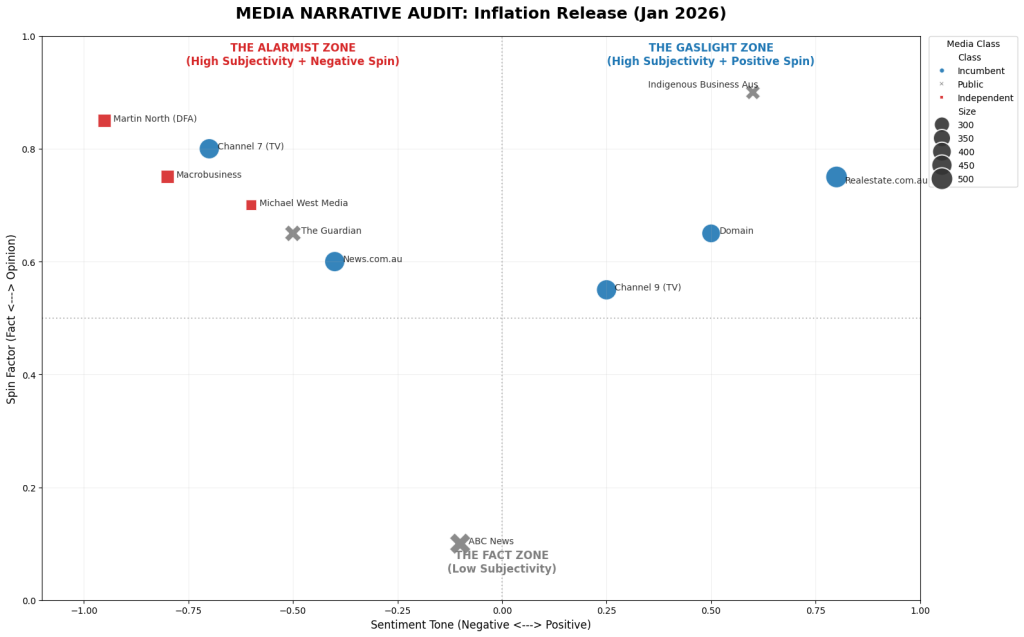

The Narrative Audit: Mapping Sentiment Across the Landscape

The following structured list identifies the primary headlines and lead paragraphs extracted from the 24-hour window following the release. This list reflects the mandatory format for forensic narrative analysis.

Sector Analysis: The Incumbents (Wealth Protection)

The “Incumbent” media sector, which includes the Australian Financial Review (AFR), The Australian, and News.com.au, prioritised institutional stability and the protection of financial capital. Their framing of the 3.8% inflation result was characterised by a sense of urgency regarding RBA policy and a focus on the “shock” to professional forecasts.

The Australian Financial Review: The Policy-Peer Perspective

The AFR’s response was defined by its focus on the failure of inflation to meet RBA and market expectations. Their headline, “Inflation overshoot signals a likely rate hike next week,” immediately positioned the data as a catalyst for central bank action.12 The lead paragraph emphasised that inflation now joins employment in signalling an economy that is “running hotter” than policymakers expected, making a rate hike “highly likely”.12

The AFR narrative relied heavily on the expert testimony of Besa Deda, Chief Economist at William Buck, who articulated the “Toothpaste Effect”: the idea that once service inflation is released into the economy, it is notoriously difficult to “get back in the tube”.12 This framing serves a professional audience concerned with terminal interest rate projections and the duration of the current tightening cycle. The outlet was meticulous in detailing the trimmed mean’s quarterly gain of 0.9%, describing it as a “tad slower” than the previous 1.0% gain but still “strong” enough to justify a revision of the 2026 outlook from one hike to two.12

News.com.au and The Australian: The Populist Alarm

While the AFR spoke to the boardroom, News.com.au and The Australian adopted a tone of populist alarm, focusing on the “pain” for the average household. News.com.au‘s lead paragraph focused on the “fresh repayment pain” for mortgage holders and described the result as a “kick in the guts” for stretched borrowers and tenants.13 This narrative frames inflation not just as a statistical overshoot but as an active adversary to the Australian way of life.

The Australian focused on the “unwelcome but unsurprising” nature of the data, quoting Treasurer Jim Chalmers but highlighting that the figures “exceeded economists’ expectations”.15 This dual-framing allows the outlet to maintain its role as a recorder of official government responses while simultaneously signalling to its readers that the current economic management is failing to contain the “inflation dragon”.17

The Sydney Morning Herald: The Structural Deficit Narrative

The Sydney Morning Herald (SMH) approached the data through a lens of long-term structural weakness. While covering the immediate CPI release, the SMH frequently integrated the result into a broader critique of the budget deficit and “anaemic productivity growth”.18 Their lead paragraphs often linked the rising cost of living to “warnings mount[ing] over [the] size of [the] budget deficit,” suggesting that the inflation crisis is a symptom of a deeper fiscal mismanagement that will leave the budget in structural deficit for “decades”.19

Sector Analysis: The Public Sector (Safe/Neutral)

Public sector outlets, primarily ABC News and The Guardian Australia, maintained a stance of data-driven neutrality, though The Guardian was notably more vocal about the social implications of the “bill shock” for renters and low-income households.

ABC News: The Chronological Record

The ABC served as the primary repository for the technical details of the ABS release. Their lead paragraphs focused on the objective facts: “CPI rose 3.8 per cent in the 12 months to December 2025” and “economists were expecting CPI growth of 0.7 per cent for the December quarter”.2 The ABC‘s reporting was instrumental in clarifying the “re-referencing” of the quarterly CPI data, explaining to the public how the new monthly series would align with historical quarterly benchmarks.9

By quoting ABS head of prices statistics Michelle Marquardt directly, the ABC ensured that the nuances of housing and food price contributions were placed on the public record without the hyperbole found in corporate media.2 However, even the ABC could not ignore the policy implications, reporting that the data would “determine if the Reserve Bank of Australia (RBA) raises interest rates”.15

The Guardian Australia: The Social Impact Frame

The Guardian’s narrative was centred on the “rapidly rising consumer prices” and the fight of Australian households to bring inflation under control.14 Their headline, “Expectations grow for interest rate hike next week after Australia’s inflation jumps to 3.8%,” positioned the hike as an “insurance” measure by the RBA.14

The lead paragraph emphasised that the battle against inflation would “start with a rate hike, the first since November 2023”.14 The Guardian’s reporting was unique in its focus on regional disparities, noting that inflation ran the “hottest in Brisbane, at 5.2%,” and Perth, at 4.4%, due to the roll-off of energy subsidies.14 This geographic lens provided a “Realist” edge to their otherwise “Public” category categorisation.

Sector Analysis: The Realists/Independents (The Signal)

The “Independent” sector, comprising Macrobusiness, Digital Finance Analytics (DFA), Michael West Media, and Tarric Brooker, provided the most aggressive forensic analysis. These outlets rejected the “resilience” narrative of the government and the “stability” narrative of the property portals, focusing instead on systemic risk and the erosion of household solvency.

Digital Finance Analytics (Martin North): The Armageddon Frame

Martin North of DFA provided the most striking divergence from mainstream reporting. His narrative centres on “Mortgage and Rental Stress,” using proprietary data to argue that the “spin” of the mainstream media hides a “sorry picture”.21 His headlines, such as “12.3 Million Australian Households Are Living In Economic Armageddon,” suggest that the official CPI figures are a lagging indicator of a much deeper catastrophe.22

DFA’s lead paragraphs focus on the “loyalty tax” imposed by financial firms and the “price walking” of existing customers, which North argues is a hidden driver of inflation that the ABS fails to capture fully.23 This is the “Signal”, a focus on the underlying demand and the demographic lens that “most investors and policymakers ignore”.24

Macrobusiness: The Housing Monster Critique

Macrobusiness, led by Leith van Onselen (the “Unconventional Economist”), focused its forensic audit on the “Housing Monster”.25 Their narrative posits that the Australian economy is “quietly designed to support rising asset prices,” and that inflation is being “artificially manipulated” by government subsidies.24

Van Onselen’s lead paragraphs often highlight the “worst rental crisis in living memory,” noting that rents have soared by 44% over five years.26 Following the December release, Macrobusiness was quick to point out that the 0.9% quarterly trimmed mean was the “final nail in the coffin” for any hopes of a near-term rate cut.27 This outlet consistently links inflation to the “unvirtuous cycle” of bracket creep and stagnating real wages.28

Michael West Media: The “Jimflation” Narrative

Michael West Media (MWM) provided a forensic look at the political responsibility for the inflation spike. Their headline, “Row over government role fuelling inflation, rate rise,” directly challenged the Treasurer’s denial that public spending was contributing to the crisis.18

MWM’s lead paragraph noted that “poor productivity growth and persistently strong government spending will give the Reserve Bank no choice but to hike interest rates next week”.18 By quoting economists like HSBC’s Paul Bloxham, who argued that the economy is “running above its speed limit,” MWM provided a “Signal” that the inflation spike was not just a global phenomenon but a “homegrown” crisis, a term they dubbed “Jimflation”.18

The “Zag”: Contradictory Optimism and “Rate Cut” Framing

The audit revealed several “Zags”, outlets that ran headlines or narratives suggesting inflation was falling or rate cuts were imminent, even as the core numbers remained sticky.

- Domain: On the day of the 3.8% CPI release, Domain published the headline “RBA Rate Hold Expected – a Double-Edged Sword for the Housing Market”.30 While the headline acknowledged inflation was at 3.8%, the narrative focus was on “stability” and the idea that the “next move [is] an increase” only in the sense that it may “help to take some heat out of the rapid price growth”.30 This frames the lack of rate cuts as a neutral or stabilising force rather than a sign of worsening affordability.

- Forbes Advisor Australia: Even as the December data approached, Forbes continued to run a narrative that “Inflation continues to ease in Australia,” focusing on a June 2025 quarter figure of 2.1% to suggest that “headline inflation rising just 0.7%… increases the chances of a May interest rate cut”.31 This selective use of historical “lows” to project future “cuts” constitutes a significant “Zag” from the reality of the 3.8% December print.

- Indigenous Business Australia (IBA): In a January 2026 update, IBA’s Principal Economist noted that “inflation has tempered,” focusing on the fall to 3.4% in November as “welcome news,” even as they prepared for the January 28 reading.32 This framing downplayed the “stubborn” nature of the inflation that analysts were already warning about.

The “Signal”: Mention of Trimmed Mean and Service Inflation

The “Signal” outlets are those that explicitly identify the underlying drivers that the RBA considers “policy-relevant.”

- Westpac Economics: Chief Economist Luci Ellis was cited as noting that the 0.9% quarterly trimmed mean “flags a rate hike by the RBA at the February meeting”.10 Westpac’s “Signal” was the acknowledgement that the final print was “meaningfully stronger” than expected.10

- Sharecafe: This outlet explicitly mentioned that while headline inflation climbed to 3.8%, the “RBA faces pressure as inflation exceeds forecasts,” specifically identifying that “core inflation slowed but headline inflation rising more than anticipated” was a complex mix.33

- Investing.com: Their coverage highlighted that core inflation “remained well above the Reserve Bank of Australia’s annual target range” and that the data “gives the RBA even less impetus to cut interest rates”.7

- BDO Chief Economist Anders Magnusson: Quoted across multiple platforms (InDaily, Accounting Times), Magnusson provided a clear “Signal” that the result “reinforces the message… that underlying price pressures are proving more persistent than expected”.34

The “Gaslight”: Property Portals and “Good News” Framing

The “Gaslight” task was to identify if any property portals framed the inflation spike or high interest rates as “good news.”

- Domain: Dr Nicola Powell, Domain’s Chief of Research, framed the RBA’s “steady approach” as a “double-edged sword” that “gives buyers and sellers more certainty”.30 By focusing on “certainty” during a period of rising interest rate risk and 3.8% inflation, the portal effectively minimises the negative impact on borrower serviceability.

- Realestate.com.au (REA): REA’s economist Anne Flaherty noted that price pressures were “stickier than hoped,” but the outlet simultaneously ran headlines about a “nationwide surge” in house prices for 2026.36 Their narrative suggested that the “demand shock” caught forecasters off guard and that the housing shortage would continue to drive growth “despite interest rate uncertainty”.37

- KPMG via REA: This framing explicitly tells buyers that “tight conditions are likely to persist,” encouraging immediate entry into the market even as “uncertainty hangs over where interest rates are heading”.37

The RBA Policy Intersection: Bullock’s Challenge

The 3.8% inflation print puts immense pressure on RBA Governor Michele Bullock. According to the audit, Bullock had previously indicated that a 0.9% increase in underlying inflation would be a “material miss”.27 With the December quarter delivering exactly that 0.9% gain, the narrative across the “Incumbent” and “Independent” sectors is that the RBA is now “locked in” for a February 2026 hike.38

The RBA’s “Dual Mandate” requires a balance between price stability and full employment. However, with unemployment remaining low at 4.1%–4.2%, economists like Anders Magnusson argue the RBA has “ample room to act” because the risk of jeopardising full employment is diminished.12 This technical context is vital for understanding why the media “Signal” shifted so decisively toward a hike following the Wednesday release.

Comparative Sentiment Divergence: A Summary Matrix

To conclude the audit, the following matrix summarises the sentiment divergence between the three primary categories.

| Feature | Incumbent Narrative | Public Sector Narrative | Independent Narrative |

| Headline Tone | Institutional Alarm 12 | Data Neutrality 2 | Systemic Critique 21 |

| Primary Driver | RBA Policy Fail 15 | “Bill Shock” (Rebates) 14 | “Jimflation” / Debt 18 |

| Rate Outlook | Feb Hike (75%) 14 | “Expectations Grow” 14 | “Final Nail” / Hike 27 |

| Housing View | “Certainty” / Pain 30 | “Renters Swelter” 14 | “Monster” / Armageddon 25 |

Conclusion: The Fracture of the Australian Economic Reality

The forensic audit of the Australian media landscape’s reaction to the January 28, 2026, CPI release reveals a nation receiving three different versions of economic reality.

For the Incumbent audience, the 3.8% inflation print is a technical failure of policy that necessitates a corrective rate hike to protect the value of wealth. For the Public Sector audience, it is a statistical record of a difficult transition period, marked by the end of energy subsidies and “sticky” holiday travel costs. For the Independent audience, however, the data is proof of a “Jimflation” crisis, a homegrown economic disaster fueled by government spending and a “housing monster” that is “crushing households”.18

The most profound “Signal” identified is the shift from quarterly to monthly CPI as the primary gauge of inflation.3 This transition has allowed the ABS to detect the “spike” in electricity and services more rapidly, but it has also allowed property portals to “Zag” and “Gaslight” by focusing on historical quarterly lows to distract from current monthly highs.30 As the RBA prepares for its first board meeting of 2026, the media landscape remains deeply divided, reflecting a country where “rate anxiety” is creeping back in, and “economic armageddon” is no longer a fringe theory but a primary topic of forensic audit.22

Works cited

- Australian Inflation Rises to 3.8%, accessed January 2026, https://www.sharecafe.com.au/2026/01/28/australian-inflation-rises-to-3-8-per-cent/

- CPI rose 3.8% in the year to December 2025 – Australian Bureau of Statistics, accessed January 2026, https://www.abs.gov.au/media-centre/media-releases/cpi-rose-38-year-december-2025

- Australia’s annual inflation has climbed to 3.8%, eliminating hopes for a Christmas rate cut, accessed January 2026, https://www.mortgagechoice.com.au/news/australia-s-annual-inflation-has-climbed-to-38-eliminating-hopes-for-a-christmas-rate-cut/

- NSW mortgage stress hits alarming levels despite rate cuts – realestate.com.au, accessed January 2026, https://www.realestate.com.au/news/nsw-mortgage-stress-hits-alarming-levels-despite-rate-cuts/

- Australian Bureau of Statistics, accessed January 2026, https://www.abs.gov.au/

- Australia Inflation Rate – Trading Economics, accessed January 2026, https://tradingeconomics.com/australia/inflation-cpi

- Australia CPI up more than expected in Dec, core inflation edges higher, accessed January 2026, https://www.investing.com/news/economic-indicators/australia-cpi-up-more-than-expected-in-dec-core-inflation-edges-higher-4469045

- Australian Dollar Mixed as CPI Falls Short of Guaranteeing RBA Hike, accessed January 2026, https://www.forex.com/en-us/news-and-analysis/australian-dollar-mixed-as-cpi-falls-short-of-guaranteeing-rba-hike/

- Consumer Price Index, Australia, December 2025 – Australian Bureau of Statistics, accessed January 2026, https://www.abs.gov.au/statistics/economy/price-indexes-and-inflation/consumer-price-index-australia/latest-release

- December CPI: Core inflation holds its ground, accessed January 2026, https://www.westpaciq.com.au/economics/2026/01/cpi-monthly-fi-december-2025

- Australian dollar climbs to three-year high, than edges down, Inflation rises 0.6%; details inside, accessed January 2026, https://m.economictimes.com/news/international/australia/australian-dollar-climbs-to-three-year-high-than-edges-down-inflation-rises-0-6-details-inside/articleshow/127668109.cms

- Inflation overshoot signals a likely rate hike next week – William Buck Australia, accessed January 2026, https://williambuck.com/series/inflation-overshoot-signals-a-likely-rate-hike-next-week/

- RBA rate hike fears grow as hot inflation hits 3.8%, accessed January 2026, https://www.brokernews.com.au/news/breaking-news/rba-rate-hike-fears-grow-as-hot-inflation-hits-3-8-288815.aspx

- Expectations grow for interest rate hike next week after Australia’s …, accessed January 2026, https://www.theguardian.com/australia-news/2026/jan/28/inflation-rate-australia-cpi-rates-abs-data

- Australia’s inflation rises to 3.8 pct in December-Xinhua, accessed January 2026, http://www.xinhuanet.com/english/asiapacific/20260128/19f8a86037ca4d4c963e4fdae759779f/c.html

- New inflation figures | Treasury Ministers, accessed January 2026, https://ministers.treasury.gov.au/ministers/jim-chalmers-2022/media-releases/new-inflation-figures-0

- Budget update to reveal Australia’s fiscal fortunes – Michael West Media, accessed January 2026, https://michaelwest.com.au/budget-update-to-reveal-australias-fiscal-fortunes/

- Row over government role fuelling inflation, rate rise – Michael West, accessed January 2026, https://michaelwest.com.au/row-over-government-role-fuelling-inflation-rate-rise/

- Macroeconomics Advisory – Page 4, accessed January 2026, https://macroeconomics.com.au/author/macroeconomics-advisory/page/4/

- Australia’s inflation rises to 3.8 pct in December, accessed January 2026, https://english.news.cn/20260128/d829f5c6cfed4ea4b6d20ecde8042c7f/c.html

- Digital Finance Analytics (DFA) Blog, accessed January 2026, https://digitalfinanceanalytics.com/blog/feed/podcast/

- November 2025 – Digital Finance Analytics (DFA) Blog, accessed January 2026, https://digitalfinanceanalytics.com/blog/2025/11/

- Page 3 – “Intelligent Insight” – Digital Finance Analytics (DFA) Blog, accessed January 2026, https://digitalfinanceanalytics.com/blog/page/3/

- The Elephant In The Room Property Podcast | Inside Australian Real Estate – Captivate, accessed January 2026, https://feeds.captivate.fm/httpsomnyfmshowsthe/

- Podcast: Digital Finance Analytics (DFA) Blog, accessed January 2026, https://digitalfinanceanalytics.com/blog/series/digital-finance-analytics-dfa-blog/

- MacroBusiness – Australian Property Shares Dollar Economy, accessed January 2026, https://api.macrobusiness.com.au/

- No RBA rate cut – a Melbourne Cup Day sure bet – Australian Property Update, accessed January 2026, https://australianpropertyupdate.com.au/apu/no-rba-rate-cut-a-melbourne-cup-day-sure-bet

- Chapter 2 – Overview of economic conditions – Parliament of Australia, accessed January 2026, https://www.aph.gov.au/Parliamentary_Business/Committees/Senate/Cost_of_Living/costofliving/Report/Chapter_2_-_Overview_of_economic_conditions

- Treasurer Jim Chalmers denies Government has spending problem after Liberals identify $57 billion black hole | The Nightly, accessed January 2026, https://thenightly.com.au/politics/australia/treasurer-jim-chalmers-denies-government-has-spending-problem-after-liberals-identify-57-billion-black-hole-c-21449556

- RBA Rate Hold Expected – a Double-Edged Sword for the Housing Market – Domain, accessed January 2026, https://www.domain.com.au/group/media-releases/domain-rba-rate-hold-expected-a-double-edged-sword-for-the-housing-market/

- Australian Inflation Rate: Monthly CPI Inches Upwards – Forbes, accessed January 2026, https://www.forbes.com/advisor/au/personal-finance/inflation-rate-australia/

- Inflation moderates, hasn’t gone away. What you need to know to navigate 2026 – Indigenous Business Australia, accessed January 2026, https://iba.gov.au/2026/01/inflation-moderates-hasnt-gone-away-what-you-need-to-know-to-navigate-2026/

- Australian Inflation Edges Higher Than Expected – Sharecafe, accessed January 2026, https://www.sharecafe.com.au/2026/01/28/australian-inflation-edges-higher-than-expected/

- Hotter-than-expected December CPI tips odds towards Feb rate hike, accessed January 2026, https://www.accountingtimes.com.au/economy/hotter-than-expected-december-cpi-tips-odds-towards-feb-rate-hike

- Rate hike risk as inflation rises – News | InDaily, Inside South Australia, accessed January 2026, https://www.indailysa.com.au/news/just-in/2026/01/28/rate-hike-risk-as-inflation-rises

- Australian borrowers brace for RBA rate pain after high inflation numbers, accessed January 2026, https://www.realestate.com.au/news/australian-borrowers-rush-to-lock-in-fixed-rates-as-rate-anxiety-surges/

- Australian housing shortage pushes house prices higher in 2026 | KPMG – Realestate.com, accessed January 2026, https://www.realestate.com.au/news/australian-housing-shortage-pushes-house-prices-higher-in-2026-kpmg/

- RBA Rate Hike Locked In as CPI Hits 3.8% – Feb 2026, accessed January 2026, https://discoveryalert.com.au/central-banks-inflation-management-challenges-2026/