APN Professional Sentiment Index™ — National and Regional Analysis

24300 | 24310 | 24126 | 24120 | 24200

Observation Period: March–May 2026 | Federal Budget Event: 12 May 2026

Classification: Publication | Significance Rating: Elevated Systemic Significance

Research Preface

This institutional research publication constitutes a formal independence declaration, affirming that all findings, metric computations, and structural deductions established herein are derived exclusively from verified Tier-1 and near-Tier-1 institutional data. No commercial influence, algorithmic orientation, or unverified qualitative sentiment has been permitted to alter the foundational analysis. The integrity of the data architecture is preserved through an uncompromising reliance on certified institutional sources, ensuring that the resulting intelligence remains structurally insulated from cyclical market narratives.

The APN Codex framework operates as a dual-layered analytical architecture, designed to systematically quantify both empirical market realities and structural policy consequences. The 21000 Series serves as the objective data ingestion layer, capturing unadjusted institutional data from official endpoints to establish fixed mathematical baselines. The 24000 Series houses the proprietary APN indices, which function as analytical lenses to translate these empirical baseline deviations into quantifiable market frictions, regulatory vulnerabilities, and asymmetric capital constraints.

This publication applies the 24300 APN Professional Sentiment Index™ and its subordinate 24310 APN Symbiotic Intelligence Network™ to the Australian property market as of May 2026, at the point of convergence between a materially restrictive monetary policy environment and the 2026–27 Federal Budget. The analysis operates at two levels: a national assessment of the structural decoupling between professional optimism and consumer constraint, and a geographic decomposition across Queensland, New South Wales, and Victoria — extending to SA4 level where ABS data permits. Supporting nodes activated in this publication include the 24126 APN Acute Vulnerability Index™ at identified SA4 zones, the 24120 APN Sentinel™ for the Melbourne City SA4, and the 24200 APN Risk & Compliance Index™ at the state jurisdictional level.

Executive Synthesis

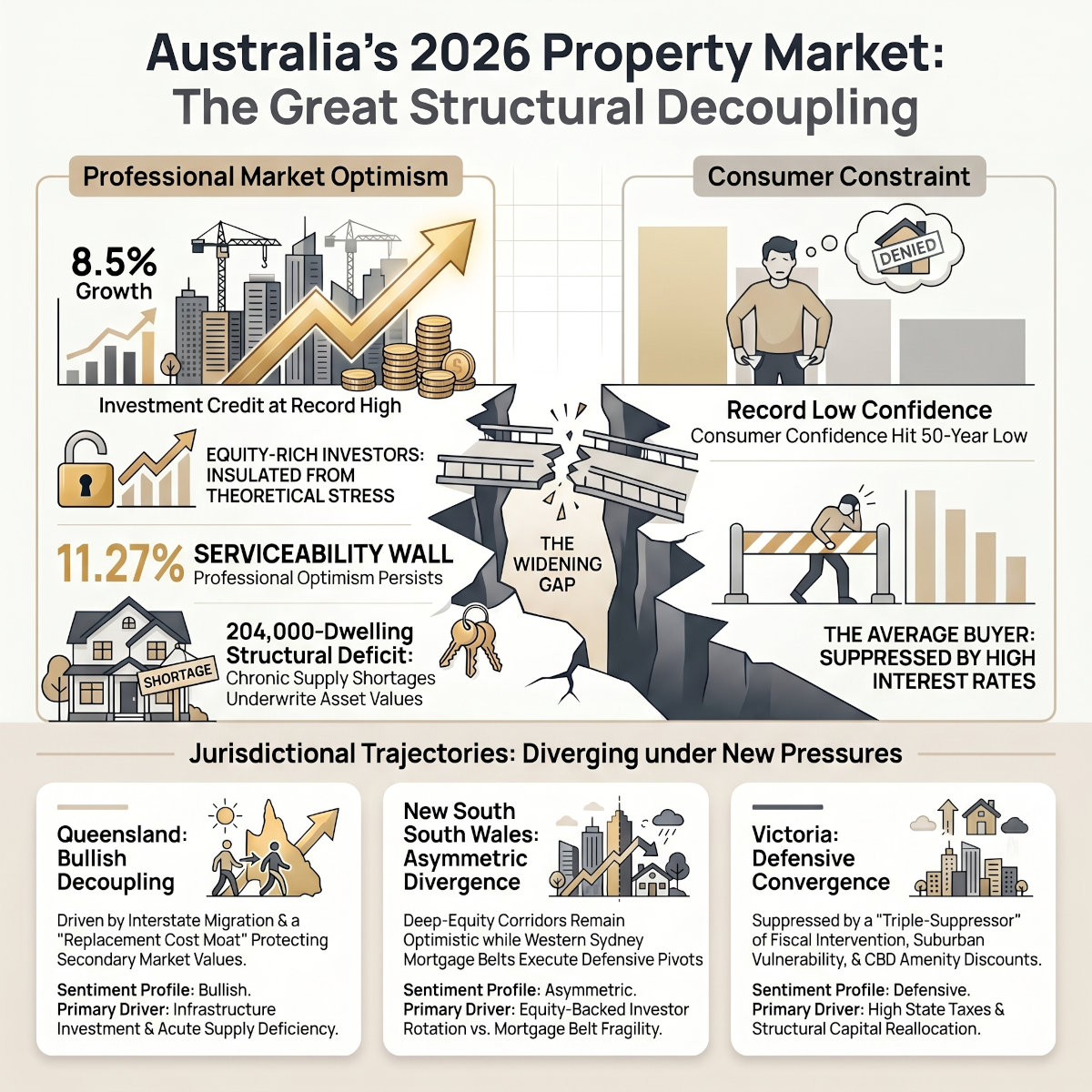

The fundamental condition recorded in the Australian property market as of May 2026 is one of structural decoupling. Investment housing credit is expanding at 8.5% year-on-year — the highest growth trajectory recorded in contemporary APRA data — while the ANZ-Roy Morgan Consumer Confidence Index has recorded its lowest reading since the index commenced in 1972, reaching 63.1 in the week of 24 March 2026, driven directly by the Reserve Bank of Australia’s decision to raise the Official Cash Rate to 4.10% on 17 March 2026. The OCR has since been raised a further 25 basis points to 4.35% on 5 May 2026, establishing a theoretical ADI stress rate of 11.27%.

Under prior analytical frameworks, this configuration would have been characterised as a divergence in animal spirits — bullish positioning among incumbent asset holders running counter to broadly pessimistic consumer sentiment. The APN Clinical Authority standard translates this phenomenon into a measurable structural decoupling coefficient: the gap between the behavioural positioning of property market professionals and the empirical consumer constraint data recorded across five active 21000 Series nodes. That gap is currently at a historically anomalous level, constituting a structural discontinuity rather than a cyclical variation.

The 2026–27 Federal Budget, delivered 12 May 2026, operates as a direct intervention into this decoupling environment. Confirmed measures — the restriction of negative gearing deductions to new-build properties only (with full grandfathering of existing assets), the transition of the Capital Gains Tax discount from the 50% flat model to pre-1999 inflation indexation, the launch of the Help to Buy shared equity scheme, and the reduction of MIT withholding tax on build-to-rent developments — have each generated distinct professional sentiment responses that vary materially across the three eastern seaboard jurisdictions.

When the national decoupling signal is decomposed geographically, three structurally distinct jurisdictional trajectories emerge. Queensland sustains a pronounced bullish decoupling, supported by demographic structural capacity, infrastructure investment, and a supply pipeline that is materially deficient relative to absorption demand. New South Wales exhibits an asymmetric decoupling: professional intermediaries servicing deep-equity investor cohorts maintain elevated optimism, while those operating in the western Sydney mortgage belt are executing defensive convergence with consumer pessimism. Victoria functions as the definitive structural outlier across the eastern seaboard, characterised by a triple-suppressor mechanism — elevated state fiscal intervention (24200), structural vulnerability convergence in outer-suburban SA4 zones (24126), and a crime perception amenity discount in the Melbourne City SA4 (24120) — producing a professional sentiment profile that is fundamentally defensive and increasingly oriented toward capital reallocation rather than accumulation.

The inter-state divergence recorded in this publication is not a behavioural anomaly. Each state’s professional sentiment profile reflects a rational integration of discrete structural fundamentals. The significance of the 24300 signal at this juncture lies not in the existence of divergence, but in its magnitude: the concurrent activation of monetary policy restriction, federal fiscal intervention, and state-level regulatory variation has produced a professional sentiment environment of elevated systemic consequence for capital allocation, housing delivery, and market access across the Australian residential asset base, valued in excess of $12 trillion.

Section 1 — Empirical Anchor

1.1 National Macroeconomic and Business Sentiment Baselines

The broader commercial environment establishes the foundational context for property sector professional sentiment. Institutional surveys indicate a material deterioration in business confidence across the broader economy, influenced by global supply chain volatility, energy pricing disruptions, and persistent domestic inflation.

The NAB Monthly Business Survey for March 2026 recorded business confidence at -29 index points — a 29-point contraction representing the most substantial negative shift since the 2020 economic disruptions. Over the broader first quarter of 2026, overall business confidence fell to -4 index points. However, dissecting the sector-specific data reveals a pronounced structural decoupling: the Finance, Property, and Business Services cohort maintained positive operating conditions, outperforming aggregate national averages. The NAB Commercial Property Index recorded +30 for the March quarter, indicating that specialised property practitioners maintain a defensible and elevated operational posture while the broader economy deteriorates.

The OECD composite business confidence indicator for Australia (BSCICP02AUQ460S, via FRED) registered a material downward trajectory entering the second quarter of 2026, corroborating the NAB findings and underscoring an environment where input cost escalation and monetary policy restriction are systematically compressing operating margins across the broader economy.

1.2 Labour Demand and Transacting Capacity

The ANZ-Indeed Australian Job Ads index recorded a 0.8% month-on-month contraction in April 2026, compounding a 3.1% contraction in March 2026. On a year-on-year basis, the index declined 1.4%. This reduction in labour demand velocity points to a managed economic deceleration, with unemployment forecast to drift toward a 4.5% terminal rate by the fourth quarter of 2026, applying sustained downward pressure on the 21230 Employment and GDP node.

1.3 Credit Velocity and Capital Allocation

The aggregate ADI residential loan book reached $2.46 trillion in March 2026 (APRA Monthly ADI Statistics). The critical professional sentiment metric is the composition of this expansion: investment housing credit recorded 8.5% year-on-year growth — the highest growth trajectory in contemporary APRA data — demonstrating that, despite the 4.35% OCR and the DTI cap of 20% for loans above 6x income, investor cohorts possessing established equity reserves are accelerating market participation rather than withdrawing from it.

ABS 5601.0 Lending Indicators for the December 2025 quarter confirm this trajectory. The total value of new loan commitments for dwellings rose 9.5%, reaching $108.3 billion. Within this aggregate, investor loan commitments rose 7.9% to $43.0 billion, while first home buyer values expanded 15.5% to $19.3 billion — the latter driven substantially by sovereign support mechanisms rather than independent borrowing capacity.

1.4 Construction and Development Pipeline

The Property Council of Australia Procore Industry Sentiment Survey for the March 2026 quarter documented a contraction in national confidence from 123 to 104 index points — a 19-point decline representing the most substantial quarterly deterioration since 2022, with housing capital growth expectations falling to their lowest level since 2020.

Master Builders Australia forecasts a 204,000-dwelling shortfall against the National Housing Accord’s 1.2 million home target by 2029. The cost of constructing a new detached dwelling has risen 48.6% above pre-2020 levels. Sixty-three per cent of surveyed builders remain bound by fixed-price contracts while absorbing these cost escalations, creating a structural pressure point that elevates insolvency risks across the sector and is directly reflected in the 21280 B2B Invoice Default Velocity node.

1.5 Intermediary and Service Provider Data

The MFAA Market Sentiment Survey (February 2026) documents the consumer constraint mechanism at the practitioner interface. Brokers report that 24.2% of their borrowers hold a negative view of their financial outlook — an increase of 5.3 percentage points from the prior observation. Ninety-seven per cent of brokers are actively engaged in restructuring client debt or negotiating rate discounts to mitigate account delinquency. This confirms the simultaneous operation of two distinct professional realities: elevated investor credit volumes and materially constrained owner-occupier serviceability, with practitioners managing both within the same operational environment.

1.6 State-Disaggregated Empirical Data

Queensland

ABS 5601.0 confirms a 6% expansion in first home buyer loan values in Queensland for the December 2025 quarter, against an 18.5% annual escalation in Greater Brisbane median house prices by March 2026 and a 1.8% rise in dwelling values in March 2026 alone. Building approvals rose 1.8% in January 2026 but remain structurally deficient at approximately 35,800 dwellings over the preceding twelve months against the National Housing Accord target of 49,000 to 50,000 dwellings per annum. Private dwelling apartment approvals recorded a 13.5% sustained contraction over the annual observation period.

SA4-level labour market data from the ABS Small Area Labour Markets publication identifies elevated unemployment in Logan-Beaudesert (5.6%), Ipswich (5.5%), and Moreton Bay North (5.3%) against the Queensland state average of 4.3%. Queensland Outback records 9.2%, indicating structural dislocation in resource-dependent regional economies. The Queensland Office of State Revenue projects property taxes to average $11.3 billion annually, contributing $45.2 billion over the four-year forward estimates period — stamp duty and land tax representing 56.0% of total state taxation revenue.

NIL RETURN — ABS 5601.0 Lending Indicators — SA4 granularity not available. NIL RETURN — ABS 8731.0 Building Approvals — SA4 granularity not available for the March 2026 observation period.

New South Wales

New South Wales is projecting overall lending growth of approximately 9% for 2026, driven by a 16% escalation in investor loan volumes (approximately 77,470 loans) against a marginal 4% expansion in owner-occupier loans. First home buyer loan values expanded 11% in the December 2025 quarter. The state captures 31% of all new investor loans nationally, confirming sustained capital asymmetry despite peak median asset values. Building approvals recorded a 1.9% increase early in the first quarter of 2026, though structural delivery friction and extended grid connection lead times continue to constrain the physical pipeline across major Western Sydney SA4 corridors.

The Central West SA4 recorded an unemployment rate of 7.6% against the state average of 4.3%. The Sydney Outer West and Blue Mountains SA4, and the Blacktown SA4, carry concentrated populations facing dual pressures from elevated debt-to-income ratios and labour market fragility. Consumer sentiment tracked the national trajectory through March 2026 before registering a marginal recovery in late April.

The abolition of the First Home Buyer Choice scheme in July 2023 reverted entry requirements to transfer duty with augmented exemption thresholds to $800,000, structurally reinstating the upfront capital barrier that had been partially removed.

NIL RETURN — ABS 5601.0 Lending Indicators — SA4 granularity not available. NIL RETURN — ABS 8731.0 Building Approvals — SA4 granularity not available for the March 2026 observation period.

Victoria

Victoria is projected to reach 166,345 total loans in 2026, but the composition reveals a material structural shift: while first home buyer loans expanded 4% in the December 2025 quarter, professional commentary confirms a sustained divestment trend among incumbent secondary-market investors managing exposure to state-based fiscal friction. Building approvals contracted 3.8% in early 2026, underperforming both Queensland and New South Wales. The Melton-Bacchus Marsh and Melbourne West SA4 area recorded 754 approvals over a five-year rolling metric — 20.2 per 1,000 people — failing to match demographic absorption velocity.

The Victorian state unemployment rate reached 4.8% in March 2026, above the national average of 4.3%. Central Goldfields LGA recorded 7.5%, indicating structural dislocation in specific regional zones. Victoria maintains the highest property tax revenue to Gross State Product ratio of the three jurisdictions. The Windfall Gains Tax, implemented in 2023, and augmented land tax thresholds have introduced material regulatory friction, suppressing project viability for development cohorts and generating a documented depletion of the established rental pool.

NIL RETURN — ABS 5601.0 Lending Indicators — SA4 granularity not available. NIL RETURN — ABS 8731.0 Building Approvals — SA4 granularity not available for the March 2026 observation period.

Section 2 — Baseline Context

2.1 National Historical Reference Anchors

Four historical cycles provide the calibration framework for assessing whether current professional sentiment represents normal cyclical variance or a structural discontinuity.

During the 2017–2018 APRA macroprudential epoch — the imposition of 10% investor credit growth caps and 30% limits on interest-only lending originations — professional sentiment in the investor advisory space contracted proportionally and synchronously with the regulatory constraint. Both consumer demand and professional optimism trended downward simultaneously. This represented a cyclically standard alignment.

The 2019–2020 Royal Commission implementation period delivered operational friction rather than structural decoupling. Professional sentiment dipped materially due to compliance bottlenecks and extended approval timelines, but fundamental consumer demand remained relatively stable. The two moved in parallel rather than diverging.

The 2022–2023 RBA rate tightening cycle — OCR rising from 0.10% to 4.35% — delivered a material shock to aggregate borrowing capacity, recording the Regulatory Borrowing Capacity Index at an epochal low of 0.6667 (Node 21350, Z-Score of -1.4085σ). During the initial phase, professional sentiment converged with consumer pessimism. However, decoupling commenced in late 2023 as structural supply deficits established a floor under asset values, preventing the price corrections that typically accompany monetary policy tightening of this magnitude.

The 2023 Stage 3 tax cut modification and 2024 pre-election housing policy environment produced a temporary sentiment normalisation, narrowing the decoupling coefficient before the March 2026 rate increases re-established the divergence at historically elevated levels.

2.2 The 2026 Structural Discontinuity

The May 2026 operating environment constitutes a definitive structural discontinuity against these historical anchors. In prior tightening cycles, an OCR sustained at 4.35% combined with record-low consumer sentiment would systematically suppress both retail consumer participation and professional property sentiment. The current data explicitly contradicts this historical pattern.

The 8.5% annual expansion in investment credit demonstrates that incumbent asset holders — utilising accrued equity rather than nominal wage growth — are driving acquisition velocity independently of the 11.27% ADI stress rate. Professional sentiment among brokers, buyers agents, and investment advisors is structurally elevated because their primary revenue-generating client base is insulated from serviceability constraints through existing capital reserves.

This configuration reflects the Asset-Wage Divergence construct: the condition where physical asset values escalate at a rate materially exceeding nominal wage growth, progressively severing the income-to-borrowing relationship for cohorts without established equity. It is not a cyclical phenomenon — it is a structural reset in which capital flows have decoupled from the macroeconomic constraints binding the median wage-earning consumer, and professional sentiment reflects that structural reality accurately.

2.3 Inter-State Structural Divergence — Historical Basis

The three eastern seaboard jurisdictions entered 2026 with materially different structural positions, established through divergent state-level policy pathways following the 2022–2023 tightening cycle.

Greater Brisbane recorded net interstate migration of 21,595 individuals and net overseas migration of 55,743 individuals in 2024–2025, colliding with a structurally deficient construction pipeline to produce acute physical scarcity. Queensland’s property tax architecture, despite generating $45.2 billion over the forward estimates, imposes relatively lower holding friction on non-resident and portfolio investors compared to Victoria, sustaining a bullish acquisition posture among interstate capital allocators. Regional centres — Rockhampton (19.2% annual growth), Townsville (26.5%), and Gladstone (23.8%) — demonstrate that the scarcity pricing dynamic extends well beyond the Greater Brisbane SA4 corridor into resource-adjacent economies.

New South Wales entered 2026 operating under the highest median price environment of the three states, mathematically guaranteeing that the 11.27% ADI stress rate enacts immediate cohort exclusion for median-wage earners. However, the projected 16% expansion in investor lending confirms that incumbent asset holders are actively rotating capital into the state’s property market. The repeal of the First Home Buyer Choice scheme structurally reinstated the transfer duty barrier, cementing the advantage of established capital over new market entrants and concentrating professional optimism in the equity-backed investor advisory segment.

Melbourne entered 2026 as the definitive structural outlier — the only major capital recording sustained price contraction, at -2.5% annualised as at the observation period. Victoria’s professional defensiveness is a rational response to the concurrent activation of three discrete structural suppressors that do not operate simultaneously in any other jurisdiction: state fiscal intervention, outer-suburban structural vulnerability, and a crime perception amenity discount in the metropolitan core.

Section 3 — Proprietary Index Pressure Point

3.1 National Decoupling Signal

The 24300 APN Professional Sentiment Index™ measures the structural decoupling coefficient — the gap between the operational optimism of the professional property ecosystem and the empirical deterioration of consumer capability. At the national level, that gap has reached a historically anomalous magnitude in May 2026.

The convergence of active deviations across nodes 21210 (Interest Rates), 21220 (Inflation), 21230 (Employment and GDP), 21260 (Construction Costs), and 21640 (Consumer Sentiment) applies direct downward pressure to the consumer side of the equation. Against this, the 8.5% investor credit expansion and the +30 NAB Commercial Property Index reading establish the professional optimism side. The resulting decoupling coefficient is not explained by forward-discounting of anticipated monetary policy relief — the ASX 30-Day Interbank Cash Rate Futures curve as at May 2026 implies a 17% probability of a further rate increase to 4.60% by June 2026, with no material rate reductions priced until the second half of 2027. The RBA’s May 2026 Statement on Monetary Policy noted that inflation risks remain skewed to the upside due to persistent services inflation and geopolitical energy pressures.

The structural supply deficit provides the empirical foundation for professional optimism. The National Housing Supply and Affordability Council 2026 report projects delivery of only 983,000 new dwellings against the National Housing Accord’s 1.2 million target — a 204,000-dwelling structural deficit that establishes an asymmetrical capital advantage for existing asset holders and provides practitioners with a legitimate, data-grounded basis for sustained optimism in the secondary market.

Budget measures have generated a specific anticipatory positioning signal within the 24300 index ahead of the 12 May delivery. The anticipated grandfathering of negative gearing provisions for existing assets is insulating approximately 1.28 million incumbent market participants from fiscal friction — establishing a structural policy advantage for established equity over prospective capital accumulation and sustaining the Asset-Wage Divergence construct. Simultaneously, the CGT discount transition is driving pre-emptive vendor activity, generating a short-term liquidity event as investors seek to crystallise gains under the current 50% flat discount framework before the indexation model takes effect.

3.2 State-Level Decoupling Matrix

Queensland — Bullish Decoupling

Professional sentiment in Queensland exhibits a sustained bullish decoupling, completely insulated from the consumer constraint recorded at the national level. This optimism is not confined to the Greater Brisbane SA4 zone but is distributed across the state, including resource-adjacent regional markets. Practitioners are explicitly framing the current environment as a counter-cyclical accumulation opportunity, leveraging the 8.5% national investor credit expansion and the structural supply deficit to execute equity-backed acquisition strategies for clients possessing deep capital reserves.

The Queensland market possesses a demonstrable Replacement Cost Moat: because it is currently financially unviable to deliver new stock at scale below existing secondary market values — driven by the 48.6% escalation in construction input costs — existing assets carry a structural valuation floor that sustains professional confidence in capital preservation regardless of the restrictive OCR environment.

New South Wales — Asymmetric Decoupling

New South Wales demonstrates an asymmetric decoupling that bifurcates sharply across geographic lines within the state. In high-amenity SA4 zones — Eastern Suburbs, Northern Beaches, Inner West — professional sentiment remains elevated, leveraging the 16% expansion in investor credit to execute equity-backed accumulation. Practitioners in these corridors are servicing client cohorts that are structurally insulated from the 11.27% ADI stress rate.

Conversely, professionals operating in the Western Sydney mortgage belt SA4 zones — Blacktown, Outer West and Blue Mountains, Parramatta — exhibit defensive convergence with consumer pessimism. In these corridors, the mathematical compression of borrowing capacity suppresses transactional velocity, forcing advisory professionals to pivot toward debt restructuring, delinquency mitigation, and distressed asset management. The Central Coast, Hunter Valley, and Illawarra SA4 zones function as the primary mortgage belt indicators, carrying high concentrations of owner-occupier households with elevated debt-to-income ratios facing refinancing pressure in the current rate environment.

Victoria — Defensive Convergence

Victorian professional sentiment displays defensive convergence, with the signal evolving toward a capitulation posture in specific market segments. Development professionals and property managers report material operational constraint attributable to the escalating state-based tax burden. The documented departure of a substantial number of established landlords — with over 10,000 rental properties removed from the private rental pool — structurally degrades professional optimism in the property management and investor advisory segments.

A nascent counter-cyclical positioning is emerging among specific buyers agents who view Melbourne’s sustained underperformance relative to Sydney and Brisbane as a long-term relative value arbitrage opportunity, contingent on a stabilisation of the legislative friction environment. This represents a minority professional signal within the broader defensive posture.

3.3 24126 APN Acute Vulnerability Index™ — Invocation Register

The 24126 APN Acute Vulnerability Index™ measures concentrated markers of localised socio-economic stress and housing insecurity at the SA4 level. Invocation requires the simultaneous convergence of three evidenced criteria: SA4 unemployment materially above the state average; sustained contraction or historically depressed levels in SA4 building approvals; and identified mortgage stress concentration from near-Tier-1 or labelled qualitative sources. All three criteria must be explicitly evidenced — invocation on the basis of partial data is not architecturally permissible.

The unavailability of SA4-level granularity in ABS 8731.0 Building Approvals for the March 2026 observation period has constrained formal invocation across the majority of candidate zones in all three states. The following register documents the outcome for each assessed zone.

Queensland Candidate Zones:

24126 — Insufficient data for invocation — Logan-Beaudesert: Unemployment elevated at 5.6% above the state average of 4.3%. Digital Finance Analytics data identifies extreme localised mortgage stress in specific postcodes within this SA4, with Tanah Merah and Daisy Hill operating at near-maximum theoretical stress exposure. NIL RETURN on SA4-specific ABS building approvals prevents full architectural invocation.

24126 — Insufficient data for invocation — Ipswich: Unemployment elevated at 5.5%. Mortgage stress documented. NIL RETURN on SA4 approvals.

24126 — Insufficient data for invocation — Moreton Bay North: Unemployment elevated at 5.3%. NIL RETURN on SA4 approvals.

24126 — Insufficient data for invocation — Cairns / Townsville: SA4 data incomplete across the required three concurrent matrices.

New South Wales Candidate Zones:

24126 — Insufficient data for invocation — Blacktown: Digital Finance Analytics mapping confirms postcodes within this SA4 operating at 100% mortgage stress concentration. Specific SA4 unemployment divergence and SA4-level approval contractions lack the granularity required for formal invocation.

24126 — Insufficient data for invocation — Sydney Outer West and Blue Mountains: Elevated labour market slack relative to inner-ring SA4 zones documented, but tri-nodal convergence data not available at the required granularity.

24126 — Insufficient data for invocation — Central Coast / Hunter Valley / Illawarra: Mortgage belt pressures active and documented, but specific data vectors remain unavailable at SA4 level.

Victoria:

24126 Invoked — Melbourne West — Victoria

Labour Market: Structural unemployment consistently elevated at 5.2%, materially above the Victorian state average of 4.8%.

Building Approvals: Sustained delivery constraint documented in adjacent corridors — Melton-Bacchus Marsh recording 754 approvals over a five-year rolling metric, equivalent to 20.2 per 1,000 people, failing to match demographic absorption velocity.

Mortgage Vulnerability: Digital Finance Analytics identifies specific local subsets within the Melbourne West SA4 operating at elevated theoretical mortgage stress exposure, representing a structural pressure point where new-build fixed-price contract failures intersect with the peak 2020–2021 lending cohort now approaching reset conditions.

All three invocation criteria are evidenced. 24126 formally invoked — Melbourne West — Victoria.

24126 — Insufficient data for invocation — Hume / Melton-Bacchus Marsh / Latrobe-Gippsland / Ballarat: SA4 data incomplete across the required three concurrent matrices at the current observation date.

3.4 24120 APN Sentinel™ — Victoria (Melbourne City SA4)

The 24120 APN Sentinel™ Safety and Sentiment Index operates on the premise that property markets price in the subjective perception of safety rather than objective crime frequency data. In the Victorian context, the visibility of crime — concentrated public order incidents in the Melbourne CBD, sustained media coverage of retail theft and antisocial behaviour, and the political salience of public safety throughout 2025–26 — is generating a measurable amenity discount in the Melbourne City SA4 independently of, and in addition to, the fiscal and structural suppressors documented above.

Invocation of 24120 requires three evidenced criteria: documented practitioner commentary linking safety perception to capital steering in the specific SA4; an observable amenity discount not otherwise explained by credit or fiscal factors; and documented media salience sufficient to establish that the perception dynamic has had broad public reach.

24120 Invoked — Melbourne City — Victoria

Practitioner Commentary: Industry advisors and property analysts have explicitly noted that the concentration of street-level crime risks reversing the CBD office and apartment market recovery, driving capital reallocation toward Brisbane, Perth, and select regional markets with stronger safety perception profiles.

Amenity Discount: Melbourne CBD high-density stock maintains prolonged price suppression and elevated vacancy rates relative to equivalent national CBD assets. The median unit value is recorded at $644,074, with quarterly growth stalled at 0.1% — a performance that cannot be fully explained by credit constraint or fiscal friction given equivalent dynamics in other capital cities have not produced comparable suppression.

Media Salience: Victoria recorded a 16.3% rise in the criminal incident rate and a 27.6% rise in retail theft over 2024–2025, generating a concentrated and sustained media narrative of deteriorating civic order in the Melbourne LGA that has demonstrably influenced institutional and retail capital allocation behaviour.

All three invocation criteria are evidenced. 24120 formally invoked — Melbourne City — Victoria.

24120 — Insufficient data for invocation — Hume / Brimbank: While socio-economic indicators suggest elevated crime perception, insufficient documented practitioner commentary explicitly linking safety perception to capital steering or amenity discounts in these specific zones at this observation date.

24120 — Insufficient data for invocation — Dandenong: A perception discount is documented, but it is conflated with structural vulnerability indicators captured under 24126, preventing an isolated 24120 invocation.

3.5 Victorian Triple-Suppressor Assessment

Victoria’s sustained structural underperformance relative to Queensland and New South Wales is the result of three concurrent suppressor mechanisms operating across distinct geographic footprints and through distinct causal pathways. This configuration has not been recorded in either of the other two jurisdictions assessed in this publication.

Suppressor A — State Fiscal Intervention (24200 APN Risk and Compliance Index™): The Windfall Gains Tax and augmented land tax thresholds apply systemic friction across all Victorian jurisdictions. Independent research indicates that four in five Victorians identify current tax settings as a direct deterrent to rental market investment. This suppressor operates at the state level and is not confined to specific SA4 zones — it applies structural yield compression to the entire Victorian investment landscape.

Suppressor B — Structural Vulnerability Convergence (24126 APN Acute Vulnerability Index™): Formally invoked for the Melbourne West SA4, this suppressor reflects the convergence of elevated unemployment, constrained housing delivery, and concentrated mortgage stress in outer-suburban corridors where the peak 2020–2021 lending cohort intersects with the current rate environment. This suppressor is geographically concentrated in the outer-ring mortgage belt rather than operating state-wide.

Suppressor C — Crime Perception Amenity Discount (24120 APN Sentinel™): Formally invoked for the Melbourne City SA4, this suppressor reflects the market pricing of perceived safety deterioration in the metropolitan core. It operates independently of Suppressors A and B — it is not a fiscal or credit mechanism, and it targets inner-urban high-density stock rather than the outer-suburban cohort affected by Suppressor B.

The Victorian professional sentiment signal is the aggregate output of these three non-overlapping suppressor mechanisms. Capital is being structurally reallocated away from the Victorian jurisdiction — toward Queensland, where the bullish decoupling is most pronounced, and toward interstate alternatives offering lower holding friction and more stable civic amenity profiles.

Section 4 — Counter-Narrative Assessment

The null hypothesis for this publication posits that neither the national professional sentiment decoupling nor the inter-state divergence constitutes a behavioural departure from empirical fundamentals — that all observed professional positioning reflects rational, data-grounded responses to genuine structural conditions.

Monetary Policy Expectations: The primary counter-narrative at the national level posits that professional optimism is a forward-discounting mechanism anticipating an RBA easing cycle. This is not supported by the institutional futures pricing. The ASX 30-Day Interbank Cash Rate Futures curve implies a 17% probability of a further increase to 4.60% by June 2026, with no material rate reductions priced until the second half of 2027. Professional optimism cannot be rationally attributed to anticipated near-term monetary relief on this basis.

Structural Supply Deficit Fundamentals: The strongest pillar of the national counter-narrative — that professional optimism reflects accurate pricing of supply-side inelasticity — is validated by the data. The NHSAC projection of a 204,000-dwelling shortfall, combined with the 48.6% escalation in construction costs, establishes a demonstrably rational basis for secondary market professional confidence. The supply constraint is not a narrative construct — it is evidenced across multiple Tier-1 data sources and is operative across all three jurisdictions, though most acutely in Queensland.

Fiscal Intervention and Sovereign Support: The confirmed Budget measures — Help to Buy (40,000 places), First Home Guarantee expansion, and Build-to-Rent MIT withholding tax reduction — provide legitimate, policy-driven foundations for professional confidence in specific market segments. These mechanisms partially offset the cohort exclusion generated by the 11.27% ADI stress rate and provide rational support for entry-level professional optimism among brokers and buyers agents servicing first home buyer cohorts.

Queensland: The null hypothesis is fully validated. Professional optimism in Queensland is empirically grounded in superior demographic structural capacity, unparalleled infrastructure expenditure, and material construction pipeline deficits that mathematically necessitate sustained price escalation. It is not a sentiment distortion.

New South Wales: The null hypothesis is validated for the investor advisory segment. The 16% projected expansion in investor lending confirms that practitioners are accurately servicing insulated capital. For the western Sydney mortgage belt segment, professional defensiveness is equally rational — it reflects accurate pricing of genuine credit exclusion in high-median-price markets with constrained borrowing capacity.

Victoria: The null hypothesis is validated. The Victorian triple-suppressor mechanism (24200 fiscal friction, 24126 structural vulnerability, 24120 Sentinel perception discount) constitutes a demonstrably rational basis for professional defensiveness. The counter-narrative for Victoria tests whether the Sentinel perception discount is overstated relative to objective crime data — and the evidence does not support overstatement. The 16.3% rise in criminal incidents and 27.6% rise in retail theft are objective data points, and their market pricing in the Melbourne City SA4 is commensurate with documented practitioner behaviour.

Analytical Conclusion: Professional sentiment across all three jurisdictions is fundamentally rational. The divergence between the states accurately reflects the underlying structural variance in demographic structural capacity, regulatory friction, and fiscal intervention. Queensland exhibits the most rationally grounded optimism. Victoria exhibits the most rationally grounded defensiveness. The national decoupling coefficient is not a behavioural anomaly — it is the mathematically logical output of a market structure in which capital flows have decoupled from the constraints binding the median wage-earning consumer, and professional sentiment reflects that structure with accuracy.

Section 5 — Budget Anticipatory Signal Matrix

The following matrix maps the confirmed and anticipated 2026–27 Federal Budget measures against professional cohort sentiment signals and 24300 index implications, extended with jurisdictional differentiation across Queensland, New South Wales, and Victoria.

| Budget Domain | Confirmed Position | National 24300 Implication | Queensland Differential | New South Wales Differential | Victoria Differential |

| Negative Gearing (new builds only; existing assets grandfathered) | Confirmed. Full grandfathering of approximately 1.28 million existing investors. | Bullish Decoupling — short-term acquisition spike driven by legislative deadline | High mitigation: strong infrastructure pipeline supports new-build pivot; elevated demand for grandfathered secondary stock | Material friction: acute physical supply constraints limit new-build transition; will compress future acquisition velocity in established suburbs | Force multiplier: compounds state-level fiscal friction; accelerates capital reallocation as investors face rising holding costs without offsetting deductions on future acquisitions |

| CGT Discount Transition (50% flat to inflation indexation; one-year grace period) | Confirmed. Transition mechanism with 12-month implementation window. | Defensive Convergence — anticipated long-term secondary market liquidity contraction | Moderate absorption: approximately 20% annualised capital growth provides deep equity buffers against the indexation transition | Yield protection: high-value asset holders likely to hold long-term, further restricting secondary market liquidity | Accelerated divestment: marginal yields and elevated state taxes make the 50% discount structurally critical; transition likely to trigger a pre-emptive liquidity event |

| Help to Buy (shared equity; 40,000 places; up to 40% for new builds, 30% for existing) | Confirmed. Income caps: $100,000 individual / $160,000 joint. State price caps apply. | Bullish Decoupling — demand-side capacity expansion partially offsetting rate environment | Unit sector catalyst: $1M Brisbane cap sits below the $1.2M house median but aligns with the $865,000 unit median; directs concentrated demand into strata stock | Structurally constrained: $1.3M Sydney cap is functionally limited against median house values; utility restricted to outer-ring SA4 zones and specific apartment corridors | Moderate utility: $950,000 Melbourne cap broadly aligns with the $982,000 median; provides functional capacity expansion for structurally constrained cohorts |

| First Home Guarantee (5% deposit; uncapped places; income limits removed; price caps increased) | Confirmed. All streams expanded. | Neutral — offsets existing structural supply constraints without resolving delivery deficit | Moderate positive: provides entry-level capacity support in regional Queensland markets where price caps align with medians | Limited positive: outer-ring SA4 zones primary beneficiary; minimal impact on median Sydney price environment | Moderate positive: aligns with Melbourne’s underperforming median price environment; provides functional support for structurally constrained first home buyer cohorts |

| Build-to-Rent (MIT withholding reduced to 15%; depreciation increased to 4%) | Confirmed. Extended to projects regardless of commencement date. | Bullish Decoupling — institutional capital deployment overriding retail constraint | Positive: supports institutional pipeline delivery into Southeast Queensland’s supply-deficient corridors | Positive: provides structural catalyst for institutional capital in supply-constrained Sydney corridors where retail development is financially unviable | Highly positive: critical mechanism for deploying international institutional capital into a jurisdiction where retail investor departure has structurally reduced rental supply |

| State Fiscal Friction (Land Tax, WGT) — baseline context | Not a federal Budget measure; included for jurisdictional comparative context | Jurisdictional Arbitrage — capital actively rotating from Victoria toward Queensland | Relative structural advantage: lower comparative tax burden functions as a magnet for interstate capital deployment | Neutral / stable: absence of sudden state tax escalation provides a predictable, if costly, operating environment | Material suppressor (24200): WGT and expanded land tax thresholds systematically suppress development viability and investor yield across the jurisdiction |

Section 6 — 24310 APN Symbiotic Intelligence Network™ Extractions

All qualitative extractions in this section are classified as Unverified Community Sentiment in accordance with the Bifurcated Source Integrity Rule. Each extraction is directly quoted with source and date, and is followed immediately by APN Clinical Reframing translating the colloquial observation into APN Clinical Authority register.

National Extractions

Unverified Community Sentiment: “The headline version: negative gearing for investment properties is being restricted to new builds only. The detail that most headlines are burying: existing landlords who currently negatively gear are grandfathered. Their tax concessions stay. All of them. That’s roughly 1.28 million Australians who won’t lose a thing… For your clients who already own investment properties, the short answer is: nothing changes for you.” — Samantha McLean, Managing Editor, Elite Agent, 10 May 2026.

APN Clinical Reframing: The anticipated grandfathering of negative gearing provisions establishes a structural policy advantage protecting incumbent asset holders. By insulating the existing cohort from fiscal friction, the State Intervention Framework systematically advantages established equity over prospective capital accumulation, thereby maintaining existing yield architectures in the secondary market and validating the Asset-Wage Divergence construct documented across nodes 21210 and 21240.

Unverified Community Sentiment: “Economic conditions have changed since the last survey. Inflation remains above the RBA’s target 2 to 3% range and cost-of-living and housing supply challenges persist. The data derived from the February survey will help us determine what impact these and other economic factors have had on borrower behaviour.” — Anja Pannek, CEO, Mortgage and Finance Association of Australia, February 2026.

APN Clinical Reframing: Intermediary data confirms the persistent degradation of retail borrower capability. Sustained macroeconomic pressures — specifically elevated inflation (Node 21220) and stringent ADI serviceability buffers (Node 21350) — are applying material downward pressure on consumer transactional capacity, actively validating the divergence tracked within the 24300 Decoupling Coefficient.

Queensland Extractions

Unverified Community Sentiment: “The overwhelming constraint on housing affordability remains a lack of supply… Queensland is well behind what is needed in terms of dwelling approvals — the 12-month building approvals to January 2025 were around 35,800 dwellings, substantially under the National Housing Accord target.” — Antonia Mercorella, CEO, Real Estate Institute of Queensland, 2026.

APN Clinical Reframing: The primary Queensland industry body confirms a state of structural supply inelasticity. The physical delivery deficit ensures that demand-side fiscal interventions will not materially improve accessibility in the near term, mathematically sustaining the scarcity pricing dynamic that underpins the bullish decoupling recorded in the Queensland component of the 24300 index.

New South Wales Extractions

Unverified Community Sentiment: “Government must stop driving investors out of the residential market through anti-landlord reforms. These reforms reduce rental supply and compound the dire situation. Demand is rising fast and the supply gap is widening at an increasing rate.” — Tim McKibbin, CEO, Real Estate Institute of New South Wales, 2026.

APN Clinical Reframing: Industry leadership identifies that legislative and policy settings (Node 21370) are generating material regulatory friction in the New South Wales rental market. This friction functions as a structural disincentive for capital deployment in the private rental sector, exacerbating the supply deficit and sustaining upward pressure on rental yields — a dynamic that is rationalising continued professional optimism in the investor advisory segment despite deteriorating consumer conditions.

Victoria Extractions

Unverified Community Sentiment: “Ironically, the relentless 10-year period of rental regulation and property tax increases we have seen play out in Victoria has served to increase complexity and holding costs for rental providers, while failing to materially improve rental affordability and access.” — Toby Balazs, CEO, Real Estate Institute of Victoria, 2026.

APN Clinical Reframing: The Victorian property sector formally recognises that sequential state fiscal interventions (Node 21310) have materially degraded the investment landscape. The compounded cost burden actively suppresses yield-maximising behaviour, validating the structural capital reallocation away from the jurisdiction that is documented in the 24300 Victorian signal.

Works Cited

- APN Master Codex 21000 Series Q4 2025 v2

- APN Codex Summaries v2.31 — April 2026

- APN Advanced Lexicon — April 2026

- APN Causal Pathway Matrix: 21000 Series → 24100 Series

- ANZ-Roy Morgan Consumer Confidence — record low 63.1, Roy Morgan Research, 24 March 2026. https://www.roymorgan.com/findings/9940-anz-roy-morgan-consumer-confidence-march-24

- ANZ — Consumer confidence falls to lowest since records began in 1973. https://www.anz.com.au/newsroom/media/ANZRoyMorganAustralianConsumerConfidence/consumer_confidence_hits_lowest_since_records_began_in_1973/

- ANZ-Roy Morgan Consumer Confidence, weekly results 2026. https://www.anz.com.au/newsroom/media/ANZRoyMorganAustralianConsumerConfidence/

- Roy Morgan Update May 5, 2026: Consumer Confidence and Business Confidence. https://www.roymorgan.com/findings/roy-morgan-update-may-5-2026

- NAB Monthly Business Survey March 2026. https://news.nab.com.au/content/dam/nab-news/documents/economics/202603%20NAB%20Monthly%20Business%20Survey%20March.pdf

- NAB Quarterly Business Survey Q1 2026. https://www.nabtrade.com.au/insights/news/2026/03/nab-business-survey—q1-2026–conditions-and-confidence-down-in

- Australia Business Confidence — Trading Economics. https://tradingeconomics.com/australia/business-confidence

- ANZ-Indeed Australian Job Ads — April 2026. https://www.staffingindustry.com/news/global-daily-news/australias-anz-indeed-job-ads-slide-further-in-april

- APRA Quarterly ADI Statistics — December 2025. https://www.apra.gov.au/news-and-publications/apra-releases-quarterly-authorised-deposit-taking-institution-statistics-26

- Investment housing credit reaches 8.5% annual growth rate, March 2026 — Broker Pulse. https://www.brokerpulse.com.au/news/investment-housing-credit-reaches-8-5-annual-growth-rate-for-march-2026

- ABS 5601.0 Lending Indicators, December Quarter 2025. https://www.abs.gov.au/statistics/economy/finance/lending-indicators/latest-release

- Property Council of Australia / Procore Industry Sentiment Survey, Q1 2026 — Mortgage Professional Australia. https://www.mpamag.com/au/news/general/property-industry-confidence-drops-to-four-year-low/573479

- Master Builders Australia — new construction forecasts and pre-Budget commentary, May 2026. https://masterbuilders.com.au/new-construction-forecasts-a-call-to-action-for-federal-budget/

- Master Builders Australia — response to RBA rate decision, May 2026. https://masterbuilders.com.au/statement-on-rbas-decision-to-lift-interest-rates-from-master-builders-australia-ceo-denita-wawn/

- MFAA — borrower confidence survey, February 2026. https://www.brokernews.com.au/news/breaking-news/brokers-urged-to-map-borrower-mood-in-mfaa-survey-288840.aspx

- RBA Statement on Monetary Policy, May 2026. https://www.rba.gov.au/publications/smp/2026/may/outlook.html

- ASX 30-Day Interbank Cash Rate Futures. https://www.asx.com.au/markets/trade-our-derivatives-market/futures-market/rba-rate-tracker

- National Housing Supply and Affordability Council 2026 report — HIA response. https://hia.com.au/-/media/files/newsroom/submissions/2026/national-housing-supply-council-gets-the-diagnosis-right—economic-insight.pdf

- ABS 8731.0 Building Approvals, January 2026. https://www.abs.gov.au/statistics/industry/building-and-construction/building-approvals-australia/jan-2026

- ABS Labour Force, Australia, March 2026. https://www.abs.gov.au/statistics/labour/employment-and-unemployment/labour-force-australia/latest-release

- Help to Buy — Housing Australia launch. https://www.housingaustralia.gov.au/media/more-australians-supported-home-ownership-launch-australian-government-help-buy-scheme

- First Home Guarantee — property price caps. https://firsthomebuyers.gov.au/australian-government-5-percent-deposit-scheme/property-price-caps

- Build-to-rent tax concessions — ATO. https://www.ato.gov.au/about-ato/new-legislation/in-detail/businesses/incentives-to-increase-the-supply-of-housing

- Negative gearing and CGT changes — broker briefing, Mortgage Professional Australia. https://www.mpamag.com/au/news/general/budget-to-shake-up-negative-gearing-cgt-and-trusts-what-brokers-need-to-know-now/573981

- CGT and negative gearing one-year reprieve — Mortgage Professional Australia. https://www.mpamag.com/au/news/general/property-investors-to-get-one-year-reprieve-on-cgt-negative-gearing-reforms/574669

- Elite Agent — negative gearing grandfathering detail, Samantha McLean, 10 May 2026. https://eliteagent.com/what-your-investor-clients-are-googling-right-now/

- NAB Housing Monitor, April 2026. https://news.nab.com.au/content/dam/nab-news/documents/economics/2026-04-09%20-%20Housing%20Monitor.pdf

- Queensland population growth highlights and trends, 2026 edition — QGSO. https://www.qgso.qld.gov.au/issues/3071/population-growth-highlights-trends-qld-2026-edn.pdf

- Queensland Budget 2025–26 Revenue Paper. https://budget.qld.gov.au/files/Budget-2025-26-BP2-Revenue.pdf

- REIQ — Queensland property prices and supply pressures, 2026. https://www.reiq.com/resources/media-releases/queensland-property-prices-pushed-up-by-persistent-supply-pressures

- REIQ — building approvals commentary, 2026. https://www.theonsitemanager.com.au/news/reiq-calls-out-home-truths-on-state-governments-housing-response/

- Home lending growth 2026 — Property Update. https://propertyupdate.com.au/home-lending-to-grow-7-in-2026-as-investor-demand-continues-momentum-new-data-reveals/

- Central West Labour Market Dashboard — Jobs and Skills Australia, April 2026. https://www.jobsandskills.gov.au/sites/default/files/2026-04/Labour%20Market%20Dashboard%20Central%20West_0.pdf

- First Home Buyer Choice — abolition context — Marsdens Law Group. https://www.marsdens.net.au/about-us/latest-news/first-home-buyer-choice-the-short-lived-annual-property-tax/

- Victoria Labour Market Dashboard — Jobs and Skills Australia, April 2026. https://www.jobsandskills.gov.au/sites/default/files/2026-04/Combined%20-%20Labour%20Market%20Dashboard%20Victoria_0.pdf

- REIV — property tax reform advocacy. https://reiv.com.au/advocacy/property-tax-reform

- Victoria’s land tax investor exodus — realestate.com.au. https://www.realestate.com.au/news/victorias-land-tax-grab-backfires-as-investor-exodus-hits-budget/

- Windfall Gains Tax — State Revenue Office Victoria. https://www.sro.vic.gov.au/owning-property/windfall-gains-tax/understanding-windfall-gains-tax

- Reforming Victoria’s Windfall Gains Tax — Mandala Partners. https://mandalapartners.com/reports/windfallgainstax

- Victorian property tax comparison — Victorian Parliamentary Budget Office. https://pbo.vic.gov.au/response/7644

- Victorian State Budget 2026–27 analysis — Pitcher Partners. https://www.pitcher.com.au/insights/victorian-state-budget-2026-27-analysis/

- REIV — state budget response, 2026. https://reiv.com.au/our-industry/news/-underwhelming-2026-27-state-budget-a-missed-opportunity-to-address-victoria-s-ongoing-rental-market-challenges

- Digital Finance Analytics — mortgage stress suburbs, 100% stress concentration. https://www.brokernews.com.au/news/breaking-news/financial-stress-soars-as-dfa-flags-100stress-suburbs-289282.aspx

- Shadows in the City — safety, sentiment and value erosion — Wizel Property Group. https://wizelpropertygroup.com/shadows-in-the-city-safety-sentiment-and-the-silent-value-erosion/

- Is crime really getting worse in Melbourne? — Melbourne Businesses. https://www.melbournebusinesses.com.au/is-crime-really-getting-worse-in-melbourne/

- Melbourne Office Market Dynamics Q1 2026 — JLL. https://www.jll.com/en-au/insights/market-dynamics/melbourne-office

- REINSW — investor market commentary, 2026 (attributed to Tim McKibbin).

- Brisbane property market update, March 2026 — Smart Property Investment. https://www.smartpropertyinvestment.com.au/hotspots/27623-brisbane-property-market-update-march-2026

- Australia Consumer Confidence — Trading Economics. https://tradingeconomics.com/australia/consumer-confidence

- Westpac-Melbourne Institute Consumer Sentiment, April 2026 — Westpac IQ. https://www.westpaciq.com.au/economics/2026/04/consumer-sentiment-april-2026

- B2B payment practices Australia 2026 — Atradius. https://atradius.at/wirtschaft-maerkte/reports/b2b-payment-practices-trends-in-australia-2026

- Australia braces for construction insolvencies — MacroBusiness, April 2026. https://www.macrobusiness.com.au/2026/04/australia-braces-for-a-new-wave-of-construction-insolvencies/

All analysis is conducted under the editorial standards of Australian Property Network. Findings are presented on the basis of data and evidence alone. No commercial relationships, advertiser interests, or industry body affiliations have influenced the findings of this publication.